The federal crop insurance program is the most expensive program authorized in the farm bill, excluding nutrition spending, and is a primary driver of monoculture commodity production in the United States. Record-high taxpayer subsidies benefit private insurance companies and a small number of the largest commodity farms, while most farmers are unable to access insurance at all. NSAC believes that the 2023 Farm Bill is an opportunity to reform the farm safety net by capping wasteful crop insurance spending and investing in on-farm resilience.

The farm safety net’s lost purpose

For decades, the farm bill’s farm safety net has had the same goal: to provide farmers some degree of protection against unpredictable disasters or sudden price declines, allowing them to stay in business for another year while providing for family living expenses.

Today’s farm safety net includes permanently authorized commodity price and income support programs, disaster assistance programs, and the federal crop insurance program (FCIP). The FCIP was created in 1938 to help farmers recover from the Dust Bowl and the Great Depression, but it was used only sparingly for several decades. To incentivize participation, Congress expanded the program in 1980 and later 1994. The introduction of taxpayer subsidies to reduce both premium costs for farmers and operating costs for private insurance companies was one of the most significant changes.

Highly subsidized crop insurance was supposed to be a cost-effective replacement to the free disaster coverage authorized under farm bills in the 1960s and 1970s. We see now, however, that this is not the case. An astounding $60 billion in ad-hoc disaster assistance – authorized outside of the farm bill to supplement permanent safety net programs – has been distributed since 2017 through the Market Facilitation Program, Wildfire and Hurricane Indemnity Program (WHIP), WHIP Plus, Coronavirus Food Assistance Program, and, most recently, the Emergency Relief Program.

The dramatic escalation of ad-hoc disaster relief spending that started well before the COVID-19 pandemic illustrates significant shortcomings in the structure of existing farm safety net programs. It calls into question the claim that modern crop insurance is effective when it has not, in fact, replaced the need for ad-hoc disaster payments as Congress intended. Moreover, much of this disaster assistance was concentrated in the hands of the largest and wealthiest farmers who arguably needed financial assistance the least, while struggling family farmers actively engaged in farming were too often left out.

The FCIP has long since diverged from its roots as a modest safety net, and the disparity is only worsening.

