Earlier this year, USDA announced a new microloan program that would specifically target the smaller credit needs of beginning farmers and other small farm operators selling to local and regional food markets. Launched in January 2013, the program has so far made over 3,400 loans in all 50 states, including the Virgin Islands, Puerto Rico, and the Western Pacific Territories.

Over the past nine months, local Farm Service Agency (FSA) offices across the country were able to provide over $66.8 million in micro farm loans to help beginning, minority, and small farmers pay for annual operating expenses such as seed and feed, rent and insurance costs, and minor improvements such as hoop houses. Many of these farmers have relied on high-interest credit cards in the past in order to pay for ongoing farm expenses.

As of the close of the fiscal year on September 30th, a total of 3,433 microloans were made, accounting for 25 percent of the total number of loans made by FSA through their Direct Operating Loan program. The number of loans made varied widely from state to state, ranging from one to 231 micro loans, and the average micro loan amount was $19,273. Some of the key findings from reviewing USDA program data for the microloan program include:

- Every state across the country made at least one microloan, but there is much room for further improvement;

- The Appalachia and Southern region in general are doing the best job reaching small and beginning farmers;

- Beginning farmers are finding this program to be a valuable resource and the microloan program is helping to bring these farmers into FSA offices for the first time; and

- More outreach is needed to minority farmers across the country.

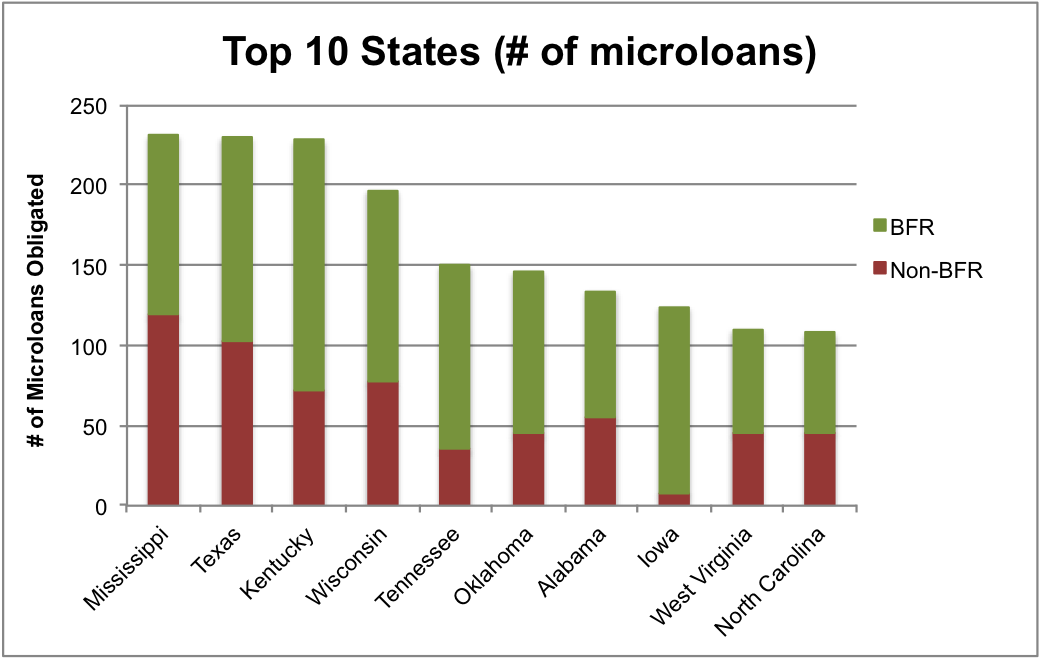

States Making Highest Number of Microloans

While the vast majority of states made fewer than 100 microloans to farmers in their states, there were several states and regions that made more. At the top of the list, were six states in the Appalachian and Southern region, including Mississippi, Kentucky, Tennessee, Alabama, West Virginia and North Carolina. In total, these states accounted for almost a third of all microloans made in the entire U.S., which is perhaps not surprising given the high numbers of small farmers in this region. The average size of a farm across these six states is just 180 acres, compared to the national average of 418 acres.

