This is the first of several blogs which will explore the impacts of consolidation and concentration in the agriculture industry on farmers and the broader food system, as well as a path forward. The blog series is authored by NSAC Policy Associate Billy Hackett with meaningful contributions by farmers and experts. Read the second entry here: Farmers Trapped in Unsustainable Cycle by Biotechnology, Seed Consolidation.

While the first days of a new presidential administration, the second impeachment of a former President, and the rollout of COVID-19 vaccinations have dominated the initial news cycle of 2021, another groundbreaking story has garnered only modest attention in recent months: antitrust proceedings have launched against tech giants, including Facebook and Google. The practice of limiting the size and market share of massive corporations for the preservation of competition, once a core tenant of American free market economic policy, has faded to relative obscurity through a combination of lax regulatory enforcement and a proliferation of consumer facing brands that obscure the degree to which many market categories lack real choice. Now, public concern is rising once again – and antitrust enforcement is at a crossroads.

Definitions

Before we dive into what, exactly, this means for agriculture, let’s establish some definitions and real-life examples to ground us in the basic economic principles that drive this series.

Antitrust: Laws and regulations that encourage competition by limiting the market power, or the ability to influence the price of an item in the marketplace by manipulating supply or demand, of any one firm.

Consolidation: The combination of several business units or different companies into a single, larger organization; e.g. when a single company owns the cattle, the stockyards, the trucking company, the processing plant, and the distribution through retail.

Concentration: The extent to which market shares are concentrated between a small number of firms; e.g. when only a few companies control all of beef processing.

Monopoly: An individual, company, or group that becomes large enough to own all or nearly all of the supply of goods, commodities, facilities, amenities, or support systems and can define an entire market segment and exclude other market entrants; e.g. a company that contracts farmers to raise chickens and owns the breeding company, the hatcheries, the feed mills, the slaughterhouses, and the trucking lines.

Monopsony: An individual, company, or group that positions itself as the sole purchaser for a particular good or service; e.g. a food processor that a farmer must sell to in order to reach consumers at market.

The facts

So, what do these antitrust proceedings against Facebook, Google, and Amazon have to do with agriculture? Everything. While the tech, pharmaceutical, finance, and oil industries grab most of the headlines, the food and agriculture industry has become highly (and increasingly) concentrated over the past 50 years.

