Editor’s Note: This is the third post of a three-part blog series analyzing the impacts of the Farm Service Agency’s fiscal year (FY) 2016 direct and guaranteed loan programs. This blog will focus on socially disadvantaged farmers and ranchers and the trends in their loan participation across the U.S.

The U.S. Department of Agriculture’s (USDA) Farm Service Agency (FSA) administered over 9,000 operating and ownership loans in fiscal year (FY) 2016 to help socially disadvantaged (SDA) farmers and ranchers – including farmers of color, women, and veteran farmers – defray the cost of real estate purchases and regular operating costs.

In the early 1990s, the National Sustainable Agriculture Coalition (NSAC) led legislative efforts to direct more of USDA’s credit resources towards beginning and SDA farmers and ranchers. Access to USDA loan and credit programs is especially critical for these types of farmers because they have historically experienced more difficulties obtaining financial assistance from the private market. As a result of NSAC’s work, there are now target participation rates within the direct and guaranteed loan programs to increase access to credit for beginning and SDA farmers.

Despite the considerable need for access to loans and credit, NSAC found that the total number of loans to SDA farmers and ranchers decreased by two percent from FY 2015 to FY 2016. However, the overall number of FSA loans actually increased during this same period. In other words, FSA increased the number of loans to established, white, male farmers and decreased the number of loans made to minority and women farmers. Unfortunately, the data does not show the actual demand for FSA loan financing in each of these categories, so it may be that demand by SDA farmers declined. However, the downturn in the overall farm economy in FY 2016 resulted in increased loan demand across all loan programs, and we have no reason to believe that this was any different for SDA farmers and ranchers.

In this post we will attempt to provide a summary analysis of FSA’s loan programs in terms of their performance in supporting SDA farmers and ranchers. We will review these data by geographic region and by loan type, as well as provide thoughts on FSA’s lending outlook going forward.

Lending Trends in FY 2016

FSA offers farmers two types of loans: direct loans, which come out of USDA’s funding pool; and guaranteed loans, which are provided by private agricultural lenders that are backed by USDA in the event that a farmer is unable to repay their loan. To ensure that SDA farmers and ranchers can access these loan programs Congress has set a target participation rate, which is determined on a state-by-state basis and impacted by the overall population demographics. For direct farm ownership (DFO) loans, the target rate is determined by the total percent of SDA persons living in a particular county. For direct operating (DO) loans, the target is determined by the percentage of SDA producers in a state. If there is leftover funding in a state’s SDA pool, that funding can be transferred to a state with higher demand. See our Grassroots Guide for more details on how target participation rates are set by FSA.