In addition to these southern states, there were two Midwestern states (Wisconsin and Iowa), and two Great Plains states (Texas and Oklahoma) that also made a high number of microloans.

A particular congrats goes out to the FSA offices in these counties who managed to get the most number of microloans in the hands of farmers: Nowata, OK (43 loans), West Liberty, KY (39), Green, WI (33), DeKalb, AL, Mitchell, NC, and Bonham, TX (31), and Attala, MS and Tuscaloosa, AL (30).

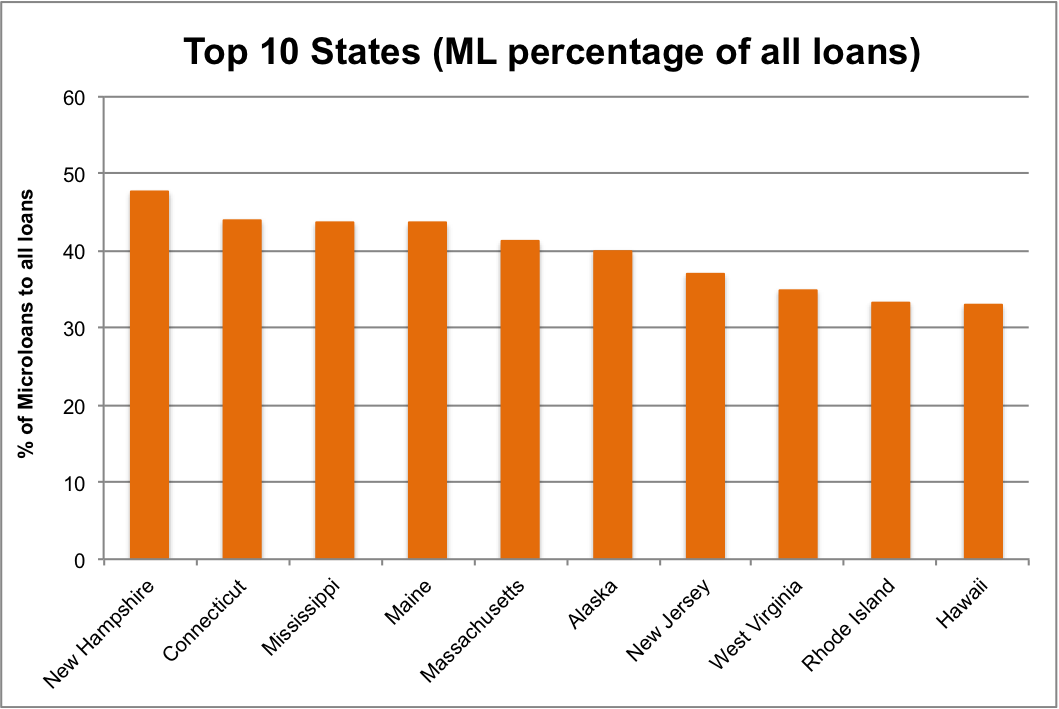

States Making Highest Percentage of Microloans

When looking at the number of microloans made as a percentage of the total number of loans made by FSA in a given state, only Mississippi and West Virginia remain at the top of the list in both number of loans and highest share of their state’s total lending portfolio. These states are clearly doing a great job not only training state and local FSA offices about how to administer this new loan program, but also in getting the word out to farmers.

When looking at the other states that made a high percentage of microloans, it is clear that the new microloan program as a great fit for New England. New Hampshire, Connecticut, Maine, Massachusetts, New Jersey, and Rhode Island all made over a third of their total loan portfolio to farmers through the microloan program, although these states typically made relatively few number of loans, with the exception of Maine and Massachusetts.

Geographic Disparities

While geographically, agriculturally, and demographically very similar, some states made far greater loans than other states in their region. For example, Alabama made almost 100 fewer loans than neighboring Mississippi, and similarly Minnesota made half the total amount of loans as Wisconsin, and Michigan and Ohio made roughly only a quarter. This may signal that some states are doing a much better job at reaching out to farmers or training FSA agents.

