To help regional food hubs to grow, it’s important to have data for baseline performance measures – data that can help assess successes, needs, and opportunities. A new report on food hubs released yesterday, July 14, 2015, provides just such data.

COUNTING VALUES: Food Hub Financial Benchmarking Study draws on 2013 data from 48 diverse and geographically-dispersed food hubs (out of 300 such food hubs and over 100 invited participants) in the nation. The study makes available—for the first time—comparative data on a sector-wide basis.

Published by NSAC member group The Wallace Center at Winrock International (The Wallace Center) in conjunction with the Farm Credit Council, Farm Credit East, and Morse Marketing Connections, the report was developed to both highlight factors affecting the profitability of regional food hubs and help them improve their profitability.

According to the USDA, “a regional food hub is a business or organization that actively manages the aggregation, distribution, and marketing of source-identified food products primarily from local and regional producers.” They’ve become a major focus of the USDA’s Know Your Farmer, Know Your Food Initiative as a promising way to help small and mid-sized family farms access larger markets such as grocery stores and institutional buyers such as schools.

By aggregating and distributing produce from a number of local farms, food hubs are better able to provide scale-appropriate services on both ends of the transaction, thus providing producers with increased market access and consumers with increased access to local food. In this study, all 48 food hub respondents sourced local product.

In addition, many food hubs have broader environmental and social missions, such as supporting small and mid-sized producers and helping improve food access to underserved communities, according to the USDA.

Like many local food marketing channels, regional food hubs have experienced tremendous growth in recent years – as large as 288 percent since 2006-2007 according to a recent USDA study.

The Counting Values study, building on experience from a pilot 2012 food hub benchmarking study, provides snapshots of the financial and operational aspects of the food hub business, providing information on food hubs’ sourcing, sources of revenue, financial position, customers, vendors, labor, and labor costs, and also providing brief comparative analyses based on profitability, size, age of hub, seasons in operation, profit goals, and sales channels.

The study also provides an example of how to use the findings to provide hub managers and owners with a business planning tool for economic sustainability. For low-margin businesses like food hubs and their conventional counterparts in perishable commodity products, efficiency appears to be key.

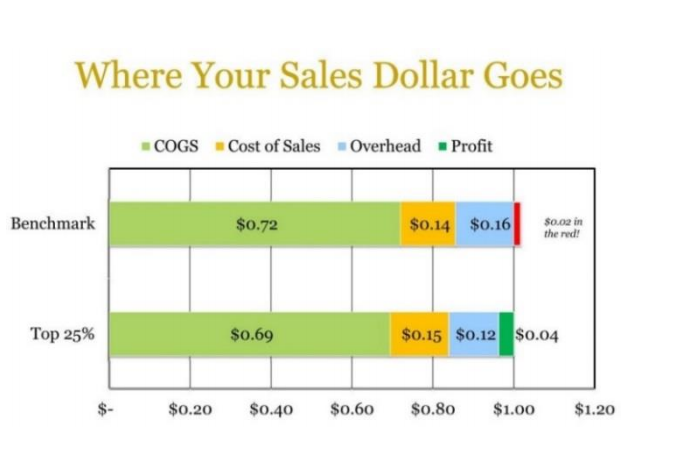

Profitability and Labor Costs

In terms of profitability, the typical food hub operates at a close to break-even level. The highest performing 25 percent posted a 4 percent profit, compared with the average of -2 percent. Within this relatively narrow spectrum, the most profitable food hubs were larger, older, for-profit operations. Those with sales greater than $1.5 million averaged profits of 2 percent, while food hubs 5 to 10 years in operation averaged a 1 percent profit.

On average, for-profit food hubs earned a 1 percent profit compared with not-for-profit food hubs, which posted -7 percent before taking into account grant income or contributions. Overall, profits ranged up to 25 percent of sales, showing what is possible in this industry.

The top 25 percent paid slightly more in income taxes and received far less in grants and contributions. While the top 25 percent spent less on Cost of Goods (for the acquisition and production, if applicable, of goods for resale) and Overhead (such as Office, management, IT, marketing, and owner labor), it spent slightly more on Cost of Sales than the typical hub.

The top 25 percent may have earned their 4 percent profit through 3 percent lower cost of goods sold (the cost of acquiring or producing goods sold) and through greater labor productivity. The top hubs spend 15 percent of sales on total labor, with the average hub spending just over 18 percent. These top hubs hired 11 FTEs (full time employees) while the typical hub had 6.5.

