Editor’s Note: This is the second post of a 3-part analysis of FSA loan program usage throughout FY 2017. Stay tuned for our final post on lending trends for women and farmers of color.

Access to credit is a make or break issue for farmers, particularly those just starting out. Rarely do beginning farmers have the capital to purchase equipment, inputs, and land outright, so many turn to private banks or seek support from the U.S. Department of Agriculture (USDA).

Accessing financing from private lending institutions, however, often proves challenging for beginning farmers, who traditionally have little-to-no yield histories and minimal credit or assets. For beginning and other producers facing challenges to securing credit in the commercial sector, USDA’s Farm Service Agency (FSA) loan programs have proven particularly crucial.

In this post, the National Sustainable Agriculture Coalition (NSAC) analyzes a year’s worth of FSA lending data in order to identify how well these programs served America’s beginning farmers and ranchers in fiscal year (FY) 2017.

Primer on FSA Beginning Farmer Loans

In the early 1990s, NSAC led legislative efforts to direct more of USDA’s credit resources towards beginning and socially disadvantaged farmers and ranchers. Since then, USDA credit and loan programs have become one of the most popular means by which beginning farmers have been able to turn their farming dreams into a reality.

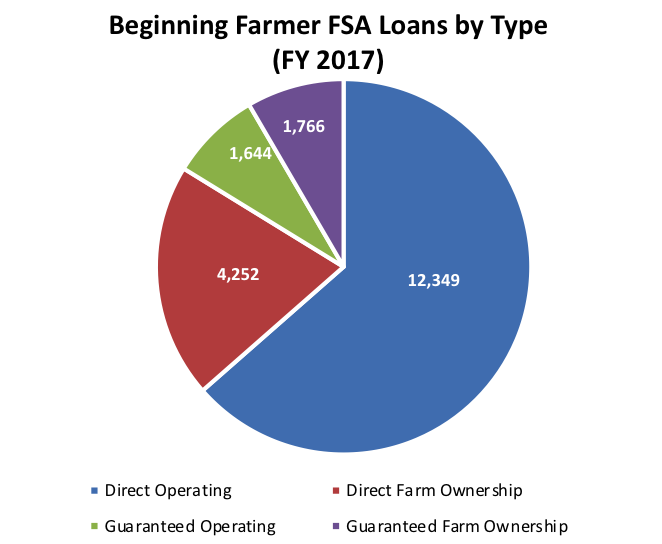

Last year, for example, nearly half of all FSA loan financing – $2.6 billion worth of operating and ownership expenses – was used to support over 20,000 beginning farmers across the country. This is an increase of two percent from the previous year.

Through FSA, farmers can receive both direct and guaranteed loans: direct loans are made directly by USDA, while guaranteed loans are provided by private agricultural lenders that are backed by USDA. These USDA loan programs can help farmers address both operating and real estate expenses, and have funding pools specifically dedicated to supporting traditionally underserved farmers – including beginners.

FSA is required by Congress to set aside a significant chunk of annual loan funding for beginning farmers:

- 75 percent of direct farm ownership loan funding is reserved until September 1 of each fiscal year. This is the largest beginning farmer set aside among all USDA loan programs, and has helped to ensure that beginning farmers are able to purchase their first farms even if they are turned down by a private lender.

- 50 percent of direct operating loan funding is reserved until September 1 of each fiscal year.

- 40 percent of all guaranteed loan funding is reserved until April 1 of each fiscal year

Beginning Farmer Loan Trends for FY 2017

- Beginning farmer loans and financing are down slightly from 2016

- Most beginning farmer loans are made directly by FSA

- Guaranteed loans are larger, more popular with established farmers

While beginning farmer loans represented a larger share of FSA’s total loan portfolio last year, overall, the total number of loans and related financing FSA provided to new farmers was down one percent compared to the previous year. However, it is important to note that overall FSA lending was also down last year, which would have contributed to a decline in total beginning farmer lending as well. Also worth noting, lending to beginning farmers actually saw a smaller decrease than the overall decrease across FSA loans (3 percent) and the decrease in total FSA financing (6 percent) from the previous year.

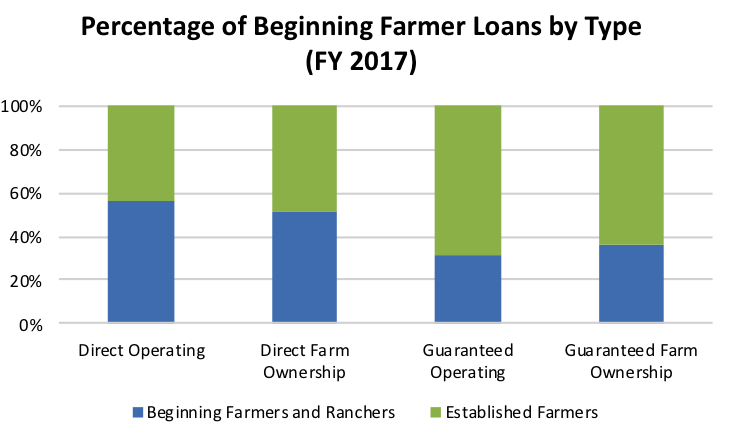

From our analysis, direct loans made by FSA continue to be more targeted to beginning farmers (see figure below) as compared with guaranteed loans, which are made by private banks. In total, direct loans made up 84 percent of all beginning farmer loans in FY 2017, which is similar to previous years.

