Editor’s Note: This is the first post of a 3-part analysis of the FSA loan program throughout FY 2016. Click here to see part 2 (on beginning farmers and ranchers) and here for part 3 (on socially disadvantaged farmers and ranchers).

Whether a farmer’s goal is to start up a new operation, expand their farm, or simply maintain their current production, farming is a demanding and capital intensive business. What’s more, this demand is often exacerbated by the high levels of risk and constant changes that are inherent to farming – including fluctuating market demand, unpredictable weather and climatic trends, increasing costs of inputs like seeds and fertilizers, and rising land prices.

In this way, loans remain some of the most important tools farmers can access to start, grow, or maintain their farming business and deal with agricultural, economic and government-based instability along the way. Recognizing the importance of financing for land and operating capital, the United States Department of Agriculture’s (USDA) Farm Service Agency (FSA) offers two critical loan programs to meet the credit needs of farmers.

FSA offers both direct and guaranteed loans to farmers. Direct loans are those made and administered directly by USDA. Guaranteed loans provide assurance to private agricultural lenders that USDA will provide up to 95 percent of a loss, if a farmer is unable to pay back their loan. FSA specifically targets farmers unable to obtain credit elsewhere, with a specific focus on the credit needs of small, beginning, minority, women, and veteran farmers.

In this post, the National Sustainable Agriculture Coalition (NSAC) has compiled a year’s worth of overview and analysis of the FSA loan program in order to better understand demand and usage of federal loan programs in Fiscal Year (FY) 2016. This post is the first of a two part blog series and will be followed by a deeper dive into beginning and socially disadvantaged farmers’ loan usage.

To see the progress that has made since FY 2015, refer to last year’s analysis blog.

FSA Loan Overview for 2016

FSA loans include both operating loans, which go towards farm maintenance costs and a farmer’s living expenses, and farm ownership loans, which help both beginning farmers and farmers seeking to expand their farm acquire land. Within these categories, loans, like the ones on RadCred, can either be direct or guaranteed (as described above). Additionally, smaller-scale, new and socially disadvantaged farmers are able to access a more streamlined loan application process through the relatively new microloan program.

Since 2015, FSA increased both the number of loans made and the amount allotted for these loans. FSA administered five percent more loans in FY 2016, amounting to a 12 percent increase in total loan amounts – from about $5.7 billion to $6.4 billion. This pattern continues the trend in recent years and reflects increased demand for federal farm financing.

