Organic producers, according to the U.S. Department of Agriculture’s (USDA) National Organic Program (NOP), are limited to farming according to a set of practices and standards that must demonstrate a commitment to protecting natural resources and conserving biodiversity. They also may only use NOP-approved substances (e.g., herbicides, fertilizers, etc.). Given organic agriculture’s adherence to a more strictly defined set of standards and practices, and more limited crop protection inputs, it would be easy to assume that organic farmers would see more losses in crops than their conventional farming peers. However, from the available evidence to date for crop  insurance loss rates, we have found the results to be mixed.

insurance loss rates, we have found the results to be mixed.

A lack of a clear “winner” when comparing crop insurance losses was the key takeaway of the 2015 Summary of Business for Organic Production report from the USDA’s Risk Management Agency (RMA).

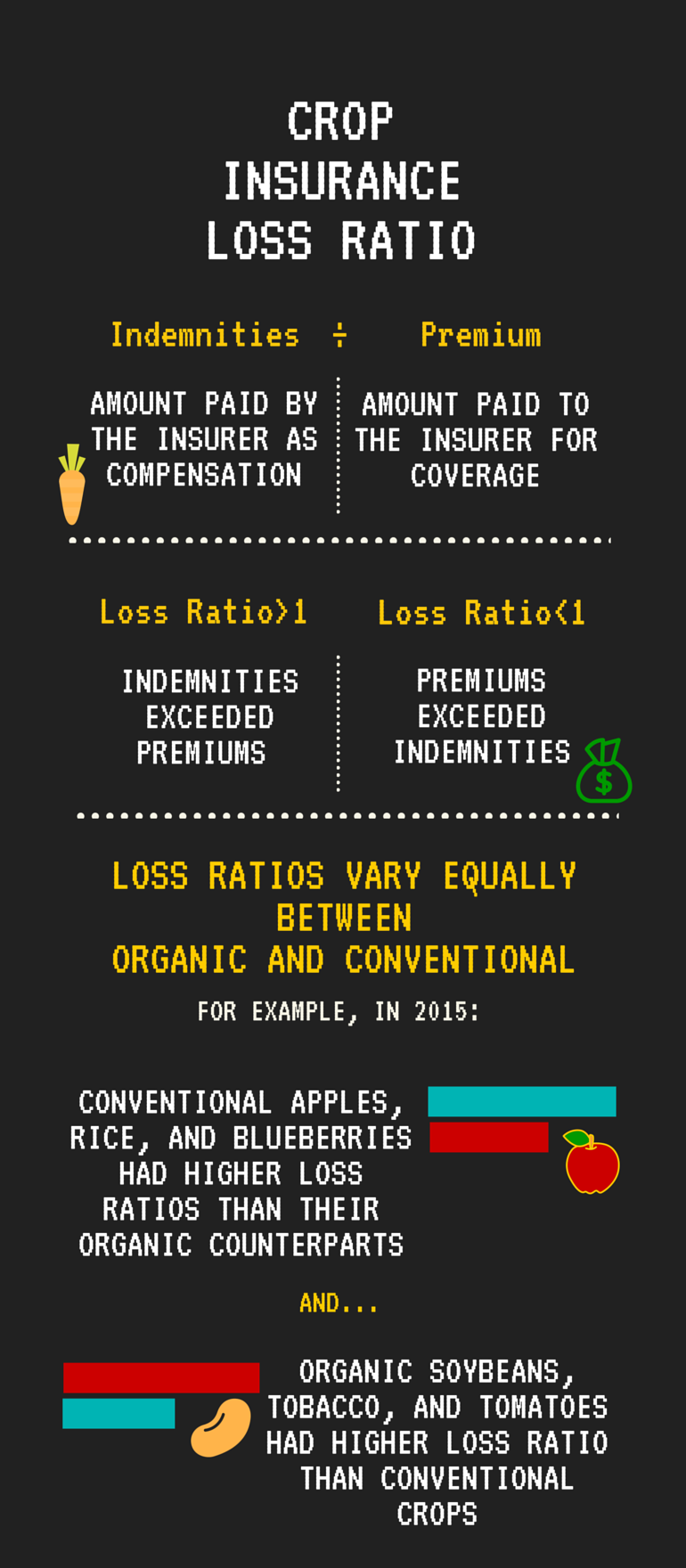

Each year, RMA compiles reports (“Summary of Business” reports) on crop insurance program usage, including organic crop insurance. The organic report breaks down, by state and crop, the “experience” of crop insurance on organic land. “Experience” refers to the loss rate for each crop in a single state, and for the same crops across different states. The loss ratio[i] is found by dividing indemnities by premiums. A loss ratio of more than 1 means that indemnities exceeded premiums, likewise a loss ratio of less than 1 means premiums exceeded indemnities.

