Editor’s Note: This is the final post of a 3-part analysis of FSA loan program usage throughout FY 2017. Prior posts focused on lending trends for beginning farmers and overall annual trends.

Recognizing that farmers of color and female farmers have historically experienced disproportionate burden and discrimination when seeking access to loan financing, the National Sustainable Agriculture Coalition (NSAC) and our allies have worked to ensure that USDA’s Farm Service Agency (FSA) loan programs include target participation rates for “socially disadvantaged” (SDA) farmers – including women and farmers of color. For years, these target rates have helped to ensure that both banks and individual FSA county offices are equitably serving all farmers in need of financing.

In fiscal year (FY) 2017, FSA administered over 8,700 operating and ownership loans to SDA farmers and ranchers, helping them to start and sustain businesses by defraying the cost of farm-related real estate purchases and annual operating costs. While FSA has certainly made progress over the years in improving and increasing its level of service to SDA farmers, their outreach has so far has not been adequate to keep up with the growing demand.

In NSAC’s recent review of FSA’s FY 2017 lending trends, we were disappointed to find that lending to SDA farmers and ranchers decreased for the second year in a row; from FY 2016-2017, the total number of loans to SDA farmers and ranchers decreased by four percent.

In this post, we will dig deeper into FSA’s recent and historic SDA lending trends. We will review data by geographic region, loan type, and provide thoughts on FSA’s lending outlook going forward.

Primer on FSA SDA Farmer Loans

FSA offers farmers two types of loans: direct loans, which come out of USDA’s funding pool, and guaranteed loans, which are provided by private lenders and backed by USDA. To ensure that SDA farmers and ranchers can access these loan programs, Congress requires USDA to set annual target loan participation rates, which are determined on a state-by-state basis and impacted by the overall population demographics.

For direct farm ownership (DFO) loans, the target lending rate is determined by the total percent of SDA persons living in a particular county. For direct operating (DO) loans, the target is determined by the percentage of SDA producers in a state. If there is leftover funding in a state’s SDA pool, that funding can be transferred to a state with higher demand. See our Grassroots Guide for more details on how target participation rates are set by FSA.

SDA Farmer Lending Trends for FY 2017

- Roughly a quarter of all FSA loans support SDA farmers

- Total loans to farmers of color and women dropped for the second year in a row

- FSA is making or guaranteeing 33 percent more SDA loans over the past 5 years

- FSA financing for SDA farmers has increased by 53 percent over the past 5 years