Insurance subsidies reach record highs

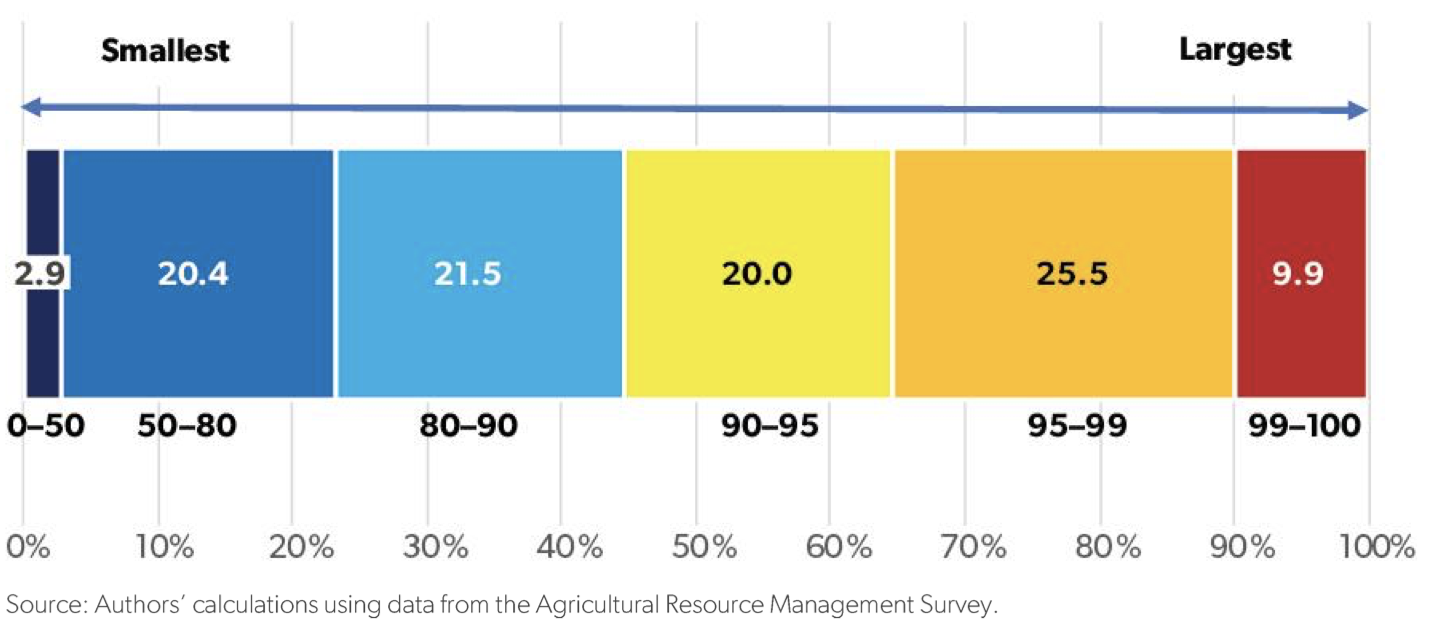

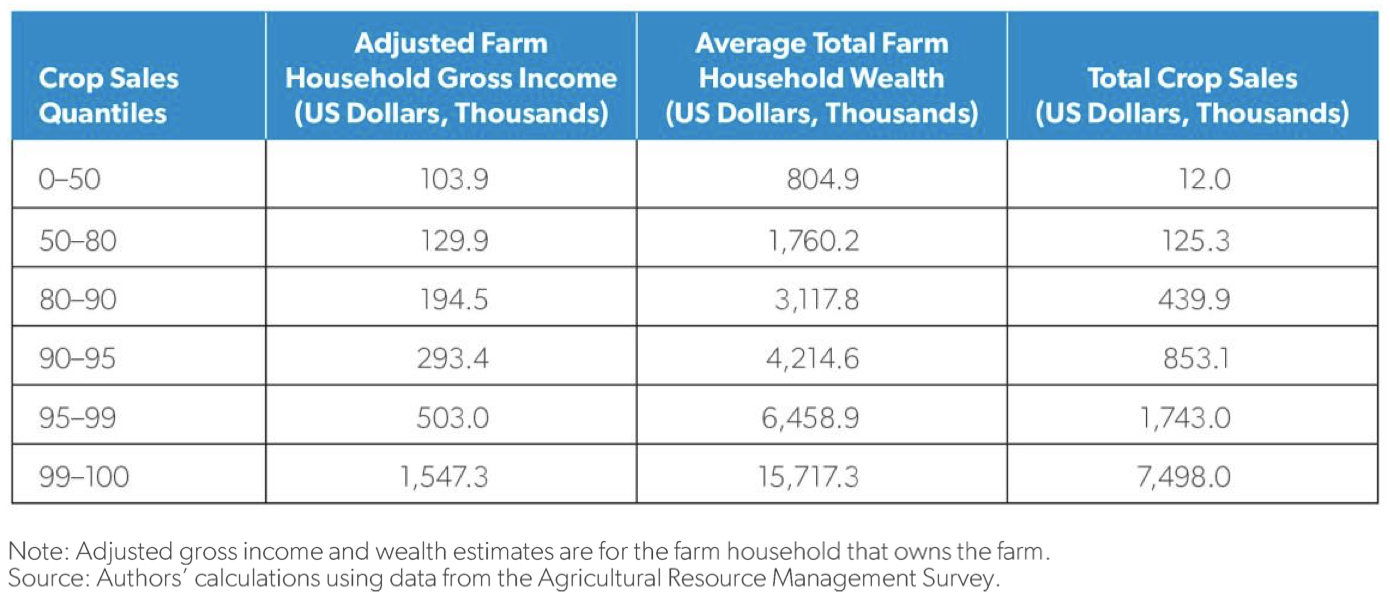

Today, the public pays on average 60 percent of a farmer’s premium costs. Farmers pay just 40 percent of the cost to purchase an insurance policy. Keep in mind that very few farmers are actually able to participate in the FCIP, even as more than 85 percent of planted acres for commodity crops (e.g., corn, soybeans, cotton, and wheat) are insured. This means that crop insurance subsidy benefits are heavily concentrated on the largest commodity farms, whose owners generally possess the highest levels of wealth and income.

These facts are illustrated in the figures below, as published in a recent paper: Who Receives Crop Insurance Subsidy Benefits?

Figure 1. Percentage Share of Total Crop Insurance Subsidies by Crop Sales Quantiles, Average, 2012-19

Figure 2. Farm Income and Wealth by Crop Sales Quantiles

The disparity is exacerbated because any farmer or landowner, even multi-millionaires and -billionaires, can receive unlimited premium subsidies. The FCIP is the only farm subsidy program without any means test or payment cap. By comparison, farmers with an Adjusted Gross Income (AGI) above $900,000 are not eligible to receive subsidies from Title I (commodity) and Title II (conservation) programs. Further (bar loopholes), Title I commodity payments are capped at $125,000 per eligible recipient, or $250,000 with a spouse.

This unchecked spending is only increasing – and drastically. For several years, the total premium subsidy was just above $6 billion per year. But in 2022, the total subsidy amount nearly doubled to $11.63 billion.

Elevated spending could, in theory, be justified if it meant the FCIP provided an expanded public benefit or coincided with a significant increase in farmer participation. But that was not the case, on either account. Instead, taxpayers funded the most expensive year ever to keep the crop insurance program afloat, in addition to record-breaking ad-hoc disaster assistance.

Figure 3. Crop Insurance Subsidies by Year

| Year | Subsidy $ (billions) |

| 2022 | $11.63 |

| 2021 | $8.61 |

| 2020 | $6.32 |

| 2019 | $6.37 |

| 2018 | $6.23 |

| 2017 | $6.36 |