The Overall Organic Experience

RMA’s Summary of Business for Organic Production report compares the experience for organic crops with that of conventional crops. To control for the fact conventional crops are much more widely grown, the report only compares the conventional experience with the organic experience in areas where both are grown.

The loss ratio for all insured organic crops (organic and transitioning) was found to be 1.16, compared to .49 for conventionally grown crops. However, it is interesting to note that 35 of the 67 organic crops surveyed in the report had similar or lower loss ratios[ii] than their conventional counterparts over the same time period (2006-2015).

A Deeper Look at the Numbers by Crop

The loss ratios for organic crops vary as widely as those for conventionally grown crops. For example, the report shows that conventional tropical fruits had a loss ratio of the 4.13 over the 2006-2015 period, while the organic experience was 1.36 over the same period. Differences in acreage between the conventional and organic produce, however, makes a balanced comparison problematic – 20,591 organic acres were included in the report versus 718,925 conventional acres.

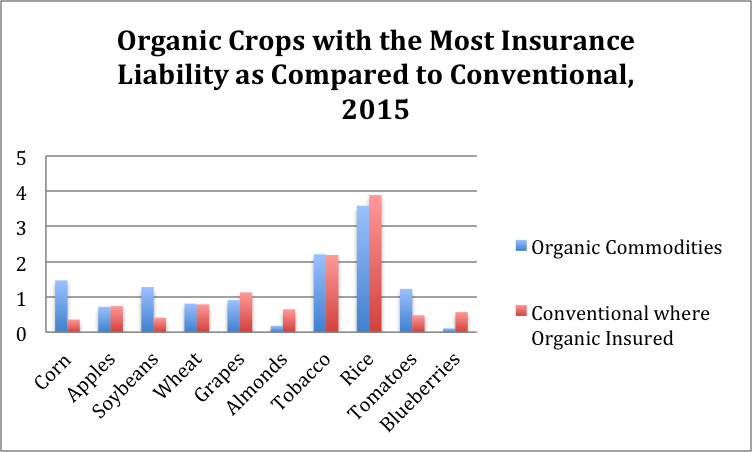

Perhaps the best comparison between the organic crop experience and conventional can be made by looking at the top 10 crops based on organic liability; these crops are grown on larger acreages, more in line with that of their conventional counterparts. The following chart shows the loss ratios for the top 10 organic crops with the most insurance liability during 2015, as compared to loss ratios for conventional crops grown in the same areas.

As we can see from the chart, there was no clear difference in loss ratios for almost all of the compared crops in 2015 (with the exception of corn and soybeans, the only two crops with GMO traits, and the only two which are produced in large quantities not intended for human consumption). Conventional apples, grapes, almonds, rice and blueberries had higher loss ratios in 2015 than their organic counterparts, while organic corn, soy, wheat, tobacco, and tomatoes had higher loss rates than conventional.

Conclusions

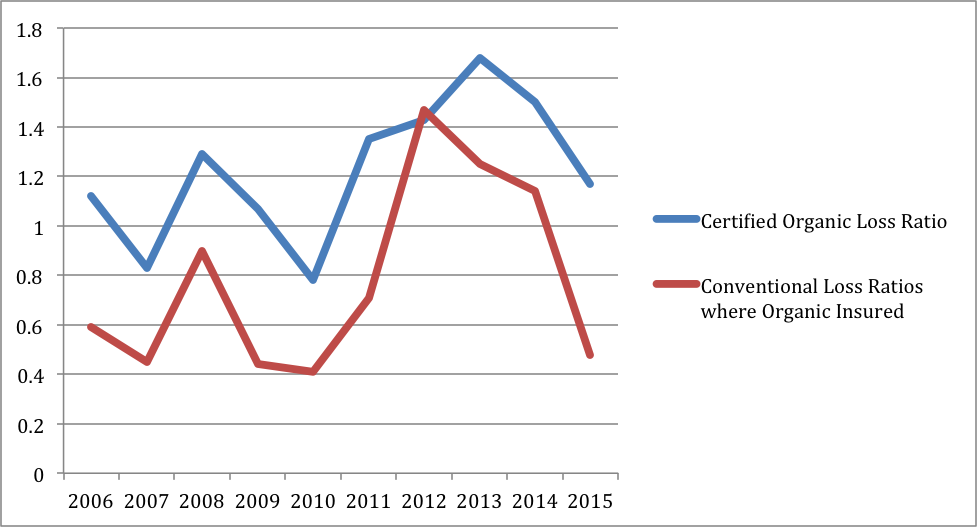

It is clear from the Summary of Business for Organic Production report that both conventional and organic experience (when compared in areas where both are insured) are both widely variable. As the chart below indicates, losses to both conventional and organic crops track each other closely. The main causes of loss for both, weather and other commonly insurable events, are beyond the ability of either organic or conventional producers to control, and remain among the biggest driver of losses.

