Last week, the exploitative business practices of multinational poultry processing companies – and the role of the Small Business Administration (SBA) in facilitating that exploitation – were put on display by a shocking report from the SBA’s own Office of Inspector General (OIG). The report reveals that SBA has in recent years made an increasing number of loans to large contract poultry operations, and that $1.8 billion worth of these loans were made illegally. It also highlights the extreme control that poultry companies, known as “integrators,” exert over chicken farmers.

The OIG report explains that the highly restrictive contracts under which contract poultry farmers operate mean that they are considered affiliates of the multi-national poultry integrators, rather than qualified independent small businesses. SBA is not allowed to guarantee loans for large poultry integrators or their affiliates.

In addition to going against SBA’s own regulations, the poultry contracts are often short-term even though the loan guarantees may span more than 20 years. Moreover, because poultry contracts are so restrictive, poultry growers take out loans without having any certainty around whether future actions by the integrator will force them out of business. These unbalanced terms mean that the benefits of the loans flow upward to the integrator, while effectively locking contract farmers into a treadmill of debt and putting taxpayers’ investment at risk.

The revelations of the OIG’s report reinforce the claims that contract farmers have been making about the exploitation and abuse that they face in their relationships with poultry integrators. It points to the need to both implement protections for farmers, and reform government loan programs to ensure that taxpayers are not subsidizing an exploitative system.

In the OIG’s own words: “The large chicken companies (integrators) in our sample exercised such comprehensive control over the growers that the SBA Office of Inspector General believes the concerns appear affiliative under SBA regulations […] This control overcame practically all of a grower’s ability to operate their business independent of integrator mandates.”

It is critical SBA takes this situation seriously, and that the agency works to quickly develop ways to rectify what is clearly a broken system. This Administration has made achieving fairness and fidelity in the contract poultry and livestock industry increasingly challenging after rescinding the Farmer Fair Practices Rules, and serious changes will need to be made in the weeks and months ahead.

$1.8 Billion in Questionable Loans

The impetus for the report came from the need to determine whether loans for poultry production facilities were properly meeting SBA regulatory requirements. The answer was: no. In all, the OIG found that over 1,500 loans made for poultry production facilities did not meet “regulatory and SBA requirements.”

Specifically, the OIG found that the farms in question were not in fact small business, but because of the highly prescriptive nature of the contracts, under which the farmers operate, were legally considered affiliates of the integrator. Poultry integrators are large, often multinational companies that own the genetics, chickens, and feed, but contract with farmers do the actual raising of the birds.

Between 2012 and 2016, the OIG found that SBA had made 1,535 loans relying on a 1993 opinion that the farms raising the chickens were independent small business; that determination was based on an analysis of a contract that SBA admits can no longer be found. As the report indicates, the chicken industry has evolved extensively since the 1993 opinion was made; what was a loan to a small, independent poultry farm in 1993 is now more frequently a loan to a large contract poultry producer affiliated with a large, often multinational integrator.

In its report, the OIG recommends that SBA review the 1,535 loans to make sure they followed the rules and regulations applying to affiliates. The report also directs SBA to reassess its procedures for evaluating the arrangement between the farms and integrators; changes to SBA rules on affiliates made in 2016 have now made the previously relied upon 1993 decision immaterial.

On March 15, 2018, Senator Cory Booker (D-NJ) offered an amendment to an SBA oversight bill, which the Committee subsequently passed, which requires SBA to report back to Congress on how it plans to address and resolve the issues highlighted in the OIG’s report.

High Risk to Farmers and Taxpayers

The vertically integrated model of the contract poultry and livestock industry effectively puts all the risk on the back of the contracted farmer, while siphoning off most of the profits for the corporate integrator. Despite the fact that the integrators control everything about a contracted operation (e.g., how the barns are constructed, how animals are raised, and how the farmer will be compensated), there are little to no guarantees about consistency or quality of service or inputs provided to the farmer. Many production contracts are made for an initial term of only a few years, after which the relationships become “flock-to-flock,” and the farmer loses any semblance of a guarantee that they will receive new chicks. Without a guarantee on the delivery and quality of new birds, the farmer is left not knowing month to month if they will be able to meet their substantial loan payments.