Guaranteed loans, on the other hand, tended to be both larger in size and more popular with established farmers: just over a third (36 percent) of all guaranteed loans compared to twice that amount (61 percent) of direct loans supported new farmers last year. Moreover, the average guaranteed loan to a new farmer was $312,124, compared to $66,506 for a new farmer direct loan. These trends are not surprising given the important and unique role that FSA direct loans have played in financing new farm operations.

Since many new farmers have limited assets, production or business experience, or credit history, many commercial lenders consider loans to these producers to be riskier than those made to more established farms. For these reasons, direct FSA loans are considerably more popular than guaranteed loans among beginning producers (see figure below).

Beginning Farmer Lending Goals

- Guaranteed lenders are still falling short of meeting statutory lending targets

- FSA successful in meeting statutory lending goals

- Beginning farmer lending goals are still below 2015 levels

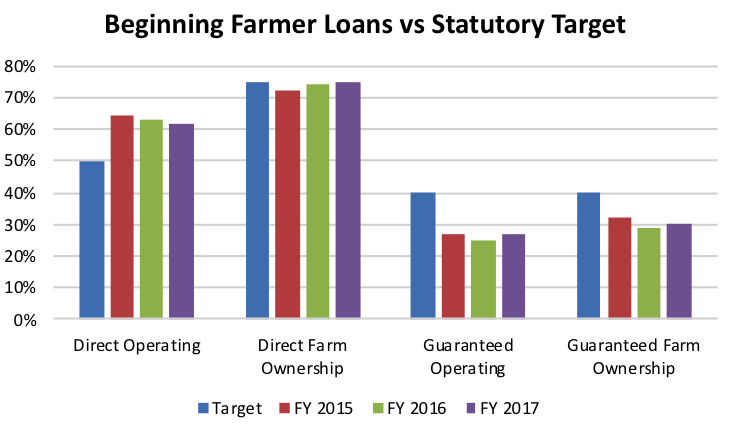

In FY 2016, the number of guaranteed loans to new farmers fell from the previous year, however, these same loans increased by 2 percent between FY 2016 and FY 2017. More specifically, the percentage of guaranteed real estate financing that went to new farmers increased from 29 percent to 30 percent in FY 2017, and from 25 percent to 27 percent for guaranteed operating financing.

While we are heartened that private lenders are extending greater amounts of credit to new farmers through FSA guaranteed loans, by and large, private lenders are still far from meeting the statutory lending targets for new farmers as required by Congress (see chart below).

With direct loans, FSA performed better than private lenders in meeting its statutory targets to reach new farmers, even though the percentage of operating loans made to new farmers is down slightly. In 2017, 62 percent of FSA’s direct operating lending portfolio supported new farmers, down one percent from the previous year. On real estate financing, FSA was successful in fully obligated the 75 percent of loan funding set aside for beginning farmers last year.

As shown in the chart above, FSA is doing better at achieving its statutory targets as of FY 2017. However, most of these financing goals are still below FY 2015 performance measures, signifying that guaranteed lenders in particular still have much work to do in properly serving the needs of new farmers.

Trends in Operating vs Real Estate Financing

- Operating loans are more popular with beginners than ownership loans

- Direct loans are in higher demand with new farmers than guaranteed loans

- Slight decrease in direct operating loans for new farmers in FY 2017

- Slight increase in beginning farmer guaranteed operating loans in FY 2017 despite decrease in overall loans

- Guaranteed loans to new farmers are larger on average than direct loans

FSA provides new farmers with loans for both operating and real estate expenses. In 2017, beginning farmers were far more likely to seek FSA loans to cover annual operating expense, rather than real estate purchases. The vast majority of these operating loans were made directly by FSA (rather than a guaranteed FSA lender), which isn’t surprising given that operating expenses are typically higher than real estate expenses for newly established farmers. In many cases, beginning farmers will rent farmland until they are financially prepared to purchase.

While direct operating loans remained most popular with beginning farmers last year, these loans also saw the most significant decrease in total loan obligations. Direct operating loans experienced a 5 percent drop in total financing to new farmers in FY 2017 as compared to FY 2016. On the other hand, financing for guaranteed operating loans were up one percent over the year before.

