Editor’s Note: For more information on the state of organic agriculture, see this article’s companion post: “Inter-Agency Blockages Threaten to Halt Further Progress on Organic Crop Insurance“

Consumer demand for organic products has been growing steadily – U.S. organic food sales approached an estimated $37 billion in 2015, up 12 percent from the previous year. Although organic products often come with a higher price tag than conventional counterparts, the U.S. Department of Agriculture’s (USDA) organic certification offers an assurance to consumers that their food has not been produced with synthetic fertilizers, sewage sludge, irradiation, or genetic engineering, and that the distributors and retailers have not comingled organic foods with non-organic products. So far, this appears to be a trade off that many Americans are willing to make. Despite higher price premiums, however, supply-side challenges could threaten organic agriculture’s ability to meet growing demand.

A recently published report from USDA’s Economic Research Service (ERS) analyzed trends in organic price premiums for 17 popular organic products and identified opportunities and challenges to the industry’s growth. Key findings from this report are summarized below.

Domestic Supply Unable to Keep Up

The obvious response to the rising demand for organic products is to expand their availability to consumers. However, domestic supply from organic growers has so far failed to keep pace with demand levels that show no signs of waning. A 2015 study by the Organic Trade Association (OTA) indicated that the U.S. is a net importer of organic products. Last year we exported $550 million worth of domestically grown organic products (mostly fresh organic produce), and imported $1.3 billion worth (the most imported product being coffee, followed by soybeans).

Increasing demand in both the domestic and global markets has put pressure on U.S. organic supply and led to USDA’s inclusion of a goal to increase the number of certified organic operations in its 2014-2018 strategic plan.

Organic Price Premiums

Premiums for organic products are supported by consumers’ willingness to pay more for organics – particularly since the establishment of the USDA organic label, which provides clear product differentiation for organic foods.

A 2010 survey of consumer attitudes toward organic and “natural” products indicated that shoppers were willing to pay up to 30 percent more for organic products. However, the report also noted that consumers believe the price gap between organic and conventional food is getting smaller.

Ongoing efforts to increase organic production will need to include assessment of whether (and if so, by how much) producers are able to receive a higher retail premium for their products. While field crop producers can consult the wholesale market to determine potential premiums (where comparing conventional and organic product prices is relatively straightforward), retail price premiums for other organic products are more complex, making them significantly more difficult to predict.

Organic Price Premium Changes, 2004-2010

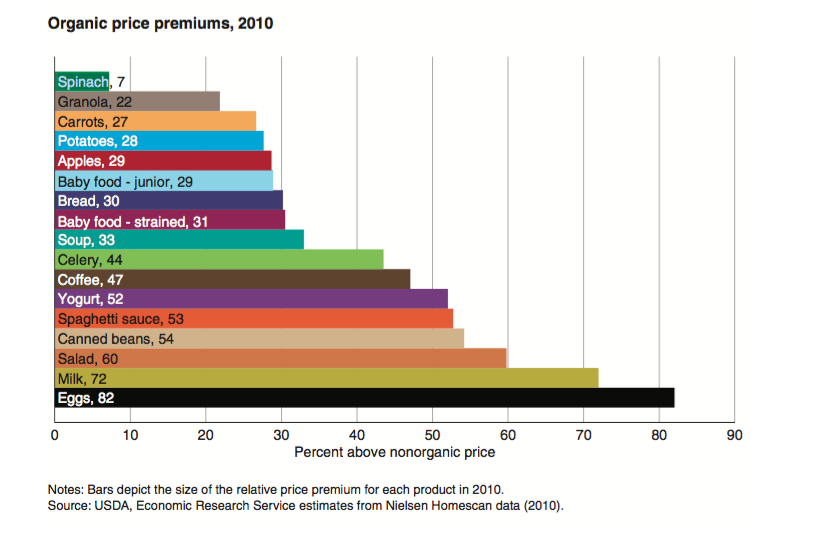

The ERS report provides valuable insights regarding the trends in organic price premiums, addressing a collective gap in understanding of these fluctuations at the retail level. Using consumer data, the report investigates changes in retail price premiums for 17 organic food products between 2004 and 2010. The data was nationally representative and the 17 products were chosen from three categories (fresh fruits/ vegetables, eggs/dairy, and processed foods), with a focus on products that had high sales, and whose conventional counterparts had high pesticide use characteristics.