In general, many states in the Intermountain West and Great Plains made the fewest number of total loans and lowest percentage of microloans, which is not all that surprising considering that many of these farms and ranches are much larger in size and subsequently have much larger credit needs. Nonetheless, there are certainly smaller and beginning farmers in these regions as well, and NSAC will continue to work with our member groups in these regions and across the country to raise the visibility of this program to all farmers.

Beginning and Minority and Veteran Farmers

Although there is no explicit priority or set-aside for microloans made to beginning and socially disadvantaged farmers, given the often smaller credit needs for these farmers who typically operate smaller-scale operations, it is not surprising that over 68 percent of all microloans made this year went to beginning farmers. In total, over 2,300 beginning farmers benefited from this new streamlined loan program, and were able to secure over $44 million to invest in their up and coming farming operations this year.

The states that made the most microloans to beginning farmers include Kentucky, Texas, Wisconsin, Iowa, and Tennessee. For the majority of farmers that received a microloan this year, this represented their very first FSA loan – which is a clear signal that the microloan program is an excellent way for USDA’s Farm Service Agency to serve farmers who may not be able to secure credit from other sources.

Over a third of all microloans made this year went to socially disadvantaged farmers, which FSA considers to include “women, African-Americans, Alaskan Natives, American Indians, Hispanics, Asians, Native Hawaiians and Pacific Islanders.” However, only half of these loans – or 17 percent of all microloans – went to minority and tribal producers. The states that made the most microloans to minority farmers include Oklahoma, Alabama, Puerto Rico, Texas, Mississippi, Louisiana, Georgia and New Mexico.

There is clearly much room for improvement in conducting outreach to farmers of color about this new credit resource and being successful in getting more of these farmers in the door of FSA and applying for microloans. This has been a perpetual issue and one of the underlying reasons for the formation of the Outreach and Assistance for Socially Disadvantaged Farmers and Ranchers Program, which is unfortunately stranded without funding since the farm bill expired last fall.

Veteran farmers received 6.8 percent of all microloans. Texas, Mississippi, Alabama, and West Virginia led the way.

The Farm Bill and Microloans

While NSAC is generally very pleased with the success of USDA’s new microloan program to date, there are several legislative improvements that need to be made to the program as part of the farm bill that is currently being hammered out by congressional agricultural leaders from the House and Senate.

Statutory changes that are included in the House bill, but not the Senate, would allow FSA to better target these microloans to young, veteran and beginning farmers. The House bill would lower the interest rate on microloans to the same rate as the Down Payment Loan Program – a highly popular program among beginning farmers – and would also exempt microloans from the term limits that are placed on all other direct loans made by FSA. This would ensure that young farmers are not discouraged from seeking a microloan for fear that doing so would limit their eligibility in the future to receive much larger loans from FSA once they have established and grown their operations.

Perhaps the most important change included in the House farm bill is giving USDA the authority to partner with private, non-profit and other public institutions in order to take advantage of the expertise and technical assistance from NGOs, Community Development Financial Institutions, and State Departments of Agriculture who are already engaged in making microloans. One of the barriers that may be an obstacle for some local FSA offices in making more microloans is the ability of their already overextended loan officers to make and service their existing loans, let alone be able to provide the technical assistance to the increased number of first-time borrowers who would be attracted to microloans. The House provision would allow USDA to work with an intermediary lender to provide and service microloans, as well as provide technical assistance to borrowers and assist in outreach and financial education to prospective borrowers.

This provision is modeled after other successful programs that utilize an intermediary lender, such as the very successful Intermediary Relending Program and the Rural Microentrepreneur Assistance Program. Currently, USDA’s ability to expand and promote the microloan program is limited and goes hand in hand with total staff resources at the Farm Service Agency – resources which have been dwindling over the years as regional and local offices have been shut across the country. That’s why it’s critical to include the House intermediary language in any final farm bill that is reported from the Conference Committee, and to ensure that USDA’s fledgling microloan program is truly able to be successful and become a longstanding resource for beginning farmers in future generations to come.

To learn more about FSA’s microloan program, click here.