USDA’s Down Payment Loan Program has been around for over 20 years, and this post is the first in a two part series that examines the impact this program has had on growing new farmers over the past 20 years. Stay tuned for our second installment later this week!

Access to affordable farmland is one of the most significant challenges that new and aspiring farmers face when looking to start a career in agriculture. Whether trying to find land in California’s Central Valley or New York’s Hudson Valley, land access can often be a make or break issue for anyone with hopes of starting their own farm.

This was certainly the case for Joan and Nick Olson of Litchfield, Minnesota who always had dreams of someday starting their own farm, but were facing challenges finding a way to afford to purchase farmland. With all the challenges of farming, says Joan, “the greatest challenge was land access.” Like many young farmers today, the Olsons didn’t grow up on a farm and accessing credit to afford land through a traditional lender posed a major obstacle.

Fortunately, the Olsons were able to use a long-standing loan program offered by USDA’s Farm Service Agency (FSA) which allowed the couple to work with FSA and a commercial lender to obtain the loan capital needed to purchase the land for their farm. This Down Payment Loan Program (DPLP) only required the Olsons to provide a modest down payment on the farmland they were interested in purchasing, and provided very favorable interest rates on both the FSA and commercial loans.

This federal loan program is targeted towards farmers who traditionally face the greatest barriers to land access (such as beginning farmers), and was what allowed the Olsons to turn their farm dream into a reality. Joan and Nick now run Prairie Drifter Farm where they grow diversified organic vegetables and raise chickens and pigs on 33 acres in Litchfield, Minnesota. They run a Community Supported Agriculture (CSA) with over 100 members, sell directly to co-ops and markets in the area, and educate their customers about eating seasonally and regionally.

“We hear so often about the aging population of farmers,” says Joan, “and this program is just one more factor that can help us address that challenge,” by supporting those wanting to go into farming and funding the next generation of innovative farm enterprise. “And it’s a loan program – so the money comes back. The money can fund more farmers. It makes sense to invest in a program like this – to grow our food production in this country, and to keep and build our farmer base strong and diverse.”

Program Summary

The Down Payment Loan Program has assisted thousands of beginning and socially disadvantaged farmers in purchasing their first plots of farmland over the past 20 years. Developed and championed by the Center for Rural Affairs and the National Sustainable Agriculture Coalition, passed by Congress in 1992, and implemented by USDA in 1994, this loan program uses an innovative approach that creates a partnership between USDA’s Farm Service Agency (FSA) and a commercial lender or private seller in order to enable beginning, minority, and women farmers to make a down payment on a farm or ranch.

To qualify for the program, a farmer must provide a cash down payment of at least 5 percent of the total purchase price of the land to be acquired. FSA then splits the remaining balance with a private lender such as a commercial bank, Farm Credit institution or private seller. The new Farm Bill that was signed into law earlier this year increases the cap on the loan amount that FSA is able to finance to $300,000 which means the total value of farmland that can be financed through this program is $667,000.

For more details on the terms and interest rates for the FSA Down Payment Loan Program, refer to FSA’s webpage.

Program History

Over the past twenty years, the down payment loan program has made over 8,000 loans in 46 states and Puerto Rico. These loans have provided over $884 million in FSA funding that has helped beginning and socially disadvantaged farmers in purchasing their first farms. Given that FSA provides a maximum of 45 percent of the total purchase price, farmers received more than double that amount through the overall program over the past twenty years.

While down payment loans provide much needed assistance to beginning farmers looking to secure capital to purchase land, trends indicate that there is still work to be done to address geographic disparities in the distribution of loans throughout the country as well as the national decline in the number of beginning farmers. Further strengthening FSA field staff training, outreach to farmers, and partnerships with private lenders can help increase the number of beginning farmers throughout the country by providing beginning farmers with the opportunity to purchase land that they couldn’t otherwise afford.

Historical Lending Trends

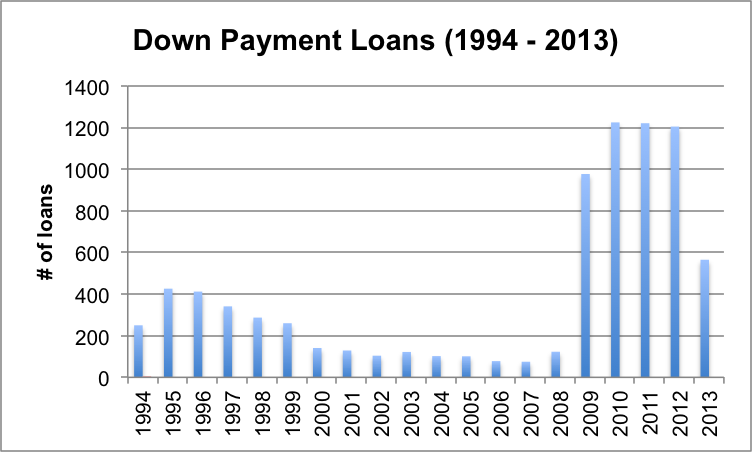

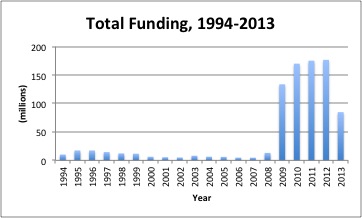

Funding provided through DPLP remained relatively constant and low for the first 15 years of the program, with the fewest number of loans made in 2007, totaling only $2.7 million – compared to its current levels of $85 million.