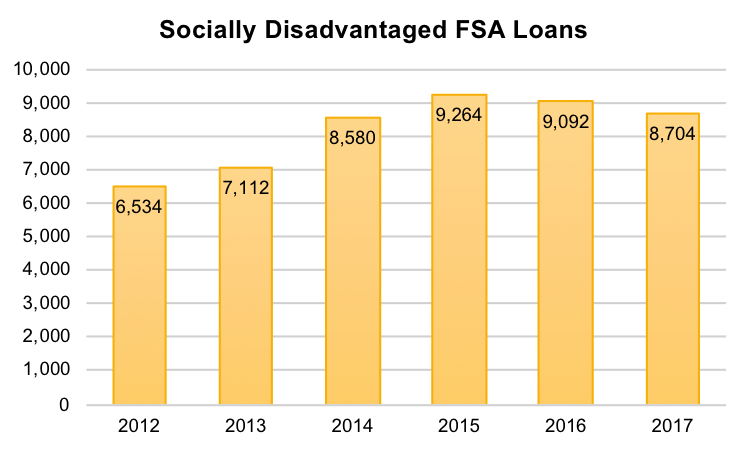

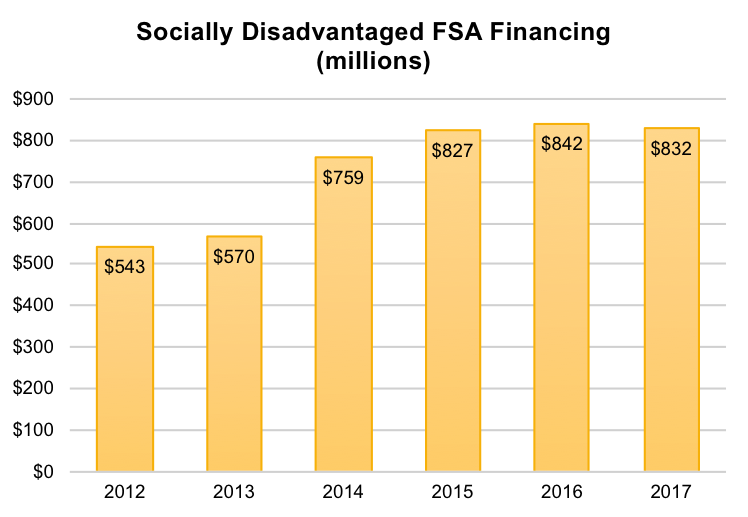

Overall, SDA farmers represent 23 percent of FSA’s total loan portfolio, which is roughly the same share as last year. Together, women and farmers of color received 8,704 FSA loans ($832 million) in FY 2017; 388 fewer loans than were made in 2016. The majority of these loans are made directly by FSA to cover annual farm operating expenses.

Although the total number of SDA farmer loans has declined by 6 percent since FY 2015, the overall number had previously (from FY 2012-2015) been steadily increasing (see chart below).

From 2012 to 2015, FSA increased not only the number of loans to SDA farmers (41 percent increase); it also increased the total financing provided (35 percent increase) to SDA producers (see chart below).

The lending trends of the last few years are concerning, particularly because the largest slide in SDA lending in these years has been in FSA’s own lending through its Direct Operating program. NSAC urges USDA to closely evaluate county-by-county SDA lending trends, compare these performance measures to the target lending goals, and report this information, as required by Congress when these target rates were first established in 1987.

Direct vs Guaranteed Lending Trends

- DO loans are the most in demand, but also experienced biggest reduction in service to SDA farmers

- Slight increase in SDA operating loan guarantees

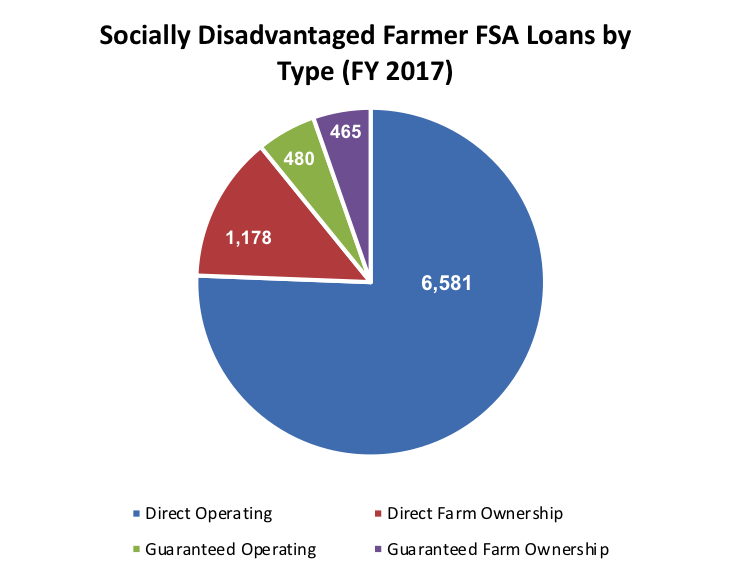

Farmers of color and female farmers have historically relied most heavily on FSA direct loans; especially DO loans, which account for 76 percent of all SDA loans (see chart below). Preference for DO loans among SDA producers follows the same trend as those seen for beginning farmer loans and for all FSA loans generally.

In FY 2017, SDA operating loans accounted for nearly a third of all FSA operating loans, while SDA ownership accounted for roughly a quarter. This suggests that there are likely still gaps in financing options and/or that barriers to land ownership persist for historically underserved farmers – particularly for farmers of color and female farmers.

Direct operating loans saw the largest absolute drop in SDA loan making last year – with 432 (6 percent) fewer loans made as compared to 2016.

Guaranteed Operating Loans (GOL), however, had a surprising increase of 24 percent (93 additional loans) more loans made as compared to FY 2016. This is particularly perplexing given that GOL experienced an 8 percent decrease in total number of loans made between FY 2015 and FY 2016. Total GOL SDA funding also significantly increased in FY 2017 (by 28 percent).

Nationally, Louisiana, California, and Oklahoma saw the largest increases in banks using loan guarantees for SDA farmers in FY 2017.

