One hundred years after Congress first created the Farm Credit System (FCS), a national network of financial institutions owned by farmers and their cooperatives and focused on providing credit to farmers, FCS remains an important source of capital for young, beginning, and small farmers across the country.

Last week, the Farm Credit Administration (the regulatory body that oversees the FCS), released its annual report, which outlined lending trends to young, beginning, and small borrowers (YBS) across FCS institutions nationwide.

In 2015, FCS institutions increased their overall lending to YBS farmers both in terms of number of new loans and total capital made available. The biggest increase was to new farmers.

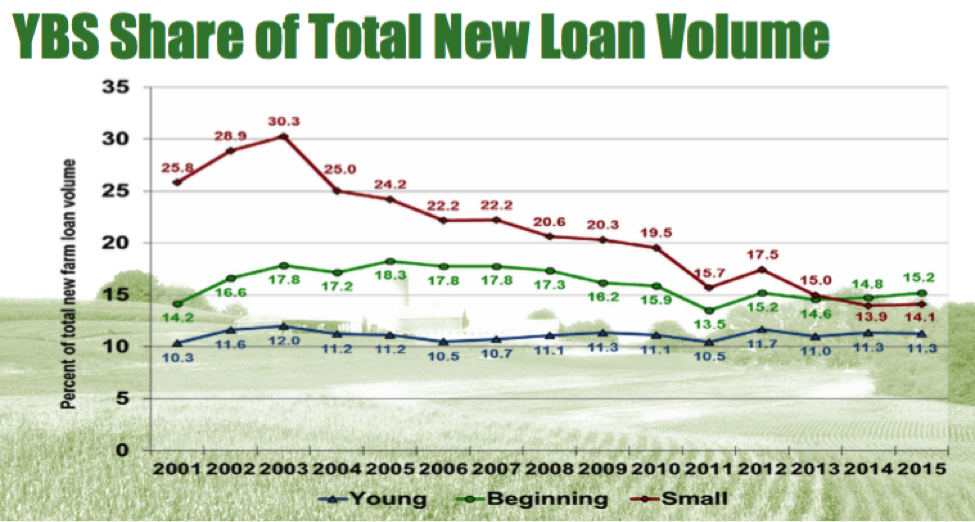

However, FCS has not yet shown progress in increasing the share of their lending portfolio that provides financial support to YBS farmers; the percentage of these loans to small farms has been in long-term decline, while loans for young and beginning farmer have remained stagnant.

About the Farm Credit System

FCS institutions are leaders in agricultural lending, holding roughly 40 percent of all farm business debt in the country. In contrast, the U.S. Department of Agriculture’s (USDA) loan programs support less than 5 percent of all farm loans; commercial banks and other lenders make up the difference.

FCS was established 100 years ago to provide farmers with access to the private capital they needed to finance their farm operations. In 1980, a statutory requirement shifted the focus of the FCS institutions, instructing them to better prioritize lending to young, beginning and small farmers (“YBS”) within FCS.

YBS includes farmers who are 35 or younger (“young”), have been farming for 10 years or less (“beginning”), and whose gross annual farm sales are less than $250,000 (“small”). The categories are not exclusive; many borrowers fall into two or even all three categories.

Report Findings

FCS is required to report on YBS lending trends annually, and recently released its report for 2015.

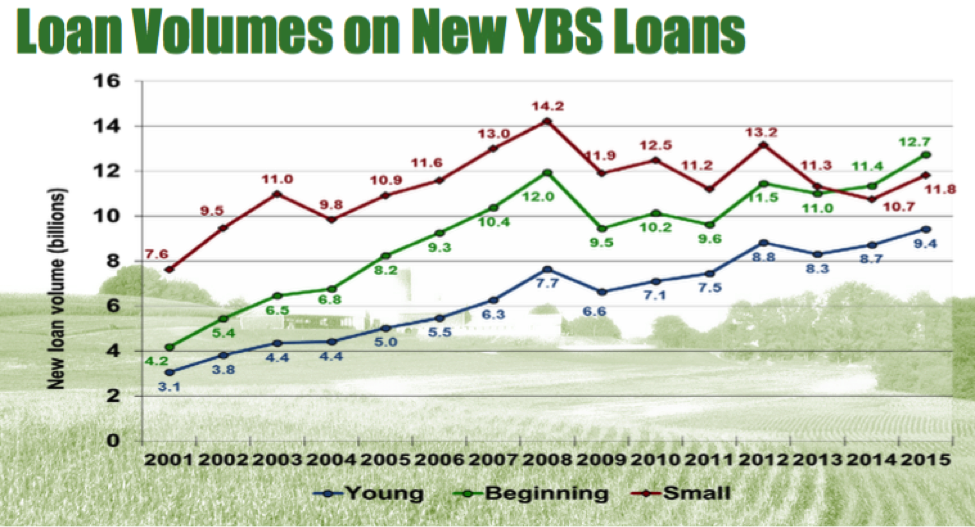

According to the report, in 2015 FCS significantly increased their loans to young, beginning, and small farmers – with the largest increase to beginning farmers, which was up 7.5 percent compared to 2014. Loans to small farmers rose by 6.7 percent, and loans young farmers rose by 5.1 percent. New farm loans for all farmers were up 3.7 percent.