One interesting finding was that the cost of the average FTE was 39 percent higher in the top hubs (comparing cost per FTE), and those workers outperformed their peers by 56 percent (comparing sales per worker equivalent). Such efficiencies may be making the difference in keeping the top hubs competitive and sustainable.

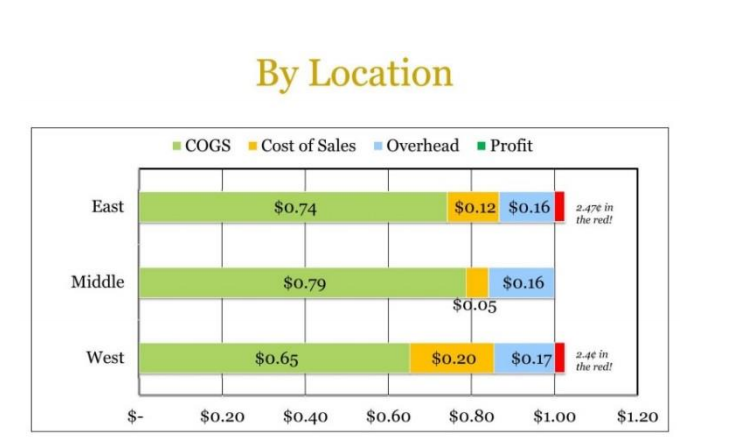

Profitability and Location

With 48 hubs, the study’s authors note that not enough participants were available to divide them into smaller regions to tease out noticeable contrasts. The participants in this study were spread across the entire United States, with solid representation from three regions: East, Midwest, and West. The study, therefore, noted differences for hubs in these three regions: the cost of product for hubs out West being much lower (as a percent of sales) than for hubs in the Midwest or in the East, while sales and distribution costs in the West were almost double that in the East and four times that in the Midwest.

Overhead was similar in all regions, and resulted in break-even performance in the Midwest and a 2.5 percent operational deficit in the East and West. Factors identified by the study as playing a role in these findings include distance to markets and sales competition.

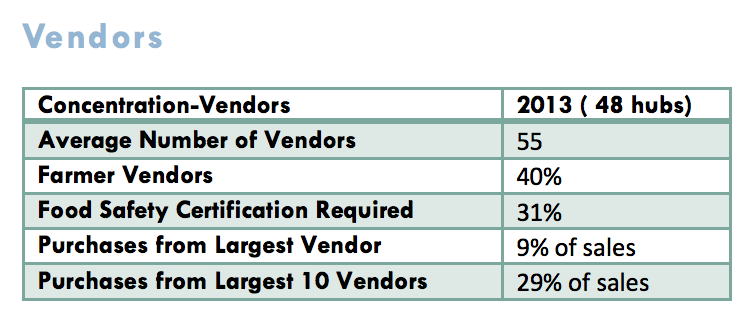

Profitability and Vendors

Typically having broader social and environmental missions while seeking to create economic value, food hubs are often built on more direct and intentional relationships with vendors. According to the study, one asset of the food hub’s value chain approach to supply (approaching vendors as partners rather than as purveyors of easily replaceable commodities) is that vendors are usually willing to participate in production planning with the hub. This allows food hubs to adjust its supply to meet buyers’ expected demand. A bonus is that producers appreciate the commitment and guidance of a customer (such as a food hub) willing to plan ahead to secure their product. The trust developed with its vendors (40 percent of whom are farmers) allows food hubs are able to come closer to optimizing value to all players in the system.

The need for more data on local food systems

As acknowledged by the study and by practitioners working in the local food system generally, there is a lack of reliable data on local food hub performance, both from a financial and an operational standpoint. According to the study, part of the reason for this is that the U.S. Department of Agriculture and other data collectors have traditionally focused on what farm product is being sold (such as grains, eggs, beef, etc.). Studying local and regional food systems requires a shift to track sales, volume, price, and other activity in the marketing channel of local and regional foods. Understanding how this market sector works is important, not just to farmers and food hub operators, but also to lenders, investors, and grant makers, who need to understand where the risks are at each stage in the value chain, and for the sector as a whole.

Back in September 2013, a food hub survey by Michigan State University’s Center for Regional Food Systems and the Wallace Center highlighted a lack of access to capital as among the challenges to food hub growth. Providing more data collection, tracking, and analysis on the participants in the local food system (and not just on its products) could help to address the access to capital challenges for food hubs.

For information on federal programs that can assist the development of the local and regional food economy, see NSAC’s Grassroots Guide to Federal Farm and Food Programs.