Editor’s Note: This is the first post of a 3-part analysis of FSA loan program usage throughout FY 2017. Stay tuned for subsequent posts on lending trends for beginning and socially disadvantaged farmers and ranchers.

Access to loans and credit lines are critical for farmers looking to start up a new operation, expand their operation, or even sometimes to help maintain current production. In order to help producers cope with the high levels of risk and constant changes that are inherent to farming – including fluctuations in market demand, weather, and input costs – the U.S. Department of Agriculture’s (USDA) Farm Service Agency (FSA) offers American producers both direct and guaranteed loans to help start, manage, and grow their businesses.

Direct loans are those made and administered directly by USDA, while guaranteed loans are made by private agricultural lenders with an assurance from USDA that the agency will provide up to 95 percent of a loss if a farmer is unable to pay back their loan. FSA loans, both direct and guaranteed, are specifically targeted toward farmers unable to obtain credit elsewhere (e.g., small production operations and beginning, minority, women, and veteran farmers). The majority of farm loans are made by Farm Credit or commercial banks, and within the agricultural lending sector, FSA holds roughly 8 to 10 percent of all farm debt in the U.S.

In this post, the National Sustainable Agriculture Coalition (NSAC) has compiled a year’s worth of data and analysis on FSA loans in order to better understand demand and usage in fiscal year (FY) 2017, and make informed recommendations regarding program improvements going forward.. This post is the first of a three part series.

FSA Loan Overview for FY 2017

FSA loans include both operating loans, which go towards farm maintenance costs and a farmer’s annual living expenses, and farm ownership loans, which help farmers seeking to expand or purchase their first farm to acquire land. Within these categories, loans can either be direct or guaranteed (as described above). Additionally, smaller-scale, beginning, and socially disadvantaged farmers are able to access a more streamlined loan application process through the microloan program.

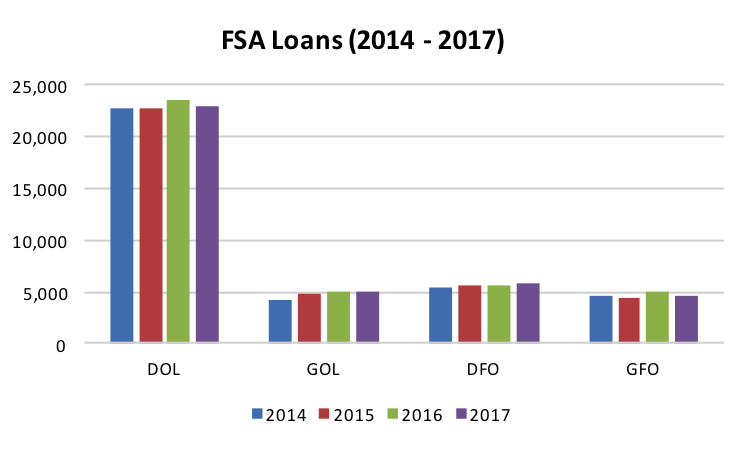

In 2017, roughly 38,400 individual farm loans, nearly $6 billion in farm expenses, were made or guaranteed by FSA, which is down slightly from 2016. The unexpected surge in demand for FSA farm loans seen the prior year was driven largely by the significant drop in commodity prices, as well as the subsequent decline in farm revenue that followed.

Last year, FSA and FSA guaranteed lenders decreased both the total number of loans made and the amount of financing provided to farmers across the country. More specifically, FSA made or guaranteed 3 percent fewer loans and provided roughly 6 percent less financing across all loan programs, as compared to 2016. The only FSA loan program that saw an increase in demand last year was the Direct Farm Ownership (DFO) loan program. In 2017, FSA provided 2 percent more loans to help farmers finance 3 percent more in total farm real estate purchases.

Although the farm economy has far from fully recovered, prices have at least stabilized, which have contributed to FSA loan levels falling last year to somewhat more normal levels. The fact that fewer farms started during the extended downturn in the farm economy likely also led to a decrease in demand, particularly for FSA operating loans.

Loan Caps – To Raise, or Not to Raise?