| 2016 | $5.87 |

| 2015 | $6.01 |

In addition to premium discounts for farmers, Congress grants private insurance companies a guaranteed annual rate of return of 14.5 percent at the expense of taxpayers. The 2014 Farm Bill contains a provision that requires any future negotiation of the Standard Reinsurance Agreement between the federal government and insurance companies to be “budget neutral,” effectively prohibiting RMA the flexibility to negotiate a better deal for taxpayers.

In 2017, the GAO reported that this guaranteed profit exceeds what may be considered a reasonable amount for the public-private partnership and did not reflect market necessities. Money pocketed by insurance executives should be kept in taxpayer hands or used to improve food system resilience.

Triple-dipping is unsustainable

The fact that record-breaking subsidies are quietly allocated to bolster the FCIP on top of commodity support programs, and also on top of billions of dollars in ad-hoc disaster assistance, is in itself an indictment of the farm safety net. It should not be controversial to say that something is not working. This is especially true when taxpayer dollars disproportionately support crop insurance companies and the largest, wealthiest commodity farms while under-serving small and midsize farms, diversified operations, and beginning and socially disadvantaged farmers.

The present strategy to throw more money at the problem is not a solution. It will soon be impossible to sustain. We must continue to subsidize insurance premiums, but to a reasonable degree – and to a different end.

Industrial monocultures are, by definition, inherently high-risk operations that maximize efficiency in pursuit of yields at the explicit cost of necessary redundancies. These “conventional” operations (which are not only prioritized but incentivized through crop insurance rules) are particularly vulnerable to pathogens and natural disasters by virtue of their genetic uniformity. And chemical inputs, which are rising precipitously in cost, will only be able to negate the effects of rapid soil erosion for so long. In fact, farmers in the Corn Belt are already losing nearly $3 billion per year in harvest yields per acre.