In the OIG’s examination of four recently defaulted poultry loans, they found that once the integrator reduced flock placements (longer periods between flocks resulting in fewer flocks over the year), withheld flocks (stopping delivery), or canceled a contract, the value of the facility dropped between 62 and 94 percent. Because chicken production barns are so highly specialized, they are basically worthless for any other purposes but storage.

The chart below from the OIG’s analysis shows just how important a contract and the continued delivery of birds is to a poultry operation.

The Loan Shift

SBA has two methods for guaranteeing poultry loans through the 7(a) program. Under the first method, SBA makes the decision regarding which loans will be guaranteed and which will not. Under the second method, known as “delegated authority,” banks use SBA criteria to determine which loans qualify for SBA guarantees.

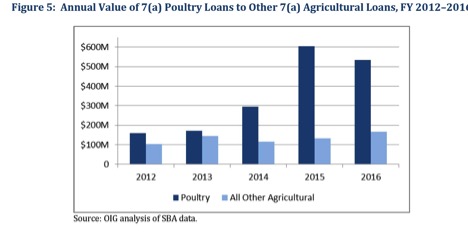

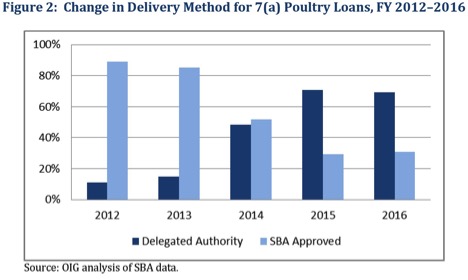

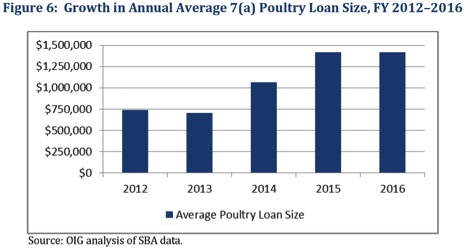

Prior to 2013, SBA approved the vast majority of poultry loans itself (89 percent in FY 2012, for example). However, it appears that after two banks, not named in the report, entered the market, a majority of SBA poultry loan guarantee determinations were made by lenders through delegated authority. “By FY 2016,” the OIG report states, “SBA directly approved 31 percent, which the clear majority of loans – 69 percent – being made by lenders under their delegated authority.” This delegation of authority also corresponded with an increase in loan maturity timelines, an increase in the average size of poultry loans (up 91 percent between 2012 and 2016), and an increase in the portion of 7(a) agricultural loans made up by poultry loans.

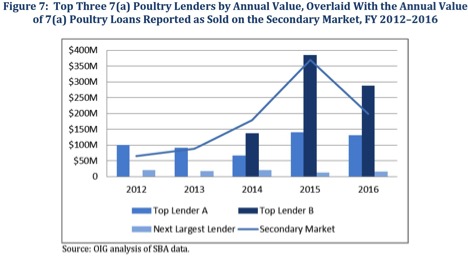

Two banks have made the vast majority of poultry facility loans between the reviewed period of 2012-2016.

Historically, the U.S. Department of Agriculture’s Farm Service Agency (FSA) was the primary lender to farms that could not obtain credit in the private market; however, that appears to have changed around 2012, when SBA began making many more contract poultry loans. This is likely related to the increase in delegated SBA lending mentioned above, but also to increased consolidation in the already vertically integrated contract poultry industry. As a result of vertical integration, the number of poultry operations has decreased and the size of operations has increased substantially. Instead of two-house systems, the large integrators appear to be moving to systems with more barns at the same location, which require larger loans to construct. FSA loans are limited to $1.4 million while SBA loans can be up to $5 million.

This trend is concerning because of the pressure it puts on federally backed loan programs – fewer, larger loans means less funding available for other applicants including beginning farmers, and farmers who have historically been discriminated against.

Next Steps

The release of this report has shed light on a historically shadowy contracting system, and pinpointed the ways in which SBA has been complicit in the integrators’ exploitative practices. Thanks to the transparency amendment brought forth by Senator Booker, SBA will now need to take action to respond to the issues raised in the report.

The revelations of the OIG’s report should also serve as a wake-up call to FSA. We hope that this will inspire FSA to take a hard look at its own lending standards and requirements to ensure that both farmers’ and taxpayers’ investments are being properly protected.