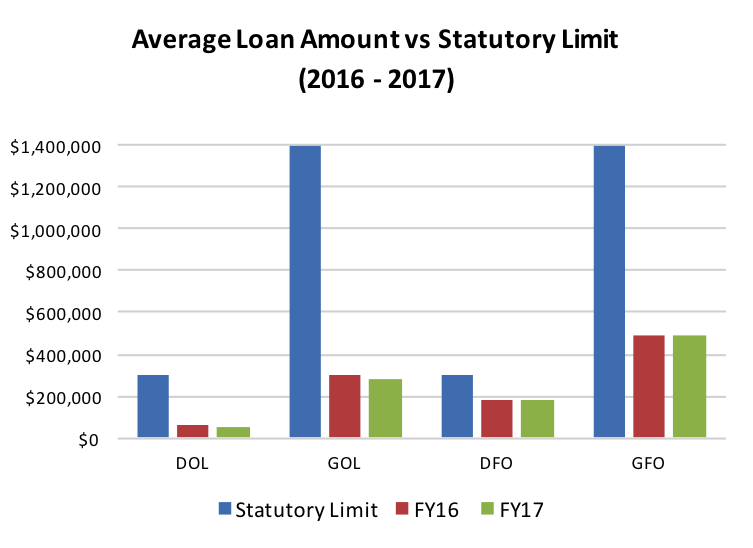

Across all FSA loan programs, the average loan was 3 percent smaller in 2017 than in 2016; Guaranteed Operating Loans (GOL) saw the largest decrease in average loan value (8 percent) during this period. The only loan program that saw an increase in the average loan size from 2016 to 2017 was DFO loans. Changes in average loan amounts by loan program are depicted in the chart below.

The maximum loan amount that FSA can finance or guarantee is set by Congress through the farm bill: $1.399 million (adjusted annually with inflation) for guaranteed loans and $300,000 for direct loans. The average actual loans made or guaranteed by FSA in 2017 fell far short of these maximum statutory loan limits (see table below). The only loan program for which the average amount was even close to approaching the statutory limit was DFO loans. These annual trends illustrate that most FSA loan programs (with the possible exception of DFO) are currently able to address the credit needs of the vast majority of FSA borrowers.

| Average FSA Loan Size – FY 2017 | |||

| Statutory Loan Cap | Average Loan Amount | Average as % of Cap | |

| DOL | $ 300,000 | $ 55,974 | 18.7 |

| GOL | $ 1,399,000 | $ 276,644 | 29.8 |

| DFO | $ 300,000 | $ 181,902 | 60.6 |

| GFO | $ 1,399,000 | $ 488,656 | 34.9 |

With the 2018 Farm Bill fast approaching, there has been much debate about how USDA loan programs should be improved to ensure that farmers have an adequate safety net, especially in times of low commodity prices. One proposal that has received particular attention over the past year is the option of increasing the statutory limits on FSA loan amounts.

Proponents of raising the loan caps (mostly commercial banks who rely on FSA to guarantee their riskiest loans), argue that FSA loan limits are too low to keep up with the increased costs of modern production agriculture. In reality, however, there has been excess demand for almost all FSA loan programs at the current statutory loan caps over the last few years. Furthermore, the average loan size for both direct and guaranteed loans is still far below the current statutory loan caps – and rather than increasing, is actually decreasing. None of these trends suggest there is any need to increase loan limits – with the possible exception of DFO loans.

USDA loans are a critical part of the farm safety net, and often the first step toward access to credit in private markets. They have filled an important gap in financing and has been vital in providing access to credit for small and mid-size family farms, including new and beginning, socially disadvantaged, veteran farmers, and others not well served by commercial credit. However, if loan limits are increased across the board in the next farm bill, the largest, more established farms would be the primary beneficiaries. This type of change, therefore, would be in fundamental conflict with the primary purpose of FSA loans – to serve those with the least access to private sources of credit and capital with a specific priority on providing financing to new farmers.

NSAC’s farm bill platform includes several alternative approaches to raising the loan caps that NSAC will be urging Congress to consider in any farm bill negotiations regarding how to strengthen and improve FSA loan programs.