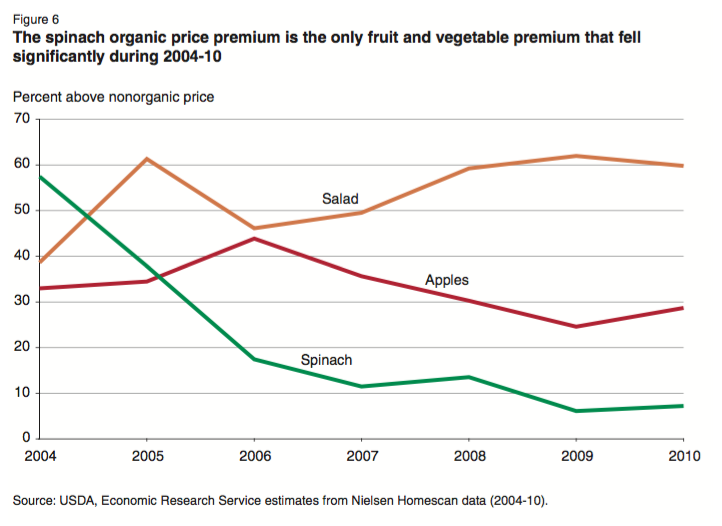

For all 17 of the products examined, organic price premiums were positive, meaning that prices were higher for the organic products compared to their conventional equivalents. As the chart below illustrates, retail premiums were greater than 20 percent of the non-organic price for all products examined, with the exception of spinach.

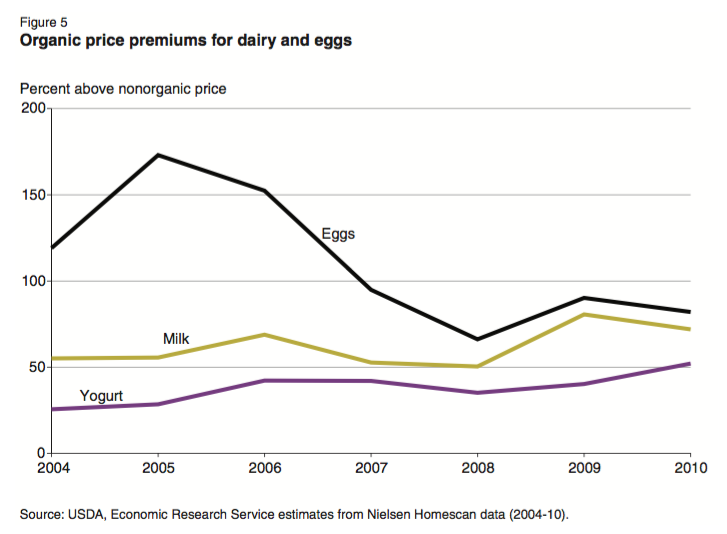

- Dairy and Eggs: Premiums were highest for dairy and eggs. Variation ranged from a low of 52 percent of the non-organic price, in the case of yogurt, to a high of 82 percent of the non-organic price for eggs.