It’s difficult to understand what specific factors led to these increases in GOLs over other loan types, however, loans to beginning farmers (another group of farmers who are historically underserved) followed a similar, albeit less dramatic, trend.

One possible reason for the increase could be that more SDA farmers were able to successfully graduate from direct FSA financing to obtaining a loan from a private bank (with an FSA loan guarantee). FSA direct loans to SDA farmers decreased by 432 in FY 2017, and looking at the numbers, nearly a quarter of these loans could have plausibly transferred from direct to guaranteed lending.

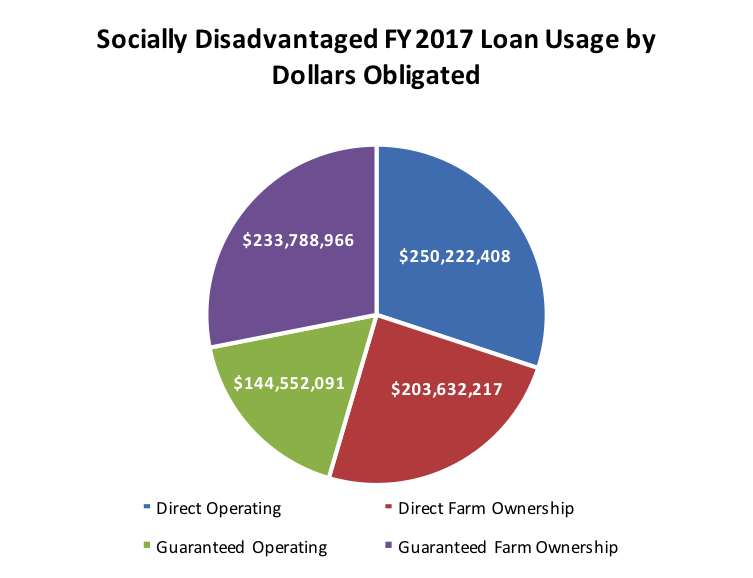

Guaranteed loans to SDA farmers represent only 11 percent of all SDA farm loans, however, these loans are on average much larger (and consequently take a much bigger slice of the total FSA funding pie) than other types of lending (see chart below). In FY 2017, guaranteed loans made up 45 percent of all FSA SDA lending, and the average SDA guaranteed loan was $400,360 (as compared to $58,4893 for a direct loan).

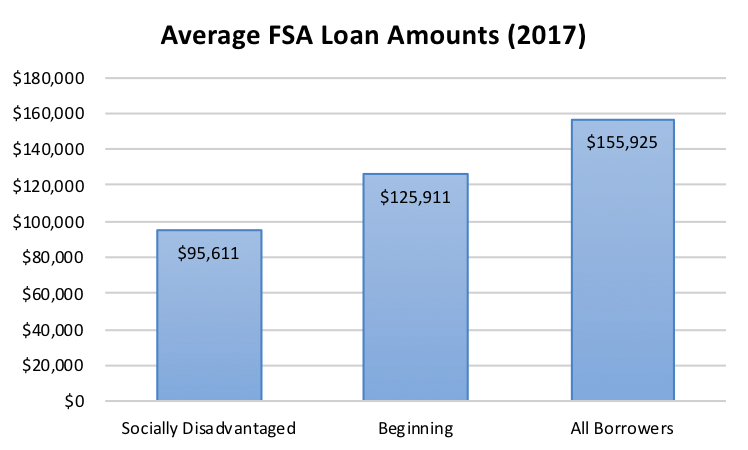

Across all FSA loan programs, the average SDA farmer loan increased slightly: from $92,571 in FY 2016 to $95,611 in FY 2017. Despite this modest increase, the average loan to a SDA farmer is still smaller (across all loan categories) as compared to loans made to other types of farmers (see chart below).

Given the historic discrimination and unique challenges that farmers of color and women have faced in securing financing, it is especially troubling that FSA decreased its support to SDA farmers across nearly every loan program in FY 2017. While some drop would be expected given the overall decrease in loan demand last year, direct operating and ownership loans to SDA farmers experienced a much larger and relatively disproportionate drop.

In fact, even though FSA DO loans were up by two percent overall in FY 2017, these same loans to SDA farmers decreased by roughly the same percent. In practice, this means that fewer farmers of color and female farmers would have been able to take advantage of FSA financing to purchase farmland last year. NSAC encourages FSA to examine this concerning trend and to work quickly to identify potential ways it can be addressed within the agency.

