It has been almost eight years since the 2014 Farm Bill created the Whole-Farm Revenue Protection (WFRP) insurance pilot to succeed the Adjusted Gross Revenue (AGR) and AGR-lite programs. WFRP has been championed by the National Sustainable Agriculture Coalition (NSAC) for its potential to encourage diversification and level the playing field for producers underserved by other federal crop insurance options. Unfortunately, due to overly complicated rules, skepticism from some farmers, and disinterest from many insurance agents, WFRP is not performing near its optimal potential.

WFRP is a novel crop insurance product that offers producers nationwide the option to insure the revenue of their entire operation, including crop, livestock, and nursery production under a single policy. It also includes a built-in insurance premium discount for crop and enterprise diversification considering its inherent risk reduction impact.

Additional information about the program can be found on the NSAC Grassroots Guide WFRP webpage and the Risk Management Agency (RMA) Whole-Farm Revenue Protection webpage.

National Performance Trends

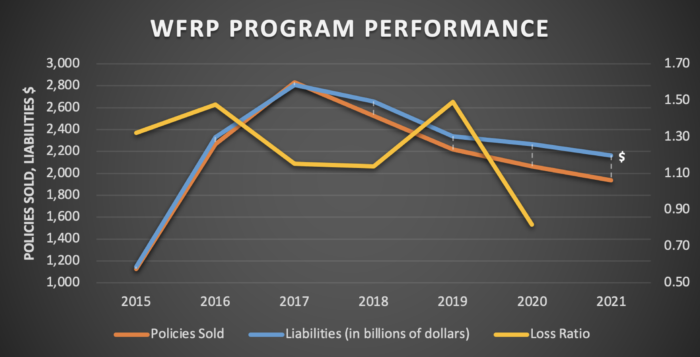

Today, national WFRP participation rates are low and enrollment trends are not favorable. Just 1,934 policies were sold to farmers in 2021, down by roughly 32 percent from the program’s height in 2017. This represents the first year that less than 2,000 WFRP policies were sold after the program’s inception in 2015. Likewise, the value of insured liabilities fell to a second all-time-low in 2021. Perhaps the only silver lining is that more policies were sold in 2021 than at the program’s height in a handful of states, including Florida, Georgia, and Mississippi.

From 2015 to 2019 the national WFRP loss ratio was consistently above 1.0, with a peak of 1.49 in 2019. A loss ratio higher than 1.0 over the long term reflects that a crop insurance policy is not actuarially sound, as the premiums invested into the system generate less revenue than the indemnity payments made to farmers. Though the loss ratio in 2020 at the time of writing is 0.82, this number will likely rise to be near, or surpass, 1.0 in the coming months based on previous experience. That lag is customary because indemnities for WFRP policies are not paid until after a farmer has filed their taxes, which can be in April or even later, following the insurance year.

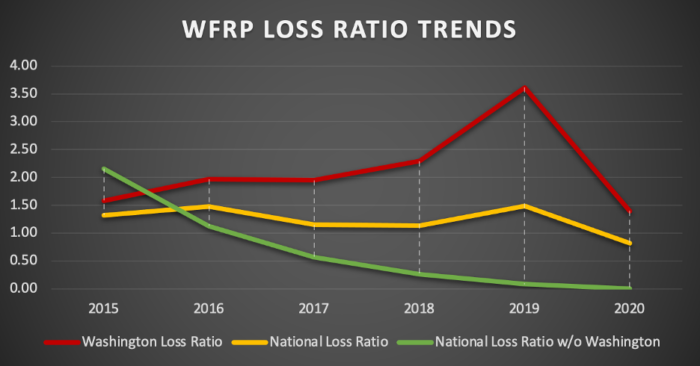

Each year, Washington state has the highest rates of enrollment – and among the highest loss ratios – compared to any other state. In fact, an average of 36 percent of total WFRP policies nationwide are sold to farmers in Washington. The average loss ratio in the state is 2.13, which reflects that indemnity payouts to farmers are on average more than twice the amount that the system receives in premiums to cover those costs. Most of these policies in Washington state insure apples and other fruit. Apple growers use WFRP because there are no crop-specific Revenue Protection policies for their primary crop.

Interestingly, the national loss ratio declines and stabilizes below 1.0 over time when Washington (as an outlier with high loss ratios) is removed from the calculation. In other words, WFRP demonstrates consistent actuarial soundness on average across the other 49 states. This phenomenon is represented in the graph below.

WFRP Challenges Explained

Without access to comprehensive on-farm WFRP data, explanations for declining enrollment and high loss ratios are necessarily limited. However, NSAC and our members collect testimony from farmers who consistently lament the program’s uniquely high paperwork burden. Farmers also report becoming disillusioned with WFRP after their indemnity payments are reduced at the time of claim. In addition, although the diversification premium discount is often cited as a draw to the program, highly diversified farmers routinely express concern that there is no significant discount beyond three commodities.