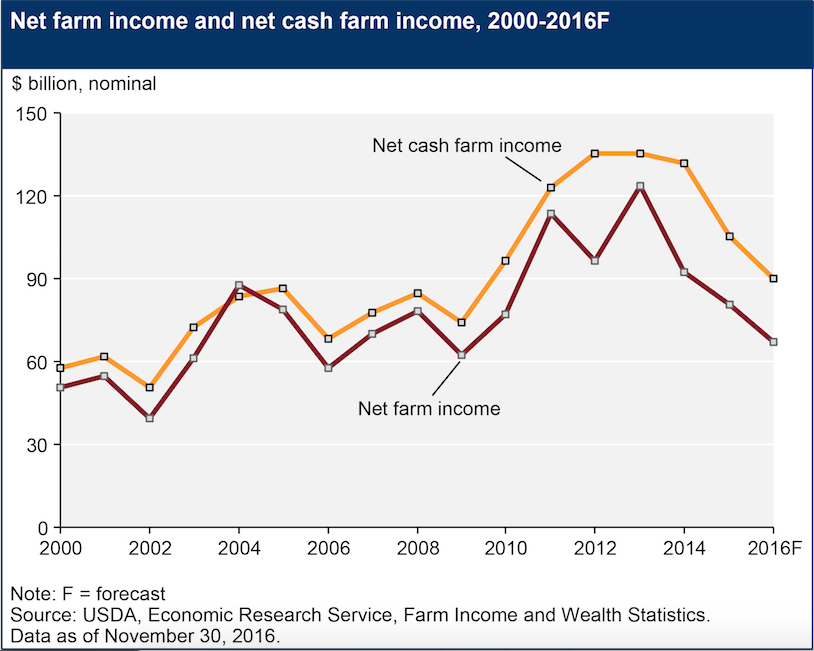

This growing demand for credit aligns with USDA’s Economic Research Service (ERS) findings that show a significant decline in net farm income since 2013. This decline, represented in the chart below, is especially obvious in 2016, in which net farm income dropped by about 11.6 percent and can help explain the growing need for federal loans. Low commodity prices are one explanation for the recent decline in farm income.

Operating Loans – National Snapshot

Overall, FSA direct operating (DO) loans have consistently represented the largest category of loans in terms of the number of loans made – 60 percent of loans in both FY 2015 and 2016. This is likely due to the nature of farming and seasonal cash flow and high demand for annual farm operating costs. However, these loans only represent 22 percent of the total loan funding that FSA gets out the door, with the majority of loan funding going to larger farm real estate loans.

In 2016, farmers utilized FSA guaranteed operating loans (GO) far less frequently, with only 4,982 loans made in FY 2016 compared to the 23,577 DO loans. However, GO loans were on average much larger than direct loans, due in part to the larger maximum loan amount allowed in statute. The average GO loan in 2016 was roughly $300,000 compared to $57,000 for a direct FSA loan.

While on the whole, FSA lending trends in 2016 mirrored previous annual trends closely, last year did see a notable increase in the demand for operating loans in particular. The demand was so high, that it actually surpassed available funding and USDA ran out of funding for operating loans. In June of 2016, NSAC, along with other organizations, pushed for a modest increase in funding for both DO and GO loans upon learning that they would soon run out. As a response to these efforts and the evident demand from new and established farmers across the country, USDA was able to secure additional funding and was able to make up nearly one third of this deficit in September. A funding bill passed in December gave USDA additional flexibility to meet loan demand through April; beyond April, however, current funded levels will not be sufficient to meet demand. Unless Congress provides additional funding in their final Agriculture Appropriations bill for FY 2017, we will see a repeat of last year’s funding crisis, or perhaps an even worse scenario.

Operating Loans – Regional Disparities

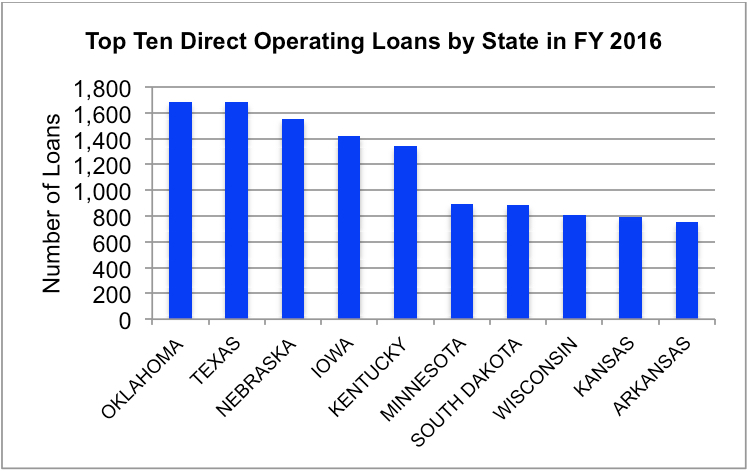

Overall, the regional breakdown of DO loans by state is unsurprising. Most DO loans aligned with the top agricultural states across the Midwest and Great Plains, including Oklahoma, Texas, Nebraska, and Iowa. States with surprisingly low usage include Illinois, Indiana, and Ohio.

