America is a nation of family farmers – nearly half of all production comes from small and medium-sized family farms. Like any small business owner, these farmers occasionally need infusions of relatively small amounts of capital to sustain and grow their operations, but often have trouble accessing funds through traditional lenders because of a lack of credit history or limited experience.

In order to better serve smaller farm operators as well as new and socially disadvantaged producers, the U.S. Department of Agriculture (USDA) introduced its Microloan program in January 2013. Just before the start of the new year, on December 30, 2016, USDA’s Economic Research Service (ERS) released a report analyzing participation patterns and the effects of outreach to farmers during the program’s first three years. Overall they found that USDA Microloans are going overwhelmingly to the program’s targeted group (small farms, beginning farmers and ranchers, veterans, and farmers from historically socially disadvantaged groups), are attracting borrowers new to USDA’s Farm Service Agency (FSA) direct loans, and that targeted outreach significantly increases program participation and acceptance rates.

About FSA Farm Operating Microloans

In response to advocacy by the National Sustainable Agriculture Coalition (NSAC), FSA officially launched its Microloan program in January 2013. The program was improved upon and expanded as part of the 2014 Farm Bill, with strong support from NSAC and our allies. The maximum size of the loans was initially set at $35,000 and was increased to $50,000 by the Agricultural Act of 2014.

The Microloan program was developed specifically to serve the credit needs of small farms, beginning farmers and ranchers, veterans, and farmers from historically socially disadvantaged (SDA) groups – but is technically open to all farmers. FSA is required by law to reserve a portion of its funds exclusively for farmers in targeted groups (50 percent of funds for direct operating loans (OLs) (both traditional and Microloans) are reserved for beginning farmers and 20 percent are reserved for SDA farmers).

Many of farmers in these subgroups have difficulty accessing credit through the commercial market, and may also find the application process for traditional FSA direct OLs to be too lengthy or cumbersome. In some cases, farmers from these groups might also be rejected for these loans because they cannot meet collateral, production history, or experience requirements. Programs like FSA’s Microloan program are important because they help cultivate the next generation of farmers by ensuring beginning and SDA farmers can access the credit and capital they need to sustain and grow their businesses.

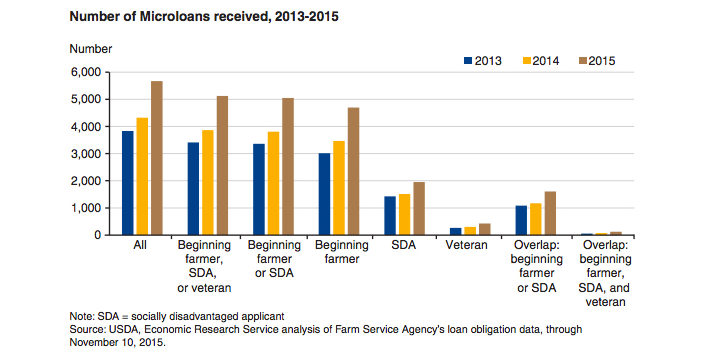

Between January 2013 and November 2015 (the time period covered by the ERS report) the Microloan program “grew from 3,833 loans with total loan obligations of $88.8 million in 2013 to 5,674 loans and total loan obligations of $162.2 million in 2015”.

FSA launched the Direct Farm Ownership Microloan program in January 2016. The new ownership program offers reduced application requirements, more timely application processing, and added flexibility for Youth Loan borrowers in meeting the farm experience eligibility.

Microloan Recipients

The ERS report, USDA Microloans for Farmers: Participation Patterns and Effects of Outreach, analyzes the composition of Microloan recipients and compared them with recipients of traditional direct OLs. The report also assesses the number and composition of new FSA DOL borrowers attracted by the Microloan program and analyzes the effect of targeted outreach on the program’s enrollment and acceptance rates.

During the course of the study period, January 2013 to November 2015, the Microloan program increased the number of loans it made by 1,841 and increased total loan obligations by $73.4 million.

Researchers were interested in determining to what extent the Microloan program was successful at serving its targeted audiences (beginning and SDA farmers and ranchers), and found that the targeted groups accounted for a strong majority of all Microloans during the survey period. According to the report:

- Farmers belonging to the targeted groups received 89 percent of all Microloans, of which beginning farmers accounted for the majority, at 81 percent. SDA farmers accounted for 35 percent of all Microloans – and 79 percent of those borrowers were also beginning farmers. Researchers also found that the targeted groups received a sizeable share of small OLs (82 percent), with 74 percent going to beginning farmers and 26 percent to SDA farmers.

- Between 2013-2015, Microloans attracted 8,182 borrowers who were new to FSA’s direct loan programs – substantially exceeding the 1,228 new borrowers who received small OLs during that time.

- New borrowers also received a much larger share of Microloans (59 percent) than of small OLs during the study period.

The success of the Microloan program at attracting new borrowers suggests that the program is servings its intended purpose. By offering smaller loans, a more streamlined application process, and more flexible requirements, researchers believe that the Microloan program has been able to attract new borrowers who would not otherwise have received traditional FSA direct OLs.

The report also analyzed Microloan recipients by regional distribution and commodity specialization and found that the most Microloans were made in states with large numbers of small and minority-operated farms, and that beef cattle operations received more than half of all Microloans.

Direct Outreach Increases Participation and Acceptance Rates

ERS was also interested in determining the effects of direct outreach on participation and acceptance rates within the program. To assess this, ERS collaborated with FSA and USDA’s National Agricultural Statistics Service (NASS) to conduct a randomized experiment in spring 2015 in nine southern states. Within the nine states, farmers in certain ZIP Codes received detailed letters describing the Microloan program and its benefits, while others did not. The experiment found that:

- The letters more than doubled the share of inquiries about the Microloan program at FSA county offices, from 2.64 percent to 5.54 percent.

- The share of borrowers receiving Microloans increased by 27 percent in ZIP Codes that had received the letters as compared to the ZIP Codes that had not.

The results from this initial experiment are promising and show the impact that outreach to farmers, especially beginning and SDA, can have. FSA and its sister agencies within USDA should seize upon these results and consider developing outreach plans for targeted constituencies across programs.

NSAC looks forwarding to continuing to work with FSA on this important program and to advocating for greater resources, outreach, and education for beginning and SDA farmers nationwide.

How To Apply

For more information on how to apply, visit FSA’s website or contact your local FSA office.