Editor’s Note: This is the second post of a three-part blog series detailing the outcomes of fiscal year (FY) 2016 direct and guaranteed loan data. This blog will focus specifically on beginning farmers and ranchers (BFRs) and their loan participation trends across the U.S.

In the early 1990s, the National Sustainable Agriculture Coalition (NSAC) led legislative efforts to direct credit resources from the United States Department of Agriculture (USDA) more towards beginning and socially disadvantaged farmers and ranchers. Adequate access to USDA loan and credit programs is critical for farmers – particularly beginning farmers and ranchers (BFRs), defined as farms where the principal operator has been farming for less than 10 years – who want to start, maintain, or expand their farming businesses but may have trouble obtaining financial assistance from the private market. Private lenders are historically more likely to see beginning farmers as “risky” investments; so BFRs rely heavily on USDA credit and loan programs. In FY 2016, 42 percent of all FSA loan obligations (21,234 loans totaling nearly $2.7 billion) went to BFRs.

Through USDA’s Farm Service Agency (FSA), farmers can receive direct loans, which come out of USDA’s funding pool, and guaranteed loans, which are provided by private agricultural lenders that are backed by USDA in the event that a farmer is unable to repay their loan. These USDA loan programs can help farmers address both operating and real estate expenses, and have funding pools specifically dedicated to supporting traditionally underserved farmers.

FSA sets aside a significant chunk of annual loan funding for BFRs: 75 percent of direct farm ownership loan funding is reserved for new farmers for the first eleven months of any fiscal year. This is the largest BFR set aside among all loans and perhaps the most necessary, considering the financial burden often associated with purchasing land. FSA also reserves 50 percent of direct operating loan funding and 40 percent of all guaranteed loan funding for beginning farmers.

Beginning Farmer and Rancher Loan Trends

Due to the downturn in the agricultural economy, demand for loans was markedly higher in FY 2016 than in FY 2015, putting FSA under pressure to increase financing to all farmers (established and beginning) in need of support. While overall FSA loan funding for BFRs went up, the increased demand from more established farmers resulted in BFRs receiving a smaller portion of total FSA loan financing than in previous years. In 2016, beginning farmers received 42 percent of all FSA loan funding, compared to 45 percent in 2015.

This downward trend is especially apparent for guaranteed loans, which tend to be larger in size and more popular with established farmers. Guaranteed financing for both real estate and operating costs for beginning farmers went down in FY 2016. BFR’s portion of guaranteed real estate financing dropped from 32 percent to 29 percent in FY 2016 and from 27 percent to 25 percent for guaranteed operating financing. This puts guaranteed lenders even further away from meeting their 40 percent target participation rate for BFRs, as set in statute. With direct loans, FSA did a much better job in reaching new farmers and meeting statutory targets – 63 percent of operating loan financing and 74 percent of real estate loan financing went to BFRs during FY 2016.

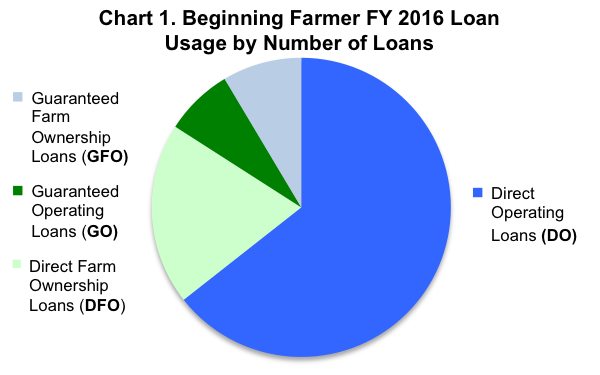

In terms of the number of loans, direct loans are more popular with BFRs as compared with guaranteed loans (see “Chart 1”), and made up 84 percent of all BFR loans in FY 2016. While the smaller set-aside for new farmer loans within the guaranteed loan program (40 percent, versus a 50 percent aside for direct loans) may be one reason BFRs prefer direct FSA financing, it more likely has to do with the challenge of accessing credit from commercial lenders.

BFRs were far more likely to seek operating loans over ownership loans. This isn’t surprising, as operating expenses are typically higher than real estate expenses for newly established farmers, who primarily rent farmland until they are financially prepared to purchase land.

Overall, the number of direct operating and ownership loans for BFRs increased by 4 percent, as did the total loan financing for BFRs through these programs. Though only a slight increase over FY 2015, this still speaks to BFR’s growing need for FSA financing.