Farm Ownership Loans – National Snapshot

In terms of real estate financing, FSA direct farm ownership (DFO) loans made up the second largest segment of FSA loans, with 5,645 loans made in FY 2016. However, since farmland purchase values are generally a larger expense than annual operating costs, DFO and guaranteed farm ownership (GFO) loans are likewise larger on average than operating loans. In fact, GFO loans in FY 2016 comprised the single largest category of loan funding – totaling 38 percent of all FSA loan funding, or $2.4 billion. This marks a significant 21 percent increase over FY 2015 levels, which could in part be the result of increased scrutiny and security required by private lenders who are nervous about low commodity prices and future cash flows required to support a long-term mortgage.

Additionally, despite the shortage in operating loans, there was a surplus of ownership loans in FY 2016, particularly among DFO loans, in which $500 million of appropriated funds went unused. With the growing number of beginning and socially disadvantaged farmers across the country, it is hard to imagine there was no use for these excess funds. Furthermore, when one considers that DFO loans averaged about $180,000 per individual loan, in theory, this would mean roughly 2,500 additional farmers could have been supported through the DFO loan program.

There’s a number of potential factors that may explain this lack of perceived demand, including the low loan cap of $300,000 which has not been adjusted since 2002, whereas real estate land prices have increased 40 percent over the same time period. Additionally, with the downturn in the farm economy and sustained low commodity prices, fewer farmers may be willing to take on additional financial debt.