Much of the reason for the recent surge in popularity of this program over the past five years is due to important changes made in the 2008 Farm Bill, which reduced both the interest rate and the down payment requirement. Additionally, the 2008 Farm Bill allowed socially disadvantaged farmers to be eligible for the program in addition to beginning farmers – opening up a greater pool of potential farmer borrowers. Federal appropriations for FSA’s Direct Farm Ownership loans (which includes funding for Down Payment loans) also increased significantly in FY 2010.

The chart below clearly shows that the rate of growth of down payment loans (both in number and total amount) greatly accelerated after passage of the 2008 Farm Bill starting in Fiscal Year 2009. Due to timing of when federally appropriated funding was made available in 2013, the total loans made last year were significantly lower than previous years.

Between 2008 and 2009, loans increased by a factor of 8 and funding increased by more than 10, indicating an increase in the number and size of loans provided. Between 2008 and 2012 down payment loans gradually increased, then dropped in fiscal year 2013. Nearly half the loans made through the program have been made in just the past five years.

The number of loans and levels of funding varied from state to state, and the states that responded most significantly to the 2008 improvements were the states that were already providing higher amount of loans than other parts of the country.

State by State trends

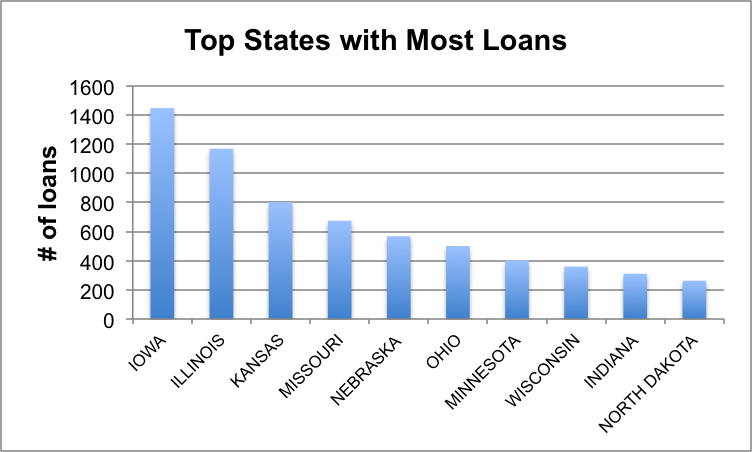

While the majority of states made fewer than 100 down payment loans to farmers over the past twenty years, there were a number of states that provided more. The states that made the most number of loans through this program were all located in the Midwest and Great Plains — including Iowa, Illinois, Kansas, Missouri, Nebraska and Ohio. Combined, these states provided more than half of all down payment loan funding throughout the country.

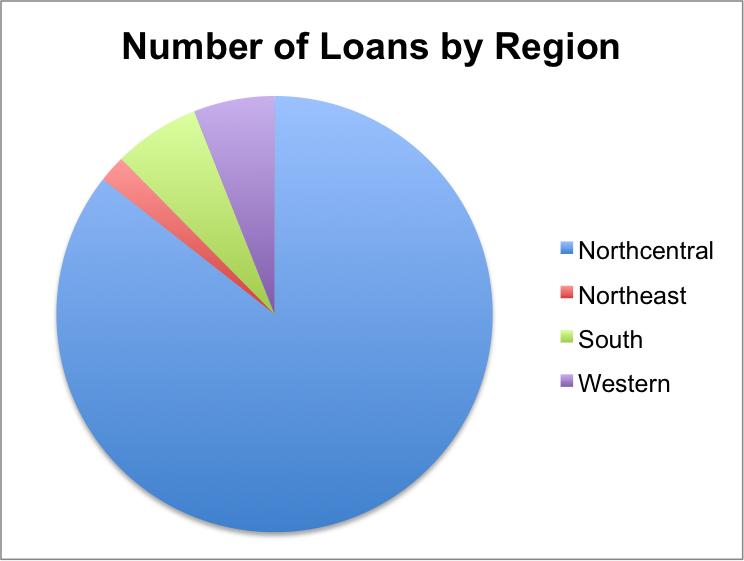

The vast majority of loans made through this program were made by states located within the North Central region — which accounted for over 85 percent of loans, totaling $766 million between 1994 and 2013. All of the top ten states that provided the most loans and the highest funding were in the North Central region.