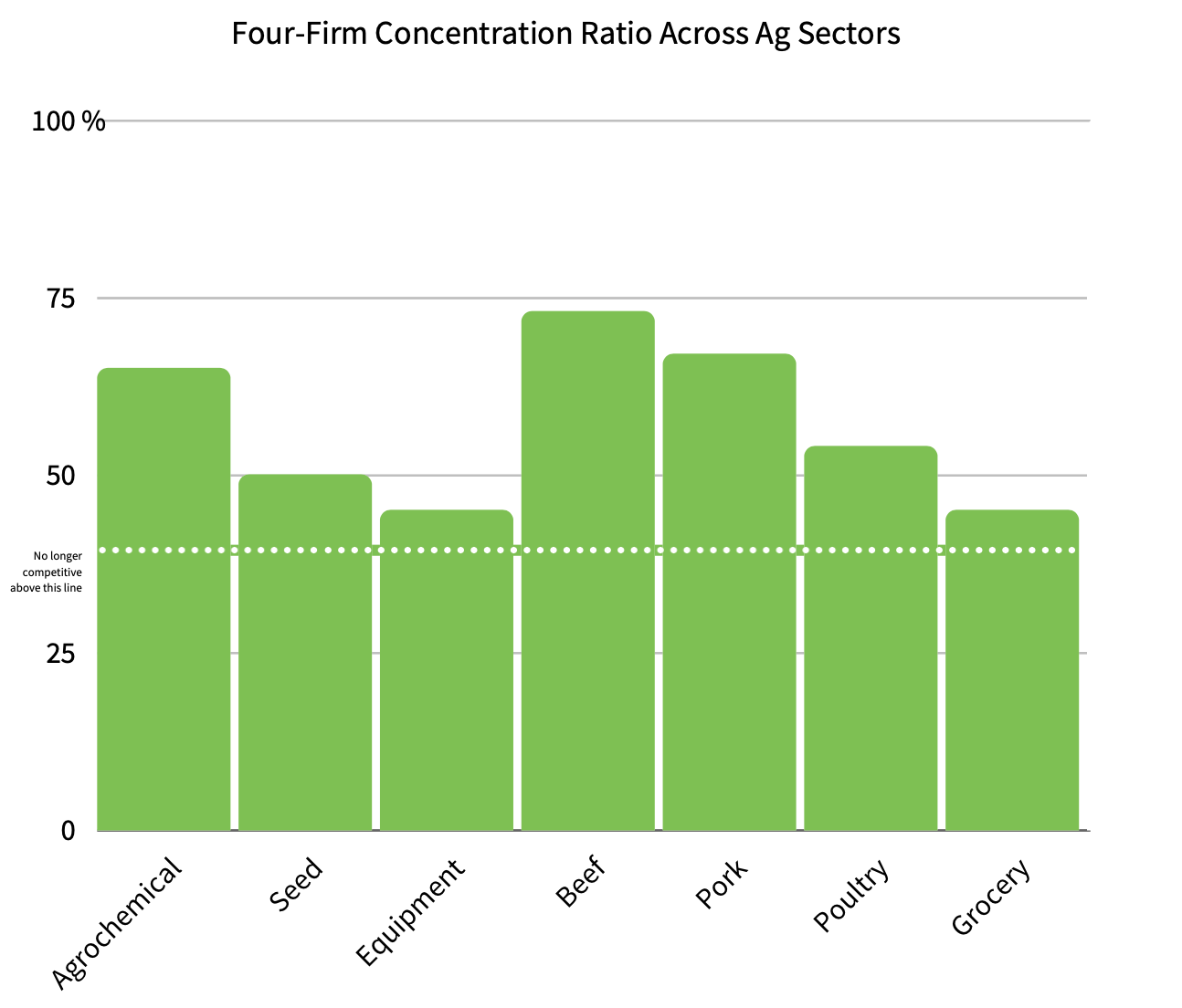

To illustrate, updated estimates of the four-firm concentration ratio (CR4) across each sector of the food and agriculture industry were published in a recent special report to the Family Farm Action Alliance (FFAA). Just four corporations are responsible for 65 percent of sales in the global agrochemicals market, 50 percent of the seed market, and 45 percent of farm equipment sales. In the United States, just four companies represent 73 percent of beef processing, 67 percent of pork processing, 54 percent of chicken processing, and 45 percent of the retail grocery market.

This concentration – which does not even account for rising consolidation, or vertical integration – has profound implications for everyone connected to the food system, from farmer to consumer. Economists agree that an industry is no longer competitive when the market share of the top four companies is 40 percent or higher, and that ceiling has been clearly exceeded across the agriculture industry. This level of concentration in any industry may lead to an exclusion of competitors, reduced wages for workers, a price increase for consumers, a decline in product quality, and depressed innovation and research.

In this blog series, we will explore how a handful of actors wield their extraordinary power to manipulate their respective markets, set the terms of debate, and, most importantly, what this all means for farmers, ranchers, and rural communities. This series is not a groundbreaking body of original research, nor is it necessarily exhaustive, but it is an introduction to the hidden, interconnected dynamics that drive the modern U.S. food and agriculture industry. At the heart of this series is the question, ‘Is the status quo worth defending?’

How did we get here?

To move forward, we must understand from whence we have come. The modern incarnation of the U.S. agriculture system has its roots in the era of the New Deal, when the federal government acted to reverse a 75 percent fall in commodity prices that began as European food production was restored, supplanting the demand for U.S. food exports that had served as foreign aid since the end of World War I. This temporary boom had been fueled by domestic overproduction as well as tax policies to protect U.S. producers from imported grains.

In its bust cycle, millions of farms foreclosed. Where 41 percent of the U.S. workforce was employed in agriculture in 1900, that number halved to 21.5 percent by 1930. President Franklin D. Roosevelt signed the first Farm Bill, the Agricultural Adjustment Act of 1933, to address the crisis. It featured measures intended to reduce market oversaturation and establish parity to keep farm income in-line with the costs of farming, including grain reserves where the government held purchased surpluses of commodities to avoid food shortages and price spikes, a price floor below which market prices were not permitted to fall, and a reduction in the number of acres farmers were allowed to plant (e.g. acreage allotment).

Parity: The ratio of the prices farmers receive for the products they sell to the prices they pay for goods and services.

The impact of these supply chain management policies continue to be debated. In the short-term, they helped restore farm incomes even as U.S. farmers again achieved temporary prosperity as World War II and the postwar reconstruction increased the demand for U.S. food exports. During this same period, however, farm employment continued to shrink until just 16 percent of the U.S. workforce was still employed in agriculture by 1945. Black farmers were notably excluded from numerous New Deal programs altogether, which played a damning role in the 98 percent fall in the number of Black-operated farms from 1920 to 1997.

Food processing, grain, and meatpacking industry owners and shareholders opposed New Deal farm policies. They had long benefited from cheap commodity prices during periods of overproduction, and in the late nineteenth century had used their profits to consolidate and form large corporate bodies, or trusts, to concentrate ever greater market share and fix prices in their favor. At that point, just five meatpacking companies controlled 60 percent of that market. Popular movements against these anticompetitive practices prompted antitrust and fair competition legislation to end the Gilded Age in 1890 (the Sherman Antitrust Act), 1914 (the Clayton Antitrust Act), and 1921 (the Packers and Stockyards Act). These measures were used and amended to curb unfair industry practices and restore competition in the marketplace through the 1970s.