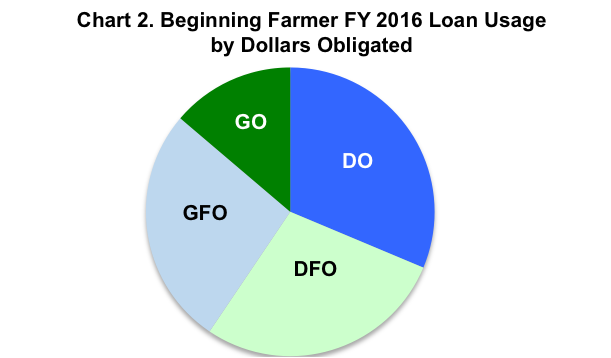

While a majority of the total loans made to BFRs were direct (see “Chart 1”), the total amount of financial support from guaranteed loans was significantly higher (see “Chart 2”). Guaranteed loans made up 40 percent of the dollars obligated towards BFR loans in FY 2016, yet only made up 16 percent of the number of loans. This means that while there were fewer guaranteed loans made to BFRs, these loans were much larger due to the larger loan amounts allowed for guaranteed loans.

Guaranteed Farm Ownership (GFO) loans played a particularly large role for BFRs in the context of loan values. The average Direct Farm Ownership (DFO) new farmer loan amounts to about $181,000 per loan, while GFO new farmer loans average about $395,000 per loan – nearly twice as much. Similarly, while BFRs received an average of about $62,000 for a Direct Operating (DO) loan, they received an average of $236,000 for a Guaranteed Operating (GO) loan.

This stark contrast between direct and guaranteed loan amounts suggests that guaranteed loans are likely going towards larger farm expenses and are associated with larger and more capital-intensive farm operations. Private agricultural lenders are far more likely to invest in large-scale livestock operations, including those that require farmers to take on massive amounts of debt and loans. Confined animal feeding operations (CAFO) not only siphon funds away from smaller and BFR-run operations, they also pose a significant threat to the environment and to the rural communities within which they reside.

Regional Analysis of 2016 Beginning Farmer Loans

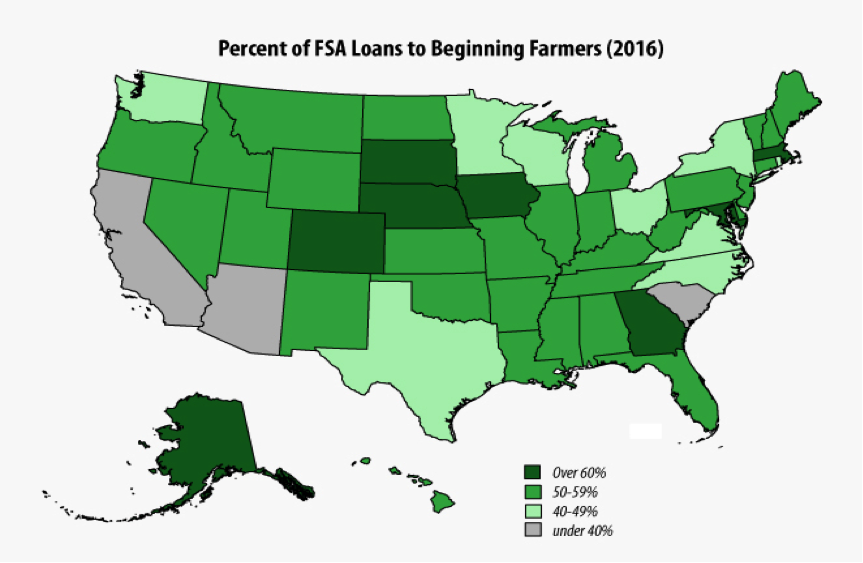

A regional analysis of BFR loan trends shows that not only is the overall percentage of loan funding to BFRs declining, but also that access to financing remains uneven across the country. The map below illustrates this trend and shows the regional disparities in BFR usage of FSA loans.

The data shows that the regions leading in FSA loan support for BFR include the Great Plains, Midwest, and parts of the South. States where agriculture is the dominate industry, including Nebraska, South Dakota, and Iowa, as well as Colorado and Georgia, also did a particularly good job in reaching out to BFRs in FY 2016.

However, there are still several states where FSA has struggled to connect with new farmers and ranchers. In Texas, BFRs received less than 50 percent of FSA loans, and in both California and Arizona they received less than 40 percent. In fact, California has the smallest percentage of loans to BFRs of any state in the country, with just 31 percent of all FSA loans made to BFRs. This is particularly concerning considering that in 2012 California was estimated to be home to nearly 16,500 BFRs. In FY 2016, California made only 269 loans to BFRs, reaching less than 1 percent of the state’s BFR population.

It is difficult to pinpoint exactly which factors are causing these trends. One possible explanation, especially for DFOs, could be the high price and low availability of quality farmland in California. It is safe to say though, that given the large amount of unused DFO funds ($500 million in DFO appropriated funds went unused in FY 2016; see our previous post for details) and increasing number of guaranteed loans being used to finance large operations, that significant opportunities exist for FSA loan programs to better serve new farmers of all kinds.

Our third and final blog in this series will be published shortly, and will analyze FSA loan data and trends for socially disadvantaged farmers and ranchers.

Thank you for your sharing, truly useful information