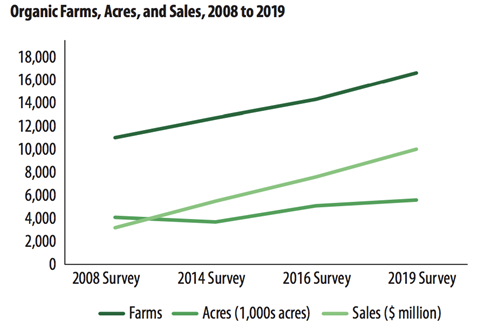

Demand for organic continues to defy expectations as consumers recognize its many benefits. Now new data underscore this trend. Organic agriculture saw a 31 percent increase in overall sales since 2016, according to the U.S. Department of Agriculture’s (USDA) National Agricultural Statistics Service (NASS) 2019 Organic Survey. The Organic Survey, conducted every five years, gathers information from certified or transitioning to certified organic farmers on production, marketing, and transitioning information pertaining to their organic operations. In addition to sales, the 2019 survey reports a 17 percent increase in certified organic farms and a nine percent increase in certified organic acres.

There were 16,585 certified organic farms in the U.S. in 2019, compared to 14,217 in 2016, with California (3,012), Wisconsin (1,364), New York (1,321), Pennsylvania (1,048) and Ohio (785) rounding out the top five states. A total of 5.5 million acres were in organic production in 2019 – a half million acre increase since 2016. The vast majority of farms (71 percent) have been in agricultural production for over 10 years, with 48 percent of certified organic farms in operation for over 10 years. 24 percent of organic farmers have been in operation for less than five years, a number which has increased since 2014 indicating a growing number of new farmers into the sector. This type of data benefits policy makers and advocates who seek to tackle challenges like an aging farm workforce, market challenges, and barriers to transitioning to organic production.

Improving Organic Data Collection

Last year NASS released the findings of its 2017 Census of Agriculture which found significant growth in the organic sector, including a 39 percent increase in certified organic operations and increased sales for organic products. Following the 2017 Census, the 2019 Organic Survey aimed to take a deeper dive into these trends, including estimates of organic crop production, costs, and management practices. Both surveys are invaluable sources of data for Congress, USDA and sustainable agriculture organizations to ensure there is an accurate reflection of the health of organic agriculture and emerging trends. The last Organic Survey was released in 2014. Note, the Certified Organic Survey was conducted in 2016 surveying only certified organic producers and does not include farmers or operations transitioning to organic.

NSAC submitted recommendations to NASS to improve the 2019 Survey. Our recommendations urged NASS to address several issues important to organic producers, including the challenges of organic contamination, organic production expenses, access to crop insurance and the availability of certified organic seeds. NASS incorporated many of these into the Survey, the results of which will help Congress and the agency determine the best policies to implement that will provide much needed support to organic farmers.

Here are some of the highlights from the 2019 Organic Survey:

Total sales of organic products rose to $9.93 billion, an increase of $2.37 billion, or 31 percent, from 2016. Among states, California grossed the most organic sales with $3.6 billion (36 percent) of the U.S. total and a staggering four times that of any other state. Washington state ($886 million), Pennsylvania ($742 million), Oregon ($454 million), and Texas ($424 million) follow California and round out the top five states in organic sales. Eleven states averaged more than $200 million in organic products. The largest farms, which account for only 17 percent of all farms, accounted for 84 percent of all sales.

Farm Characteristics:

| Sales Class | Percent of Farms | Percent of Sales |

| < $10,000 | 11% | 0.1% |

| $10,000 – $99,999 | 38% | 3% |

| $100,000 – $249,000 | 22% | 6% |

| $250,000 – $499,999 | 12% | 7% |

| $500,000 + | 17% | 84% |

Among organic products, 58 percent of organic sales came from crops (field crops like corn) followed by vegetables and fruits. Livestock and poultry products (e.g. milk and eggs), saw a small increase of 12 percent, while livestock and poultry (e.g. broiler chickens, cattle) had a greater increase of 44 percent. Top commodities seeing the greatest increase in sales since 2016 include:

- Corn, for grain……………..+70%

- Broiler chickens…………..+49%

- Carrots…………………….+49%

- Spinach………………………+52%

- Grapes……………………..+52%

- Cultivated Blueberries……+104%

- Raspberries……………….+197%

- Turkeys…………………….+68%

Organic Performs Well at Local Markets

Organic also performed well in direct to consumers sales and local markets. The survey found that $2.04 billion in sales – 20.5 percent of all organic sales – were made directly to retail markets, institutions, and local/regional food hubs. Three hundred million dollars’ worth of organic products were sold directly to consumers at farmers markets, on-farm stores and stands, roadside stands, self-harvest, community supported agriculture farms, and online markets. Jams, meat, cheese, wine and other value-added products had $727 million in sales. Unsurprisingly, California led states in the amount of sales made directly to consumers, followed by New York, Oregon, Washington, and Vermont.

Production Challenges Continue for Organic Farmers

Despite the growing success of organic, many organic farmers continue to face production and marketing challenges. To get a better understanding, the 2019 survey asked farmers questions around their production practices, expenses, and economic losses. For the first time the survey asked specific questions around the purchase of organic feed, seed, and seedlings. The results show this continues to be a major expense for organic farmers. Costs have significantly increased for seed and feed since 2014. Nationally, expenses for non-certified organic seed stood at over $328 million in 2019 compared to $340 million for organic seed. Fortunately, more farms were able to source organic seed and feed (11,303 using organic seed vs 6,983 using non-organic seed).