Regional Analysis

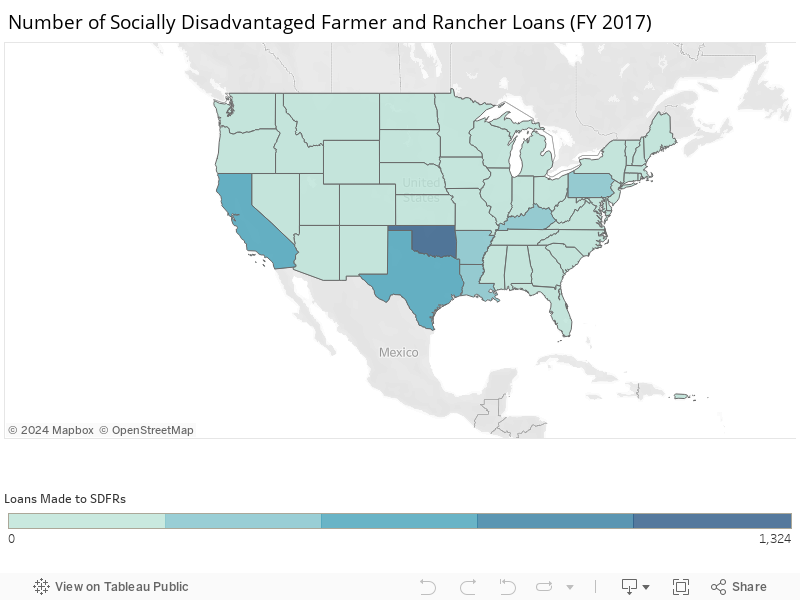

The geographic distribution of FSA loans to SDA farmers is unique compared to FSA lending to other groups. SDA lending tends to be more heavily concentrated in the South and West (see map below), which have higher populations of minority farmers, whereas loans to many other farmer groups are clustered around the agricultural regions of the Midwest and Great Plains.

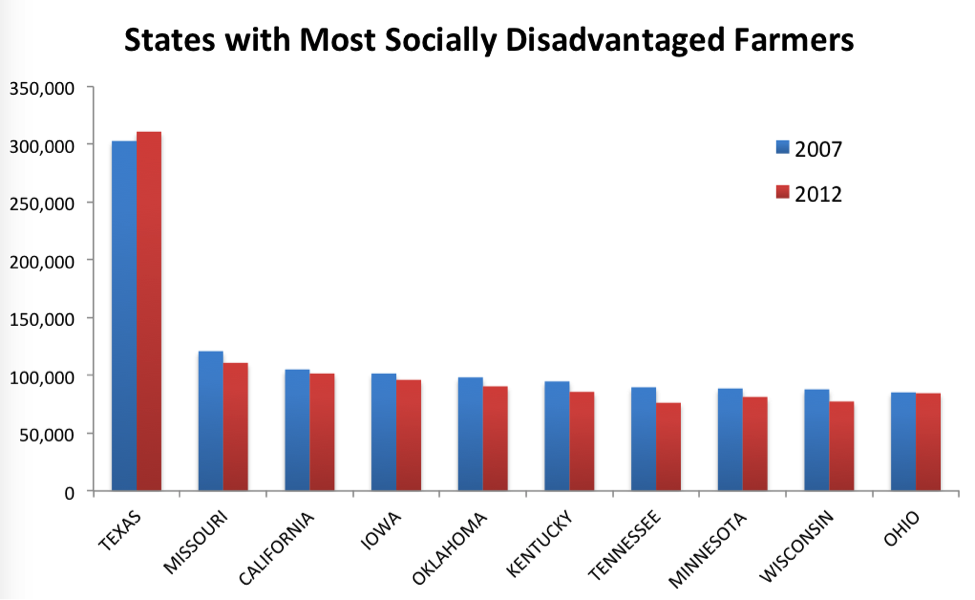

Following similar trends as those reported in the U.S. Census of Agriculture (see chart above), the states making the most SDA farmer loans include: Oklahoma, Texas, California, Kentucky, Arkansas, Louisiana, and Pennsylvania.

Missouri, Iowa, Tennessee, Minnesota, Wisconsin, and Ohio, which reported high numbers of SDA farmers in the Census, strangely reported lower than expected numbers of loans to these same farmers. NSAC recommends that FSA follow up with farmers and county offices in these states to see what can potentially be done to improve outreach or targeted assistance to these communities.