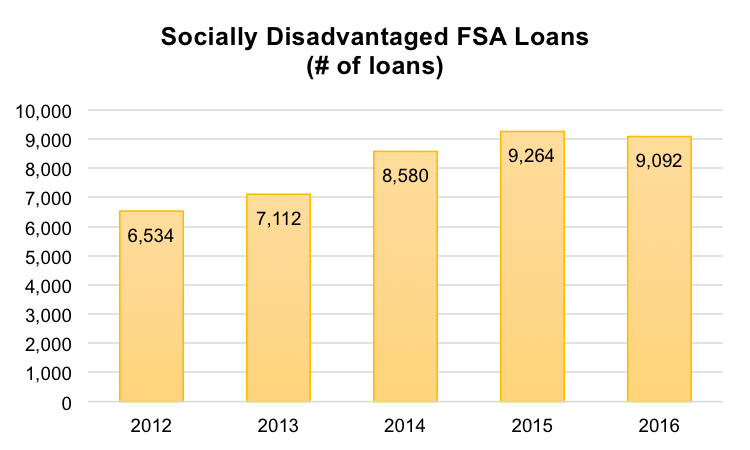

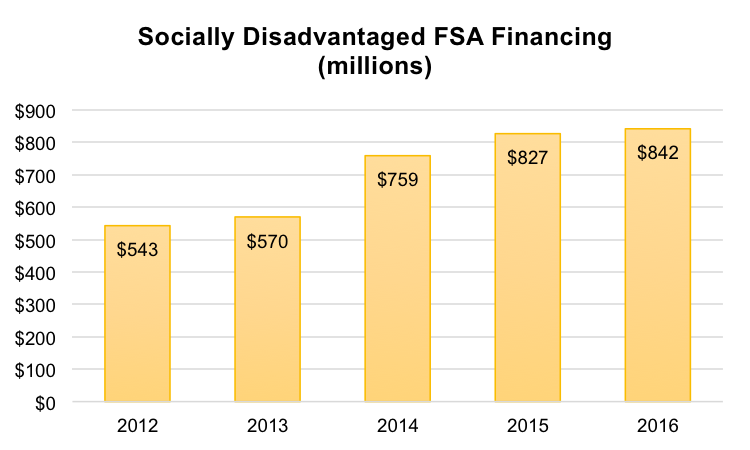

Overall, SDA farmers received 9,092 loans ($842 million) in FY 2016; 172 fewer loans (a decline of two percent) than were made to SDA farmers in 2015. Guaranteed operating loans saw the sharpest decline amongst all loan categories, with 8 percent fewer loans made to SDA farmers in 2016. Direct operating loans, however, saw the largest absolute drop – with 135 fewer loans made in 2016.

Although the total number of SDA farmer loans declined in 2016, the number actually increased substantially over the past five years. Since 2012, FSA has increased the number of loans to SDA farmers by 40 percent and increased total loan financing by 55 percent. It is worth noting that these increases are larger than either the growth in FSA’s beginning farmer loan portfolio (32 percent) or the FSA loan portfolio (24 percent) over the same time period.

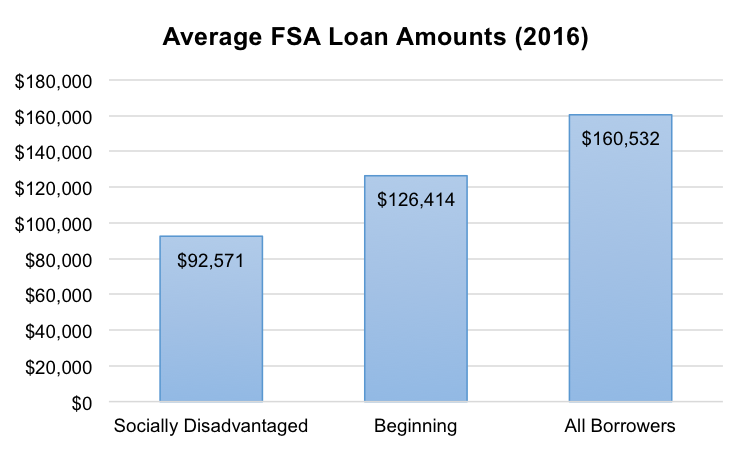

As in prior years, SDA farmers relied most heavily on direct loans; especially direct operating loans, which made up three quarters of all FSA loans to SDA farmers in FY 2016. Guaranteed loans tended to be larger than direct loans, though the average loan amount to SDA farmers was smaller across all loan categories compared to loans made to other demographics. The average SDA farmer loan in FY 2016 was roughly $93,000; the average loan size was $126,000 for beginning farmers and $160,000 for all FSA borrowers. Over the last five years FSA has most increased the size of loans going to established, non-minority farmers.

Because of the historic discrimination and unique challenges that SDA farmers face in securing financing, it is especially troubling that FSA decreased its support to minority and women farmers across nearly every loan program in 2016. Several factors could be contributing to this trend, including increasing demand by and competition from established farmers for loans, and a lack of outreach and information made available to SDA farmers on behalf of FSA. NSAC will continue to monitor FSA loan-making activities over the coming year, and will urge the agency to address these concerning trends.

Regional Analysis

The map below represents the percentage of loans administered to SDA farmers relative to each state’s total number of FSA loans.