Operating Loans – National Snapshot

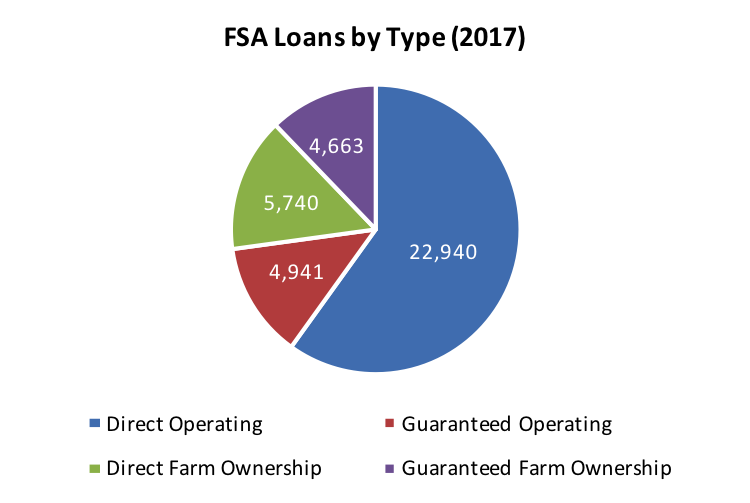

Following historic trends, the vast majority of FSA loans (73 percent) made or guaranteed last year were for farmers’ annual operating expenses (which must often be paid up front at the start of the season). The bulk of these loans were made directly by FSA.

Overall, FSA direct operating loans (DOL) have consistently represented the largest category of loans in terms of the number of loans made or guaranteed – 60 percent of loans in both FY 2016 and FY 2017. This is likely due to the nature of farming and seasonal cash flow and high demand for credit to cover annual farm operating costs. In terms of total loan funds, however, DOL only represent 21 percent of the total funding that FSA gets out the door each year. The majority of FSA loan funding actually goes not to DOL, but to larger farm real estate loans (discussed further below).

In 2017, farmers utilized FSA guaranteed operating loans (GOL) far less frequently, with only 4,941 loans made in FY 2017 compared to the 22,940 DOL loans made that same year. Both loan programs are down slightly from 2016, with 3 percent fewer direct and one percent fewer guaranteed operating loans.

On average, guaranteed loans are much larger than direct loans, due in part to the larger maximum loan amount set by Congress. The average GOL in 2017 was $276,644 (down 8 percent from last year) compared to $55,974 for direct FSA loans (down just one percent from last year).

Operating Loans – Regional Differences

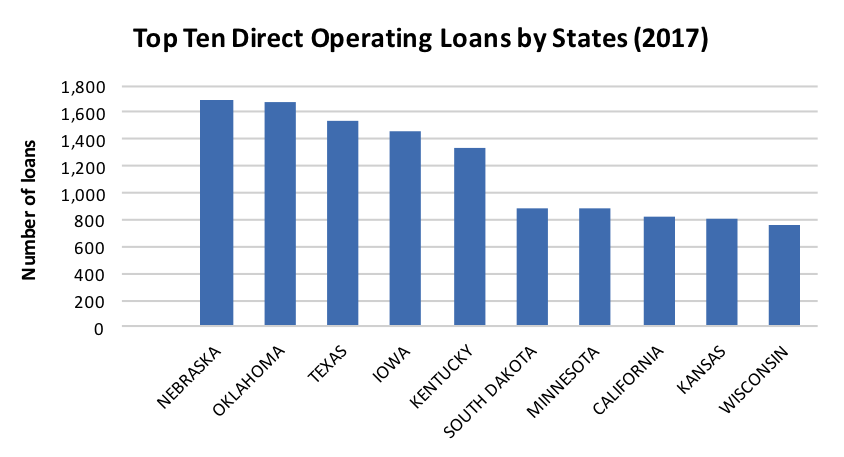

The regional breakdown of operating loans corresponds with the top agricultural states across the Midwest and Great Plains, with a few notable exceptions. California, for example, made 25 percent more operating loans in 2017 (compared to a 6 percent decrease nationally) and also moved into the top ten states making the most direct operating loans that year (see graph below).

Aside from the U.S. territories and Alaska, the states with the fewest number of operating loans are centered primarily within the Northeast, where agriculture is a smaller part of the regional economy.

Nationwide, FSA direct operating loans have been more popular with farmers than guaranteed loans made by private banks; roughly 4.5 times as many direct loans were made nationally last year versus FSA guarantees. However, in some regions of the country there are very few lenders utilizing FSA loan guarantees and these regions are therefore more dependent on FSA lending directly.

These regions include the South (MS, AL), Southwest (AZ, NV, UT), Northeast (NJ, RI, ME), Appalachia (WV), and territories and states outside the continental U.S. Many of these states are more rural, less populated, less agriculturally dependent, or lack the financing infrastructure necessary to extend guaranteed operating loans to farmers in the region. It is also notable that FSA directly made significantly fewer operating loans in both Alabama (-33 percent) and Mississippi (-16 percent) in 2017, compared to a 4 percent decrease nationally.