The states reporting the fewest number of SDA loans were generally also those with less diverse farming populations or less agricultural production in general. These areas include the Northeast, Intermountain West, and the Midwest.

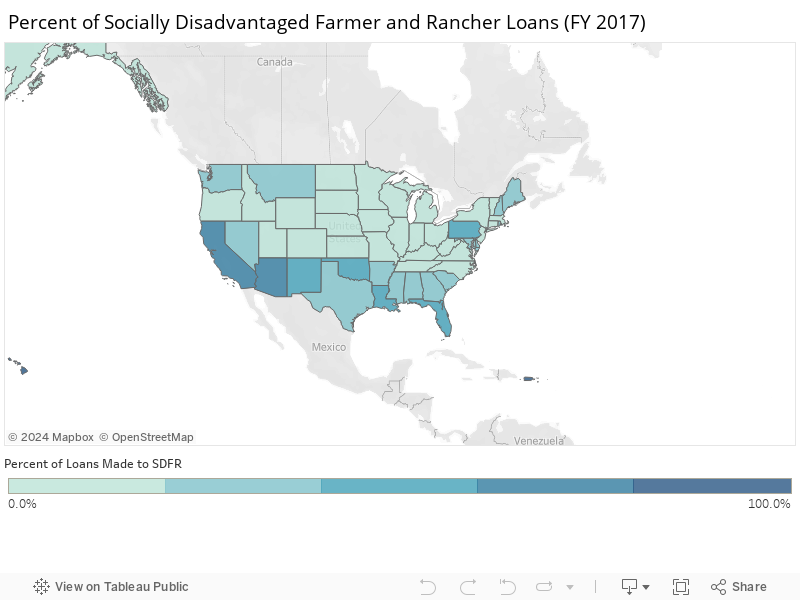

Interestingly, the areas with the highest percentage of loans to SDA farmers were also those where FSA loans to beginning farmers were particularly low. States with a higher percentage of farmers of color (e.g., California, Arizona, New Mexico, Texas, Oklahoma, Florida, and Louisiana) also made a larger percentage of their state’s total FSA loan portfolio to these farmers (see map below for concentration of SDA farmers nationally).

One state that stands out for having both a large number of SDA loans and a higher than expected percentage of loans to SDA farmers is Pennsylvania. In total, over 48 percent of all loans in PA were made to women or farmers of color in FY 2017 – most of these were made directly by FSA.

It is also important to note that the islands and U.S. territories (i.e., Puerto Rico, Hawaii and the Pacific Territories) had the highest percentage of SDA loans as compared to other states. The same trend is also evident in California, which awarded the largest percentage of loans to SDA farmers of any state in the continental U.S. California, however, also had one of the lowest percentage of loans to beginning farmers (for more information on FSA lending to beginning farmers, see our previous blog post).

Unfortunately, FSA provides limited data on the demographic breakdown of SDA farmer loans, so it is difficult to determine how many of these loans went to female farmers vs. veteran farmers vs. farmers of color. This is in part due to the fact that there is overlap between these demographic groups, and that “socially disadvantaged farmers” are defined by Congress to include both ethnic minorities and women.

NSAC will continue to work with USDA and Congress to further advance FSA’s data collection and reporting abilities so that we might better understand to what extent and how well farmers are being served by these important federal programs.

Final Takeaway

It is clear that FSA loans remain an important source of financing for farmers of all kinds – including those just starting out and others who have been historically underserved by private lenders. With the farm bill on the horizon and changes to loan programs being considered (including whether or not to raise the limit on the maximum amount a farmer can borrow), it is important to understand first, how these programs are being utilized and which farmers still struggle to gain access to loan funding – both within certain regions and populations across the country.

It is clear from our analysis that despite the existing policy mechanisms to target funding to underserved farmers, not all farmers are able to gain access to this fundamental USDA farm program. Additional evaluation of specific lending trends related to specific demographics (beginning, women, veteran, farmer of color, etc) on a state by state basis is needed to understand what the unique barriers are to accessing federal loan financing through FSA, and consequently, what the policy solutions may be to address these barriers.

NSAC will continue to work with both Congress and USDA to improve evaluation, oversight and accountability of these federal programs to ensure equitable access to farmers of all kinds.