The fact that the top 10 organic crops by insurance liability have loss ratios closely in line with conventional crops indicates that as a crop’s organic acreage increases (and likely also the grower’s experience level), the difference in loss ratios decreases.

The connection between ability to scale and experience levels is one of many reasons we need more support for more organic agricultural research, which can help to close the knowledge and cultivar gap between organic and conventional production. The limited availability of cultivars adapted to organic systems and the disparity in research funding for organic production methods puts organic producers at an serious disadvantage.

As more organic and diversified producers are able to access federal crop insurance programs and more robust data becomes available, the loss ratios between conventional and organic production are likely to change significantly. As of 2015, only ~1 million acres of organic production were insured, compared to ~295 million conventional production acres.

More Access and Research for Organics Needed

The inherent challenges in comparing the experience of organic to conventional crops suggests that RMA, and the crop insurance industry as a whole, need to do more to bring organic and diversified growers into the crop insurance program and study their usage. One promising way this can be done is through the promotion of policies like Whole Farm Revenue Protection (WFRP). WFRP insures all the crops and animals on a farm under one revenue policy, instead of on a crop-by-crop basis.

The policy is growing in popularity among farmers, but many agents fail to recommend it to their agricultural clients because they don’t fully understand how the policy works or how to write one. WFRP policies can take longer to write than crop insurance policies because the agent needs to construct a revenue history for the farmer and enumerate each crop grown. Because agents are paid no more for selling and writing up WFRP policies than for simpler, single crop insurance policies, this reduces the incentive for agents to promote WFRP. Changing the existing reimbursement policy will be important for advancing WFRP.

Federal Crop Insurance Program Background [iii]

In 1938, Congress established the federal crop insurance program following several unsuccessful attempts by the private sector to sell multiple-peril policies (which began in the late 1800s). Since then, private crop insurance has focused on single peril insurance for causes of loss not correlated across wide areas, such as hail or fire.

The current program, which is administered by the U.S. Department of Agriculture’s Risk Management Agency (RMA), provides producers with risk management tools to address crop yield and/or revenue losses for about 130 crops, although most of those policies are only available in a few states and counties.

In purchasing a crop insurance policy, a producer growing an insurable crop selects a level of coverage and pays a portion of the premium, which increases as the level of coverage rises. The federal government pays the rest of the premium (62 percent, on average, in 2014). Insurance policies are sold and serviced through 18 approved private insurance companies. As spelled out in a Standard Reinsurance Agreement (SRA), the insurance companies’ losses are reinsured by USDA, and their administrative and operating costs are reimbursed by the federal government.

In 2014, federal crop insurance policies covered 294 million acres. Major crops are covered in most counties where they are grown. Four crops – corn, cotton, soybeans, and wheat – typically account for more than 70 percent of total acres enrolled in crop insurance.

Most crop insurance policies are either yield-based or revenue-based. For yield-based policies, a producer can receive an indemnity if there is a yield (production) loss relative to the farmer’s “normal” (historical) yield. Revenue-based policies protect against crop revenue loss resulting from declines in yield, price, or both. Other insurance products protect against losses in whole farm revenue (rather than just for an individual crop) or gross margins for livestock enterprises.

Government costs for crop insurance have increased substantially during the last decade. Ranging between $2.1 billion and $3.9 billion from fiscal year (FY) 2000 to FY 2007, crop insurance costs rose to $7 billion in FY 2009 as higher policy premiums from rising crop prices drove up premium subsidies to farmers and expense reimbursements (which are based on total premiums) to private insurance companies. Costs peaked at $14.1 billion in FY 2012 when crop prices surged again and poor weather resulted in program losses. With a return to more favorable weather and smaller crop losses, total program costs declined $8.7 billion in FY 2014 and are expected to be $8 billion for FY 2016

[i] These crops had either lower loss ratios than their conventional counterpart, or were within .20 of the conventional loss ratio.

[ii] The ratio of the claims paid by an insurer to the premiums earned, usually for a one-year period.

[iii] Based on the Congressional Research Service Report R43494

Greetings from Florida! I’m bored at work so I decided to browse your site on my iphone during lunch break.

I really like the knowledge you provide here and can’t wait to take a look when I get home.

I’m surprised at how fast your blog loaded on my mobile ..

I’m not even using WIFI, just 3G .. Anyways, superb site!

There’s certainly a lot to learn about this issue.

I like all the points you made.