In pursuit of efficiency, the farm safety net has consistently shifted the cost of risk mitigation from building resilient production systems onto the taxpayer. And it prioritizes farm operations that rely on federal programs for risk management and places others at a significant economic disadvantage, particularly for those who manage risk through diverse, integrated, and regenerative production systems, with significant benefits for our land, water, communities, and families.

This artificial removal of risk for conventional operations effectively eliminates incentives that a farmer may otherwise experience to innovate and build on-farm risk mitigation strategies into their enterprise, such as the adoption of soil-health practices and diverse rotations. Farmers should bear some weight of risk to experience these natural incentives, even as small, diversified farms should be able to access insurance to protect against unforeseen disasters.

In essence, the program should be stewarded back to its original purpose: to be a safety net, accessible in times of need by all farmers, not an open-ended entitlement program for the largest, wealthiest farms.

Congress must cap subsidies

To curb wasteful spending and to promote resilience in the food system, Congress must introduce reasonable caps on crop insurance subsidies in the 2023 Farm Bill. NSAC published a report in July 2022 which outlines several policy options to achieve this goal. These proposals would on average impact less than three percent of farms and save up to $20 billion in taxpayer dollars over 10 years. Savings in federal expenditures can be reallocated to improve the delivery of federal crop insurance and other high priority farm bill programs, reduce burdens on taxpayers, or reduce the federal budget deficit.

The following are opportunities that Congress should consider to level the playing field for farmers and taxpayers:

- Eliminate or reduce by 50 percent crop insurance premium subsidies for farms with an Adjusted Gross Income (AGI) above at least $750,000

- Implement a $50,000 payment cap on crop insurance premium subsidies for commodity crops, with a separate premium subsidy limit for specialty crops of at least $80,000

- Introduce a progressive cap on crop insurance premium subsidies for farms with a production value over $1 million up to $2.5 million.

- Eliminate restrictive language that prevents RMA from renegotiating with private insurance companies to reduce total government spending on subsidies and save taxpayer dollars.

- Prohibit crop insurance premium subsidies on land that USDA currently deems unsuitable for cropping.

The myth that caps will hurt small farmers

The most common argument against capping insurance subsidies is that it would destabilize the FCIP and hurt small farmers the most. Let’s break down this misleading claim.

First, understand that the FCIP relies on its “actuarial soundness” – a state of equilibrium where total indemnities that are paid to farmers in the event of a loss must equal total premiums, including premium subsidies, over time.

The argument in question assumes that introducing modest caps or a means test to crop insurance premium subsidies would inevitably force a significant number of farmers to abandon their policies and flee the FCIP. The FCIP would then raise premium costs to accommodate for lost income and maintain actuarial soundness, making insurance more expensive for small farmers. This is a baseless assumption – and not only because most small farmers already face insurmountable barriers to purchase insurance. The GAO released a 2015 report that projected minimal impact on the soundness of the insurance program if a means test were introduced, in part because so few crop insurance participants would actually be affected.

Remember that on average less than three percent of farms would be affected by any modest payment limitation. Those farmers who would see a discount ceiling are among those with the highest income or value of production and are thus presumed to be best resourced of any farmers to continue purchasing insurance – still discounted by tens of thousands of taxpayer dollars each year, if not more, but at a slightly reduced rate. Imagined defections from the program would likely be on principle, rather than means, but the risk of operating without any subsidized safety net would be great.

The crop insurance program may aspire to its original purpose once more by reinvesting savings into the farm safety net to make it more accessible to farms of all types and sizes. Congress should also use savings to invest in the adoption of on-farm risk mitigation strategies that both elevate soil health to reduce threats from worsening weather-related disasters and diversify market streams to protect against sudden market fallout. With farmers subject to fewer losses, these actions would meaningfully reduce the costs of the crop insurance program overall and dramatically limit the need for ad-hoc disaster assistance.