The same trends hold true for the total new loan volume, which is the amount of capital financed by FCS through loans they’ve made. The largest increases were in total loan volume to support beginning farmers; up 12.2 percent compared with 2014. Loan amount totals to small farms were up 10 percent, and loan amount totals to young farmers were up 8 percent. Total new loan volume across the system rose by 8.8 percent.

In sum, these findings show that last year FCS not only made more loans to young, beginning and small farmers, but also that on average the loans were larger as well.

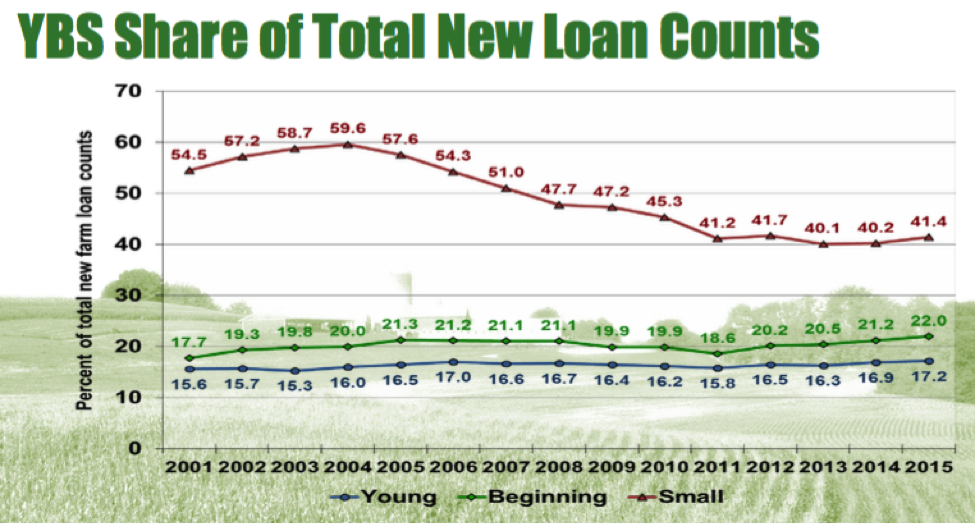

Roughly 40 percent of all FCS loans made in 2015 were to small farmers, with just under a quarter supporting beginning farmers and ranchers. Young farmers received slightly over 17 percent of all loans made by FCS last year. Again, the categories are not exclusive; hence the numbers cannot be added up, since the same borrower is typically counted in multiple categories.

While the trend of increased lending to the next generation of small-scale family farmers is promising, the total share of FCS’s YBS lending portfolio has remained flat over the past few years. In the case of small farms, loans have been declining since 2004, with only very modest increases in recent years.

In 2015, new small farm loans comprised just over 41 percent of all new loans made by FCS. However, while the total absolute number of new loans to small farmers increased by 6.7 percent, the share of FCS’s small farmer lending portfolio increased by less than 3 percent, up from 40.2 percent in 2014.

Looming Credit Squeeze

As we head into the height of the growing season, farmers across the country will be looking to farm loans to finance operating costs until they can sell their crops. These loans are especially important for beginning farmers, who are less likely to be able to draw on accumulated savings or other assets to cover upfront operating costs, or make up for shortfalls in revenue. Access to reliable and appropriate credit options is absolutely essential to ensure farmers – particularly YBS farmers – are able to succeed.

Focusing on YBS and next generation farmers will be especially important as USDA confronts their own expected shortfall in loan funding later this month. USDA’s Farm Service Agency (FSA) has less than $100 million remaining for the rest of the fiscal year to finance annual operating expense for farmers who are turned down by commercial lenders. Other lenders, like FCS, commercial banks, and Community Development Financial Institutions (CDFIs) will therefore need to fill in this gap in financing to ensure our nation’s farmers are able to access the credit they need to keep their farm business in operation.

It is good to hear that FCS has increased its numbers (both in terms of number of loans and capital) for new farmers, it will encourage others to join the industry.