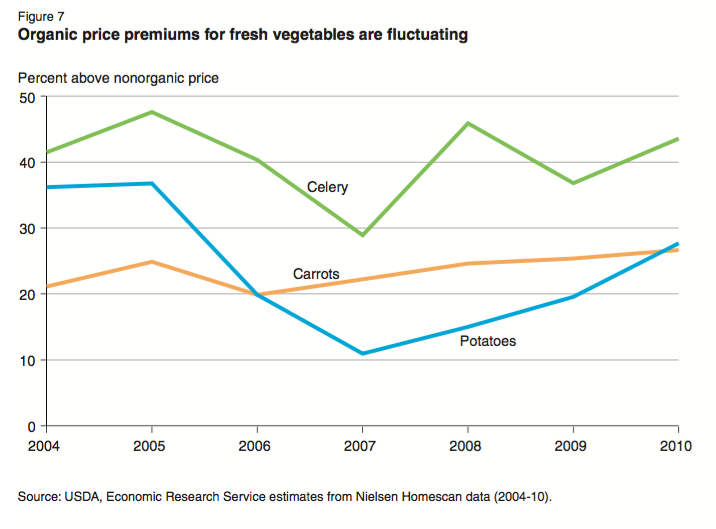

- Fresh Fruits and Vegetables: Prices for fresh fruits and vegetables had the most variability between 2004 and 2010, with premiums ranging between 7 and 60 percent of the non-organic prices of each product.

- Processed Foods: Organic prices for processed foods, which represent a growing share of the organic industry and include both single and multi-ingredient products, ranged between 22 and 54 percent of their non-organic counterparts.

It is not surprising that premiums showed the most variability between 2004 and 2007, when the USDA organic standards were still relatively new. The share of organic sales out of the total market increased for all products in the study, with sales generally higher for products with lower premiums or for foods frequently fed to children.

Supply-Side Costs for Organic Livestock Producers

The ERS report found that premiums for dairy and eggs were higher than for other products, likely driven in part by higher costs particular to organic livestock farmers. These costs include the higher price of organic feed, the cost of transitioning from a conventional to organic herd, and organic healthcare practices (which do not allow the use of antibiotics or growth hormones). Shortages in the supply of organic feed, as well as the time and risk involved in converting pastureland to organic, have meant that producers of organic livestock have been unable to keep pace with increases in demand for their products – particularly for organic milk. This disparity may lead to even higher premiums for milk in the future.

As the chart below illustrates, price trends varied among egg and dairy products from 2004 to 2010. Premiums for organic eggs dropped, while yogurt premiums increased, and milk premiums were designated as undetermined. Milk prices in the conventional market are historically volatile, and some of the same factors that influence conventional price irregularity may similarly affect organic milk prices.

Fresh Fruits and Vegetables Dominate

Fresh fruits and vegetables make up the largest segment of the organic market – 35 percent of all organic sales as of 2012. Organic price premiums for fresh produce, as illustrated by the following charts, fluctuated significantly over the course of the study.

Product-specific attributes may account for much of this variability. For example, certain apple varieties are more common in the organic market, and apple variety was shown to be the most important price-differentiating factor for consumers, even more so than whether the apple was organic or conventional. Some products also experienced dramatic changes in their markets during the study period, which may have contributed to price premium shifts. Both organic and non-organic produce industries are expanding their processing, pre-packaging, and brand offerings, and these changes likely influenced the premium fluctuations observed. Salad mix, for example, shifted from being available primarily as loose greens sold at a per-weight price to a wide variety of pre-washed and pre-cut packages, and even some salad kits that include nuts, dressings, and other toppings. Similar supply-side shifts are expected in the future as consumers look for healthier options, premium fluctuations are expected to continue for these products.

More Data Still Needed

While the ERS report provides valuable insight into organic price premium trends, the study was limited by its method of gathering data from consumers, who may have become more price conscious over the course of the study. The report also does not reflect organic premiums for products sold directly from farmers to customers via farmers’ markets, community supported agriculture (CSAs), or other direct-sale mechanisms.

Looking Ahead

Despite increasing demand for organic products, challenges remain for producers looking to transition to organic or expand their organic product offerings. There are several resources available to support this transition, including organic certification cost share assistance, conservation support through the Environmental Quality Incentives Programs (EQIP), and crop insurance options for transitioning producers. Additional data on organic price premiums can also help inform producers looking to utilize new expansions in crop insurance tailored to the needs or organic producers. USDA’s Risk Management Agency (RMA) is currently working on expanding organic price elections that may allow for more robust safety nets for organic farmers, and evidence-based figures on price premiums can help RMA in that task.

The National Sustainable Agriculture Coalition (NSAC) is engaging in efforts to ease the transition to organic, and we will be keeping an eye on further research on barriers to and opportunities for organic transition.