Of the ten states that provided the most FSA funding for down payment loans over the past five years, six of those states (Iowa, Illinois, Minnesota, Indiana, Wisconsin and North Dakota) also had the lowest share of beginning farmers and ranchers in the most recent 2012 Census of Agriculture. While this is not representative of the how the percentage of beginning farmers has changed over time in these states, this may indicate that even though these states are successfully using this program, there is still room for improvement to increase the number of beginning farmers in this region. However, given that this region also has the youngest farmers on average than any other region across the country, it may be the case that this program has helped younger farmers get started earlier than they would if loan funding has not been available.

The ten states that provided the least amount of down payment loans were all from the Northeast, West, and Southern regions – with the Northeast states making the fewest number of loans. This is not all that surprising, given the smaller number of farms and agriculture in general in this region. However, many parts of the West and South are very agriculturally-based, which indicates that there is clearly room for improvement in these regions to increase the popularity and usage of this program.

In comparing this data with the average age of farmers throughout the country, regions that provided the fewest number of loans also have the oldest farm populations — such as the South and Western regions of the country. This disconnect between the average age of farmers and DPLP distribution throughout the country illustrates an unmet need for increased support to beginning farmers in regions where the farm population is oldest, and the greatest need for financial assistance to help more young farmers get started on the land.

The North Central region has the lowest average farmer age and also made the highest number of loans, while the other three regions have older farmers but have made fewer loans.

In comparing the number of loans provided and the number of beginning farmers and ranchers by region, the South stands out with over 40 percent of the country’s beginning farmers, and yet FSA offices in Southern states provided less than 6 percent of all down payment loan funding in the past twenty years. These numbers indicate that additional factors must be contributing to the high number of beginning farmers and ranchers in the South, particularly in states such as Texas, Missouri and Oklahoma, such as successful land transfers, land link programs, or innovative training initiatives.

The North Central region has the second largest share of beginning farmers and ranchers in the country (31 percent), perhaps indicating that the high number of down payment loans has supported beginning farmers in this region who are able to access the capital necessary for purchasing land.

The Northeast provided the smallest share of down payment loans throughout the country and also has the smallest number of beginning farmers and ranchers.

Increased efforts to raise awareness around DPLP are therefore critical in the Northeast, especially to promote the improvements that were included in the 2008 Farm Bill. The Northeast states did not show the same rapid increase following those changes as demonstrated throughout the rest of the country.

Farm Bill Changes

While the 2008 Farm Bill made several improvements to the Down Payment Loan Program, including lowering the interest rate, the most recent Farm Bill also contains significant changes that will hopefully improve the program and increase its popularity in the future. Prior to the passage of the 2014 Farm Bill, the maximum value of land that could be financed under this program was $500,000. Although this loan cap is higher than the cap on FSA Direct Farm Ownership Loans (which is $300,000), this restriction prevented many new farmers from using the program who were looking for farmland in areas of the country that have very high land values — including areas in the Northeast and around other urban centers that are under high pressure from development as well as other parts of the country where commodity prices have driven up land values.

The 2014 Farm Bill improves this slightly by increasing the value of land that can be financed to $667,000. Although this land value is much greater than FSA Direct Farm Ownership Loans, it is still likely to be not high enough to help some farmers finance their land purchases in certain parts of the country where land values are extraordinarily high.

Conclusion

USDA’s down payment loan program has been a long standing resource for new farmers over the past twenty years and will be a critical tool moving forward in addressing the aging farm population throughout the country by helping beginning farmers access their first plots of farmland. Over the past twenty years, FSA has provided over 8,000 Down Payment loans to aid farmers in purchasing land, predominantly in the North Central region of the country. As evident in the most recent Census of Agriculture, the North Central region has one of the youngest farming populations, which may be a direct impact of the success of this program in the region.

Joan Olson points out that the very nature of the Down Payment Loan Program means that the money will continue to come back to help support future purchases. “The money [that’s made available through this program] can fund more farmers. It makes sense to invest in a program like this – to grow our food production in this country, and to keep and build our farmer base strong and diverse.”

However, in looking at the geographic distribution of loans over the life of this program, it is clear that not all regions are benefitting equally or taking advantage of this critical resource for beginning farmers. NSAC has long advocated for this program and continues to urge USDA to institute a policy that would require FSA loan officers to first consider making a joint-financing loan that utilizes both FSA and private loan capital (such as through the Down Payment Loan Program), before making a loan that is solely financed with federally appropriate dollars. If USDA were to adopt this policy, federally appropriated loan funds would be leveraged with private capital and allow FSA to serve more farmers with the same amount of funding.

Stay tuned for our second post in the series coming later this week, illustrating the impact that this program has had on farmers across the country.