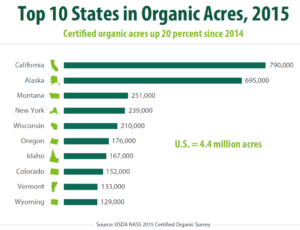

Organic acreage has increased 20 percent from 2014 to 2015, reaching about 4.4 million acres.

A closer look at the 2015 Organic Production Survey reveals that virtually all of the increase of 691,289 acres can be attributed to a single organic operation becoming certified in September 2015. Due to the addition of this large livestock ranch, Alaska shot from up from having around 300 certified organic acres to having nearly 700,000, second only to California in total certified acres.

While organic acreage did increase by a significant amount, the addition of this single livestock operation is not likely to impact the shortage of organic acreage in the United States that has lead to increased imports of organic crops.

Excluding Alaska, it is likely there were only a marginal number of new certified acres in 2015. However, this is still better news than last year when the 2014 Organic Production survey showed a decrease in organic acreage.

A Deeper Dive on the Acreage Increase

While the 2015 Organic Production survey found that organic acreage remained roughly flat if Alaska is excluded, organic sales increased 12 percent from 2014 to $6.3 billion. While this is much lower than the 72 percent increased reported in 2014, it still shows that as before, organic producers are becoming more efficient, producing more on fewer acres, or in some cases that organic prices are increasing.

If we dig a little deeper and look at the top five states for organic acreage in 2015, excluding Alaska, we find a mixed bag with some states experiencing a significant increase and other seeing a significant decrease.

- California – 685,848 to 790,413 acres, a 15 percent increase

- Montana – 317,878 to 251,531 acres, a 21 percent decrease

- New York – 210,871 to 238,700 acres, a 13 percent increase

- Wisconsin – 226,056 to 209,615 acres, a 7 percent decrease

- Oregon – 203,555 to 175,675 acres, a 14 percent decrease

With only two years of comparable data, one should not read too much into the numbers yet, but it does appear that a significant number of acres are moving back and forth between being certified and not certified, which is a potentially concerning trend given the time and effort that must be expended to become certified and the growing demand for organic products.

Organics by the Numbers

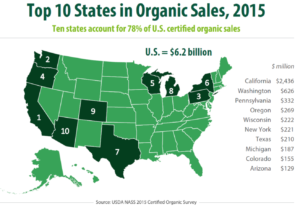

In 2015 organic sales at the first point of sale were $6.2 billion up from $5.5 billion, a 12 percent increase. While not statistically significant this is still a large increase in sales, and is testament to the growing demand for organic products. A majority of the increase, some $500 million, is credited to livestock and poultry products, mostly eggs and chickens.

The total number of Certified Organic Farms in 2015 was 12,818, down from the 14,093 reported in the 2014 survey. However, it must be noted, that while this survey is mandatory, discrepancies can exist between the survey and other sources, such as AMS’s organic integrity database. The Organic Integrity Database is currently showing 15,904 certified organic operations in the United States raising crops or livestock, and gathering wild crops.

Farmers are required to fill out the Organic Production Survey. However, the results are self-reported, so there may be discrepancies between this data and the National Organic Program’s List of Certified Organic Operations. These discrepancies may exist because some farms may have multiple certifications; the timing of the data collected, and survey responses. Check out this report on Organics in Texas for more information on the discrepancies between this survey and the Organic Integrity Database.

There was some movement in the top ten states for sales between 2014 and 2015. The top five remained the same – California, Washington, Pennsylvania, Oregon, and Wisconsin. However, the next five shuffled positions, with Arizona joined the top ten, taking the place of Iowa. All experienced an increase in sales, but some more than others. The top ten states represent 78 percent of total sales.

As in 2014, apples led the way in organic sales at $302 million, while milk again led the way for animal products at $1.174 billion, which is a small increase over the $1.1 billion posted for milk in 2014. Chickens and eggs, however, experience greater increases in sales, with organic egg sales increasing $312 million to $732 million and organic chicken sales up $48 million to $420 million.

GMO Contamination Impacts

The number of farms and the amount of the loss from Genetically Modified Organisms (GMO) contamination remained steady from 2014 to 2015 with only one more farm experiencing a loss and a total loss of just a few thousand dollars more than in 2014.

It must be noted that these are direct losses to individual farms and are self-reported.

These numbers don’t included any estimates about losses caused by loss of a market, such as was the case when non-approved GMO wheat was found in Eastern Oregon in 2013 or when China rejects shipments of grains because of the presence of unapproved GMO crops.

The survey does not address other types of contamination such as from drift of herbicides from fields with resistant crops, as has been occurring this year in soybeans. As well, it does not address the costs to organic producers incurred to prevent contamination. Most organic farmers employ buffers and other techniques to prevent contamination, which has a cost because they may have to take productive land out of production to create the buffer.

What About Transitional Acres?

The 2015 Survey found that current organic producers are transitioning 151,000 acres to organic production. This represents an increase of just 3 percent of the current level of organic acreage.

However, the Organic Production Survey is only distributed to producers that are currently certified, so does not count producers transitioning to organic that don’t already have certified acreage.

Transitional acreage is important because of the shortfall in organic production that has led to increased imports of organic crops. Demand for organics has been growing by double digits in recent years, but domestic production has not been able to keep pace.

It is quite likely there is significant acreage currently being transitioned to organic that is not captured by this survey.

Future of Organics Data Collection

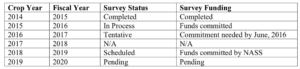

USDA has conducted six surveys of organic producers since 2007[1], but due to differing approaches on several questions these surveys cannot be fully utilized to identify trends in organic production and sales. It is important to have at least three years of comparable data in order to identify real trend. The acreage data issue discussed above is an example of how datum can very from year to year.

This is why it is important that the next administration continue the commitment to organic data collection by conducting regular and consistent organic production data into the future.

[1] 2007, 2008, 2011, 2012, 2014, and 2015