Unsurprisingly, the regional distribution does not change much in regards to the amount of operating expenses financed by FSA loans in 2017.

Farm Ownership Loans – National Snapshot

In terms of real estate financing, DFO loans made up the second largest segment of FSA loans, with 5,740 loans made in FY 2017. However, since farmland purchase values are generally a larger expense than annual operating costs, DFO and guaranteed farm ownership (GFO) loans are typically larger on average than operating loans. In fact, GFO loans in FY 2017 comprised the single largest category of loan funding – totaling 38 percent of all FSA loan funding, or $2.3 billion, similar to historic trends.

In 2017, the demand for farm real estate loans fell for guaranteed loans by eight percent and increased by 2 percent for direct loans; an interesting trend that warrants further analysis. On the one hand, it could signal that fewer banks are requiring a federal guarantee in order to finance new farm purchases – which is a good sign. On the other hand, it could mean that fewer established farmers are choosing to expand their operations or purchase land – with the exception being new farmers taking advantage of FSA direct farm ownership loans.

Farm Ownership Loans – Regional Differences

The map above represents the distribution of DFO loans made across the country in 2017. The largest concentration of DFO loans correlate to heavily agricultural states in the North Central and Southern Plains regions, and are being used to a lesser extent elsewhere. The under-utilization of loans is especially notable in the South (where predominantly minority farming populations are concentrated) and in the West (which includes many important specialty-crop producing states).

In the southern region, FSA financed just over 200 loans in total to help farmers buy farmland in Mississippi, Alabama, North Carolina, South Carolina, Georgia, and Florida. This compares to over 3,000 loans made to help farmers in the Great Plains and across the Midwest purchase farm and ranchland. This regional disparity highlights the inequitable access to credit that farmers of color in particular continue to face.

Guaranteed farm loans generally followed the trends of direct loans, but were more heavily concentrated in the North Central region, where more commercial agricultural lenders are also clustered.

Compared to other regions in the country, producers in the West (in California particularly) have experienced high barriers to accessing FSA farm real estate loans. Even though California leads the country in total agricultural sales, in FY 2017 only 51 direct and 63 guaranteed ownership loans were extended to farmers across the entire state. This total represents a 16 percent increase in FSA farm real estate loans over last year, but it is also important to note that even with the increase, these loans served less than a tenth of a percent of the state’s 81,500 farms (as of the Agricultural Census of 2012).

There are likely many factors contributing to the unbalanced level of lending in the West and in California specifically, the most significant being the $300,000 limit on FSA real estate loans. Farmland in California is valued at roughly $8,700 per acre, one of the highest in the country, and over the last year land values have increased roughly 10 percent (USDA-NASS). This means that the average farm in California comes with a price tag of about $2 million, according to the most recent Census of Agriculture. Clearly, $300,000 doesn’t go a long way for farmers looking to buy land in California, or in other areas with high real estate values, like the Pacific Northwest.

In 2017, FSA made fewer than 75 ownership loans in the Pacific Northwest states of Washington and Oregon. It’s quite likely that DFOs were not successful here due to the production of high value orchards, which command a sales price that exceeds the $300,000 maximum DFO loan amount. For reference, the average farm in Washington comes with a price tag of just under $1 million (USDA-NASS). With high land prices and inadequate loan offerings from FSA, farmers (in particular beginning farmers, who on average have less capital and access to credit) are left with very few options for financing a new farm purchase if a private lender turns them down.

In the Northeast, low FSA loan usage trends (most states had below 50 DFOs in FY 2017) can largely be explained by land availability and affordability. The Northeast has a concentration of smaller states with predictably small farming communities. Because of the pressures of development and urban and suburban sprawl, these small-scale and typically diversified farmers are often unable to afford or access financing to afford agricultural land.

Final Takeaway

FSA loans have become an increasingly important tool for farmers – especially new and socially disadvantaged farmers – however, their availability and use patterns do not correspond with producers’ needs. Many farming communities are unaware of and/or unable to tap into these incredibly important financial resources, especially in the case of farm real estate loans. While the trends identified in this post can be troubling, the analysis will be incredibly useful as we seek to better understand USDA programs and craft thoughtful recommendations for reform.

In our next post in this series we will take a dive deeper into the availability and impact of FSA loans on socially disadvantaged and historically underserved farming communities, including beginning, female, and veteran farmers, and farmers of color.

I’m currently applying for an FSA DOL as a socially disadvantaged farmer. Thanks for this article.