Direct loans followed trends similar to those seen for overall FSA loans, however, FSA guaranteed lenders actually increased operating loans to new farmers and decreased operating loans to more established farmers. Despite this positive change, as much as 40 percent of the dollars obligated towards beginning farmer lending in FY 2017 were targeted toward guaranteed lenders, yet only 16 percent of beginning farmer loans that year were guaranteed loans. This means that while there were fewer guaranteed loans made to beginning farmers, the loans that were made were much larger in FY 2017.

Lastly, we note that Guaranteed Farm Ownership (GFO) loans played a particularly large role in supporting beginning farmers in the context of loan values. While the average Direct Farm Ownership new farmer loan comes to only about $184,000 per loan (an increase of $3,000 from FY 2016), GFO new farmer loans average about $391,000 per loan – nearly twice as much. Similarly, while beginning farmers received an average of about $60,000 for a Direct Operating loan, they received an average of $226,000 for a Guaranteed Operating loan – a significant decrease from FY 2016 levels. Beginning farmer loan usage by dollars is displayed in the chart below for each of the loan types discussed in this section.

Regional Analysis of 2017 Beginning Farmer Loans

- Regional disparities exist in FSA financing for new farmers

- Production agriculture states lead in new farmer loans

- West and east coast states make the fewest loans to new farmers

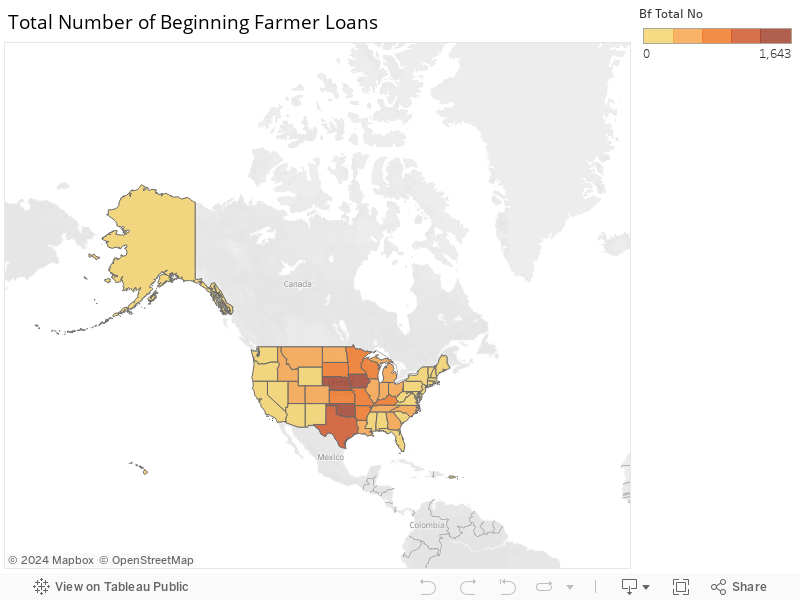

A regional analysis of beginning farmer loan trends shows that not only is the overall percentage of loan funding to beginning farmers increasing, but also that access to financing for new farm start-ups remains uneven across the country. This trend has persisted over the last few years.

As shown in the map above, the areas where production agriculture dominates are also those leading the country in FSA lending to beginning farmers: the North Central region (the Great Plains, Corn Belt, and parts of the Midwest), as well as Nebraska, Iowa, Oklahoma, and Texas.

The states making the fewest number of loans to new farmers followed general FSA lending trends, with the West Coast and Northeast (as well as parts of the South) making the fewest number of loans.

In terms of the percentage of loans targeted to new farmers in each state, the national average was 55 percent in FY 2017, compared to 54 percent in FY 2016.

States within the Great Plains (including Nebraska, Iowa, Missouri, and Arkansas) as well as states in South (Georgia) and Northeast (Maryland, Delaware) had the highest overall percentages of loans to new farmers. Over 62 percent of all FSA loans made to beginning farmers were made in those states.

There are, of course, still several states where FSA has struggled to connect with new farmers and ranchers. The states with the lowest percentage of loans to new farmers include California (28 percent), New Hampshire (22 percent), Arizona (32 percent), and New Jersey (34 percent). California has made some important progress, however, increasing the number of loans to new farmers from 21 percent in FY 2016 to 28 percent in FY 2017. While this is a promising trend, California’s higher than average land prices continue to be a serious barrier to beginning farmers looking to start operations in the Sunshine State.

Final Takeaway

It is clear that FSA loans remain an important source of financing for new farmers, although access to these loans remains uneven across different agricultural regions. Direct operating loans remain the number one USDA loan program serving new farmers, while guaranteed lenders are showing slight signs of improvement in scaling up lending to new farmers. Despite some positive trends, the data shows us that additional and targeted outreach is still needed to bring lenders into compliance with congressional lending goals.

Stay tuned for our third and final blog in this series, which will analyze FSA loan data and trends for women and farmers of color.