Farm Ownership Loans – Regional Disparities

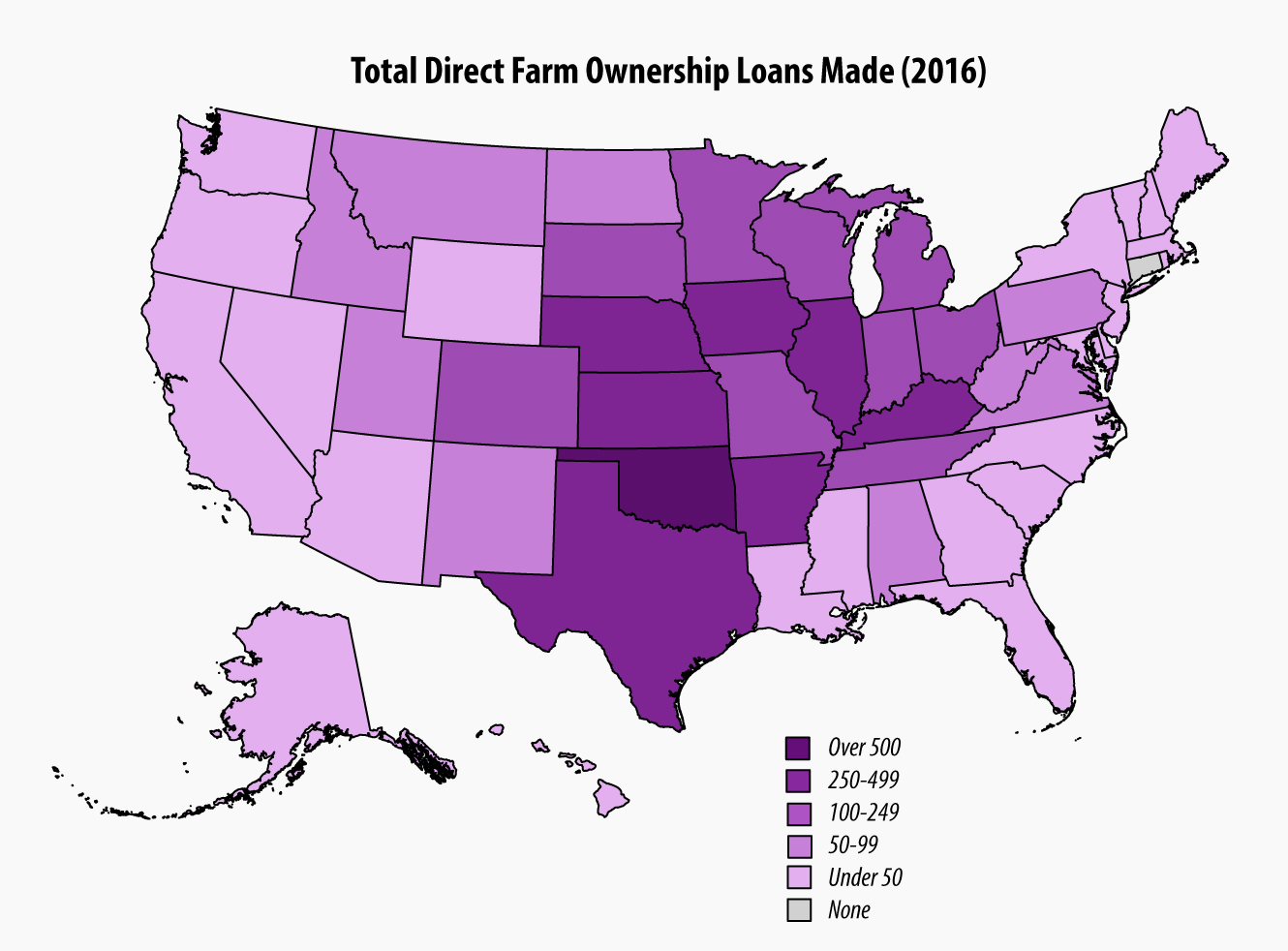

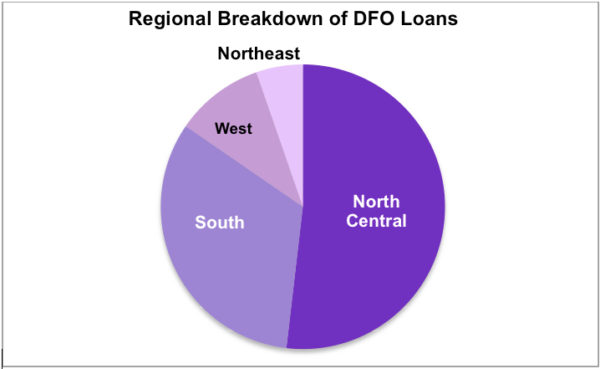

The map above represents the distribution of DFO loans made across the country in 2016. The largest concentration of DFOs correlate to heavily agricultural states in the North Central and Southern regions, and are being used to a lesser extent elsewhere. The under-utilization of loans is especially notable in the West, which includes many important specialty-crop producing states.

For example, California, which leads the country in total agricultural sales, only made 43 direct ownership loans to farmers across the entire state in all of FY 2016, in comparison to the state’s 81,500 farms (as of 2012). There are likely many factors contributing to this trend, most predominantly the $300,000 cap on real estate loans. Farmland in California is valued at roughly $7,900 per acre, one of the highest in the country. This means the average size farm in California comes with a price tag of about $2.9 million, not including any infrastructure on the farm. Clearly, $300,000 doesn’t go a long way for farmers looking to buy land in California, and other states with high real estate values across the country.

Similar trends can be seen across the Pacific Northwest. In 2016, FSA made fewer than 50 ownership loans in both Washington and Oregon. It’s quite likely that DFOs are not successful here due to the production of high value orchards that command a sales price that exceeds the $300,000 maximum DFO loan amount. This leaves beginning farmers with very few options for financing if they are turned down by a private lender.

Finally, the low usage trends in the Northeast, where most states have below 50 DFOs in FY 2016 (such that FSA made zero DFO loans in Connecticut), can largely be explained by land availability. These are smaller states with strong, yet small farming communities. Because of the pressures of development and urban and suburban sprawl, these small-scale and typically diversified farmers (beginning and new) are often unable to afford or access financing to afford agricultural land.

Summary

In summary, while the FSA loan program has become an increasingly important tool for farmers, especially new and socially disadvantaged farmers, the farming community in many parts of the country have yet to tap into this incredibly important financial resource. In our next post, we will expand upon these issues and dive into the ability of these programs to reach beginning and socially disadvantaged farmers.