Farmers also routinely express an inability to find crop insurance agents who are willing to sell – or even have knowledge about – WFRP, despite the legal requirement for Approved Insurance Providers (AIPs) to sell the product. “I ended up educating my agents about WFRP, and I am not an insurance professional,” said one farmer at a listening session in January.

Another farmer said: “It is not just that they don’t understand, but in my experience, they are outwardly hostile to a different insurance program.”

While some agents fill a niche market by specializing in selling WFRP to farmers, this is rare. Many crop insurance agents are reluctant to sell WFRP because the compensation structure is based on total premiums, which considers the value of the crop, and has no connection to the actual time or expenses that an agent incurs in administering a policy. WFRP generally takes more time to write due to greater paperwork requirements and wide variability between farms when compared to an average, relatively cookie-cutter (and higher value) single commodity revenue program.

Another key barrier to broader adoption of WFRP is a regulation that impacts the entire Federal Crop Insurance Program: RMA’s definition of Good Farming Practices (GFP). Farmers must adhere to GFPs to be eligible to receive indemnity payments, and RMA currently maintains that a practice which reduces yields may not be considered a GFP. This is a serious deterrent against adoption of many conservation practices because temporary yield drags are customary on farms transitioning to climate-friendly, regenerative, and organic systems before yields can stabilize and even rise.

Read more about Good Farming Practices in an NSAC guest blog.

Changes to WFRP

The Risk Management Agency adjusts WFRP with the intent to improve the pilot each crop insurance year. The most recent changes implemented by RMA target a small portion of local food producers – in particular, very small farms and organic farmers that sell directly to consumers. These are important improvements, but they do not address the full set of challenges above.

For example, a new Micro Farm policy within WFRP eliminates the burdensome need for expense reporting and simplifies record-keeping requirements, but it is limited to farm operations that earn an average allowable total revenue up to $100,000. Of these, only direct market producers are eligible for the reduced paperwork burden. According to some estimates, 85 percent of farms producing for local systems fall into this category. But local food farms that earn a gross cash income above $350,000 account for 67 percent of local food sales, and these farms do not qualify for the Micro Farm policy.

Similarly, RMA increased the expansion limit from a flat 35 percent to the higher of $500,000 or 35 percent for certified organic producers and those transitioning to organic. However, organic producers were not uniquely constrained by the 35 percent ceiling to expansion when compared to non-certified or conventional producers, whose ability to expand their operations under this policy continues to be hampered at a flat 35 percent.

NSAC appreciates the changes that RMA is applying to expand access for a small group of producers. That said, we continue to believe that these are common-sense changes which should apply to all producers enrolled in WFRP, or at the very least all small and mid-sized producers. They would benefit greatly from the reduced paperwork burden and higher expansion limit which, at present, are benefits available only to micro farms and organic producers, respectively.

RMA maintains that more stringent requirements, and relieving said burdens for only a fraction of farmers eligible for WFRP, are necessary steps to improve WFRP’s inconsistent actuarial soundness. But the case for reform is bolstered by the loss ratio numbers presented above (with reference to Washington state as an outlier), suggesting that concerns about reforms harming the program’s actuarial soundness may be overblown.

In fact, the law of large numbers holds that courting more diverse and diversifying producers to purchase WFRP policies across the country should offset Washington’s high loss ratio and contribute to improved actuarial soundness.

Read our most recent recommendations to USDA, as well as an anonymous transcript from a 2021 farmer listening session about WFRP in this memorandum. You can find even more recommendations that NSAC shared with RMA in mid-2021 on our website.

What’s Next for WFRP?

The 2021 USDA Action Plan for Climate Adaptation and Resilience cites WFRP as a key program to support farmers who use diversification to reduce risk and combat decreasing agricultural productivity.

NSAC strongly agrees that WFRP can – and should – be an important tool to mitigate risk in the face of worsening weather-related risk and market uncertainties. Yet to fulfill this role, well-documented historical barriers to access must be overcome and the strengths of the policy must be fully leveraged.

NSAC is grateful for the opportunity to continue collaborating with the Risk Management Agency to improve WFRP. We are not the lone voice sharing these recommendations; language in the 2018 Farm Bill directs RMA to consider many of the measures outlined above to improve WFRP, as does the 2021 Feasibility of Insuring Local Food Production report commissioned by RMA.

In addition, our members and allies are coming to these conclusions through conversations and projects with farmers in the field, including a 2019 report from the National Center for Appropriate Technology (NCAT) which featured a comprehensive WFRP analysis: Is Organic Farming Risky?

With the next Farm Bill on the horizon, we are working with our members and allies to leverage this as an opportunity to supplement any actions which USDA takes to improve WFRP.