Overall, the west coast and the southern region are areas in which FSA seems to have made particular effort and were most successful in serving SDA farmers. Interestingly, the areas with the highest percentage of loans to SDA farmers were also those where FSA loans to beginning farmers were particularly low. This is especially evident in California, which awarded the largest percentage of loans to SDA farmers of any state, yet had the lowest percentage of loans to beginning farmers (for more information on FSA lending to beginning farmers, see our previous blog post).

In the Midwest and Plains regions where beginning farmers received a large portion of loans, only a small percentage (less than 20 percent) of loans went to SDA farmers in FY 2016. This disparity is partially due to differing regional demographics, but also indicates that FSA may need to address its outreach to beginning and SDA farmers on a national level.

Unfortunately, FSA does not yet provide a breakdown of its socially disadvantaged farmer loan data by different demographics (i.e., women, minority, and veteran); this is in part due to the fact that there is overlap between these different demographics. We can gain some insight into lending practices among these particular groups, however, by reviewing lending data from the FSA microloan program (which provides information broken down by specific demographic data).

Microloans

The FSA Microloan program was created in 2013 to meet the credit needs of smaller-scale beginning and SDA farmers – including urban growers, and those serving local and regional markets. FSA’s Microloan program is particularly useful for these farmers because the application process is streamlined to be more efficient and more accessible. Over the past four years, microloans have grown to represent 12.5 percent of FSA’s total direct operating loan portfolio. Microloans have a maximum loan amount of $50,000 and thus are more popular for operation and maintenance purposes than for real estate purchases.

FSA data provides a detailed breakdown of user demographics for operating loans only. In FY 2016, FSA made roughly the same number of microloans as the year prior, with nearly 75 percent of all microloans going to beginning farmers. This is notably higher than the 62 percent of all direct operating loans that go to beginning farmers, which demonstrates that microloans are an especially attractive loan option for this group.

In FY 2016, 34 percent of microloans went to socially disadvantaged farmers; roughly 60 percent of these loans went to women farmers. Since there is some overlap between loans made to minority and to women farmers, it is difficult to assess exactly how many of the 2,250 SDA farmer microloans went to farmers of color. Of the 34 percent of microloans that went to SDA farmers, seven percent of microloans were made to military veterans; over $11 million in loan financing for annual operating expenses.

Additional data is still needed in order for us to better understand how microloans are being targeted toward and how well they are meeting the needs of America’s SDA farmers.

Next Steps: FY 2017 and Beyond

With government funding currently operating on a Continuing Resolution (CR) and the number of farmers in need of FSA loan services continuing to rise, the potential for a FY 2017 farm credit backlog is high (see our previous post on the CR and farm credit funding). Because FSA provides critical support for farmers who wish to purchase farmland, as well as those who require assistance with routine and necessary farm maintenance expenses, the livelihoods of many farmers may ultimately depend on the availability of this funding. Throughout 2016 NSAC fought for additional funds to be allocated to FSA to stave off this credit crisis. Ultimately, we were successful in convincing Congress to allocate an additional $185 million in stopgap funding for direct and guaranteed farm operating loans, and we also secured a rare “anomaly” in the CR, which will allow USDA to make loans to farmers and ranchers in proportion to demand. This anomaly provision will make it possible for USDA to offer credit to beginning, SDA, and other family farmers during the winter and spring months (when demand peaks) without running out of loan funds.

NSAC will continue to fight for adequate funding to FSA loan programs in the FY 2017 budget, particularly for funds that provide critical support to beginning and SDA farmers and ranchers. Stay tuned to our blog for more updates on FSA, and on the FY 2017 budget, as developments occur.

Interesting story about Disadvantaged Farmers of US it helps other to learn many thing thanks for showing the chart also

Well said, Good info. There is no doubt that for a new business setup, most of the people take business loan but some people’s loan application is rejected by the banks and lots of people don’t know what the reasons behind are. But thanks for the post, it’s really informative for those people which are need business loan.