The 2019 Organic Survey asked questions regarding the impact of unintended presence of genetically modified organisms (GMO) and, new to the survey, the presence of non-National Organic Program (NOP) pesticides on organic farms. The majority of farmers indicated they did not experience GMO contamination (15,248) or pesticides (15,339) on their farms, while many others stated they just did not know. For farms that did experience economic impacts from unintended GMO (125) and pesticide exposures (142) in 2019, the numbers affected slightly decreased or remained relatively the same since 2018. However, looking at prior data the number of farms experiencing GMO contamination increased overall since 2006. The 2019 data, however, do not quantify the economic impact of contamination so it is difficult to determine the financial burden of this on farmers.

Regulatory hurdles remain a major impediment for organic farmers with 54 percent of farmers reporting they have experienced regulatory challenges while 39 percent noted they experienced production challenges. These are marked increases since 2014 and may mean farmers are unable to access on-the-ground assistance from local state and federal agencies. It is unclear what these regulatory challenges were, but they could range from understanding NOP standards or application to federal programs. Thirty percent of farmers experience challenges accessing markets, with 38 percent unable to overcome market price hindrances. Given the increase in the number of farmers experiencing these barriers, much more needs to be done to determine why these challenges persist for organic farmers.

Increase in Transitioning Farmlands

Before a farm or field can be certified as organic it must undergo a three-year transition period during which time non-organic materials cannot be applied. Farmers are increasing organic production by transitioning more acres to organic. This is reflected by the survey data. Certified organic farmers transitioned 255,060 acres in 2019, the majority of which are located in Montana and California. This marks a 113 percent increase in transitional acres since 2014. Similarly, over 60,611 acres are being transitioned to organic by non-certified farms, compared to 50,688 in 2014. While 44 percent of organic farmers intend to maintain their current levels of production, 29 percent indicated plans to expand their organic operations.

Organic Production Practices

Organic farmers use a range of practices and tools to build healthy soil, conserve water, and manage pests without harmful toxic inputs. Most farms (65 percent) utilized sustainable and conservation practices that include buffer strips or border rows used to separate organic crops from conventional crops; animal and green manures; and conservation tillage, no-till or minimum till.

| Organic Practice | Number of Farms |

| Buffer strips or border rows | 10,796 |

| Animal manures | 9,160 |

| Water management practices | 7,880 |

| Green manures | 7,564 |

| Conservation tillage, no-till, or minimum till | 5,970 |

| Mulch or compost, produced or used | 5,737 |

| Planting locations planned, to avoid cross-infestation of pests | 4,962 |

Mixed Participation in Conservation Programs, Crop Insurance

The survey reports that 7,306 or 44 percent of organic farms participated in the National Organic Certification Cost-Share Program (NOCCSP) in 2019 – a 27 percent increase since 2014. NOCCSP provides farmers with cost-share assistance to certify their farms as organic, in compliance with the standards of the National Organic Program (NOP). The increase in participation signals the importance of the program’s utility to those needing to certify their operations. However, due to astonishing accounting errors made by USDA, NOCCSP is at risk of running out of funds unless Congressional action is taken.

Organic farmers also took advantage of the EQIP Organic Initiative Program which provides financial assistance to organic producers to implement and install conservation practices. Through EQIP Organic Initiative, administered by the Natural Resource Conservation Service (NRCS), farmers are able to develop conservation plans, establish buffer zones, plan and install pollinator habitat, improve irrigation, cropping rotations, cover cropping, and nutrient management to address resource concerns. A total of 1,323 (7.9 percent) certified organic farms were enrolled in the program in 2019 with 230,573 acres. This marks a decline in participation from 2014 where 1,673 certified farms enrolled in EQIP Organic Initiative.

Another important data set worth investigating is participation in crop insurance. Of the 16,585 certified organic farms with organic acreage, only 4,255 had organic acres enrolled in crop insurance in 2019 – just 25.6 percent of farms. This is a slight improvement from 2014 where around 20 percent of organic farms were covered by crop insurance. 2,392 organic farms had 100 percent crop insurance coverage while 234 had less than 25 percent coverage. With just over 25 percent of organic farms covered by some level of crop insurance, it’s critical that more options be provided to organic farmers. Unfortunately, farmers indicated that crop insurance was either too expensive (1,600), not available for their commodities (1,223), or that organic price elections were not offered for their commodities (158). Many farmers (2,165) said they were not familiar with organic crop insurance while 115 said their insurance agent was not familiar. Almost 45 percent (7,478) indicated they did not need or want crop insurance.

The Takeaway

The data reflected in the 2019 Organic Survey show that even though organic sales and acreage continue to grow across the U.S., much more regulatory and policy support is needed to support this growing sector. Organic agriculture is here to stay, and farmers deserve access to production and marketing resources that will help their farms be successful. We hope that NASS and USDA maintain their commitment to organic by continuing to conduct this survey and other organic data collection activities on a regular basis. The importance of data collected over time, which show trends, is critically important to policy makers and organic farmers. This information helps inform policy priorities and farmer decision making.

Additional survey results as well as the results of previous NASS organic surveys are available at www.nass.usda.gov/organics or in NASS’s online Quick Stats database.