Powerful industry, banking, and business leaders quietly organized a retaliatory campaign to combat the growing power of farmers and workers. They formed groups like the Committee for Economic Development (CED), which leveraged a revolving door to the public sector and close ties to academia to make their laissez-faire economic philosophy mainstream. They exploited what became clear in the 1950s – that the largest, mechanized farms had emerged as the chief beneficiaries of price support policies – to divide farmers and advance an alternate vision for the U.S. agriculture system best articulated in a 1962 CED report (their fourth on the subject): “An Adaptive Approach to Agriculture.” The report’s influential contributors, which included faculty from the Chicago school of economics, advisors to U.S. presidents, and executives of national banks and food processing companies, charged that the “farm problem” was too many farmers using too many resources while producing too little return on investment. Perpetuated by government programs, they argued, this inhibited maximum economic efficiency. The solution? Fewer, larger farms.

When these coalitions spoke, the framers of agriculture policy listened. Ezra Benson, President Eisenhower’s agriculture secretary, embraced the free-market approach to mitigate the farm problem. Through the 1950s and 1960s, the adoption of new farm technology was promoted to elevate productivity and, coupled with reduced price supports for commodities and a lowered price floor, falling commodity prices from overproduction forced more and more small farmers to find stability from off-farm income. The industrialization of farming and vertical integration of profitable food processors that followed prompted a former assistant secretary of agriculture to coin the term “agribusiness,” which he lauded as the best alternative to government programs. These policies contributed to a 56 percent decline in the farm population between 1950 and 1970.

This trend accelerated with Secretary of Agriculture Earl Butz from 1971 to 1976, who told farmers to “get big or get out” and professed that “agriculture is big business.” Butz, who served on the boards of several agribusiness firms, removed 25 million additional acres from the acreage allotment program to boost grain production and created a new program that required U.S. taxpayers to make up the difference when commodity prices fell below a target price set by USDA – not food processing or grain companies, who in effect had their input purchases subsidized. He continued to reduce domestic price support to incentivize exports, foreseeing the United States as the world’s breadbasket in a strategy that, if balanced, should mitigate falling prices, and a grain contract with the Soviet Union (USSR) indeed sent wheat and corn prices soaring.

The ensuing surge in public and private sector loans to farmers to expand their operations, modernize their equipment, and keep up with the pace of production was heralded by agribusiness interests but ultimately proved unsustainable. Farmers could not make payments on loans after interest rate hikes were imposed to mitigate the inflation of land prices. Then, an export embargo placed on the USSR after the country invaded Afghanistan cut farmers off from the market upon which they had become dependent. Prices for the grain commodities that farmers planted – from “fencerow to fencerow,” as Butz had urged – crashed and, compounded by the oil embargo that led to heightened costs for farm equipment and fuel in the 1970s, farm debt ballooned by 400 percent between 1960 and 1977. An unprecedented number of farming families were forced to default on their debts and flee the countryside to seek employment in cities, further depopulating rural communities. By 1978, just 19 percent of farms produced 78 percent of crops in the United States – and the worst farm crisis since the 1930s had begun.

Ronald Reagan was elected to the presidency on a deregulatory, free-market platform in 1980. His administration did not act to mitigate the farm crisis in its pivotal first years. Instead, the Federal Trade Commission and Department of Justice under Reagan eviscerated the antitrust policies built over 60 years. Influenced heavily by Robert Bork, the intent of Congress was reimagined and merger guidelines were narrowly re-written such that only consumers may be considered victims of monopoly, establishing that mergers may only be harmful and thus warrant antitrust enforcement if they led to a rise in retail cost to the consumer. The new guidelines prompted an unparalleled number of food mergers and acquisitions that continues today, giving consolidated agribusiness corporations the ability to buy-out potential competitors or otherwise expand their services and markets unchallenged.

Multinational agribusiness companies, experiencing unprecedented growth, successfully lobbied the Clinton Administration to enter the World Trade Organization (WTO) and sign the North American Free Trade Agreement (NAFTA) in the 1990s. They were now free to produce and process food where labor was cheapest and environmental regulations were weakest (which has at times bred scandal for food retail brands). The projected boom in agricultural exports did not materialize to the extent needed to keep up with increased production, however, and in conjunction with the Freedom to Farm Act of 1996 – designed to phase out New Deal price support mechanisms once-and-for-all over several years – excess surplus led to another crash in commodity prices.

The biggest winners from this windfall were the industrialized meat industry and food processors, who used the excess profit to consolidate further and concentrate ever greater market share. Farmers, on the other hand, were losing money. Congress passed emergency relief payments to assist farmers in 1999, nullifying the intent of the 1996 Farm Bill to eliminate government support. These direct subsidies were then codified in the 2002 Farm Bill to avoid further political fallout – becoming the taxpayer-funded commodity crop programs, or farm subsidies, that we know today.

For more on this history, read Foodopoly by Wenonah Hauter.

Grounding in the present

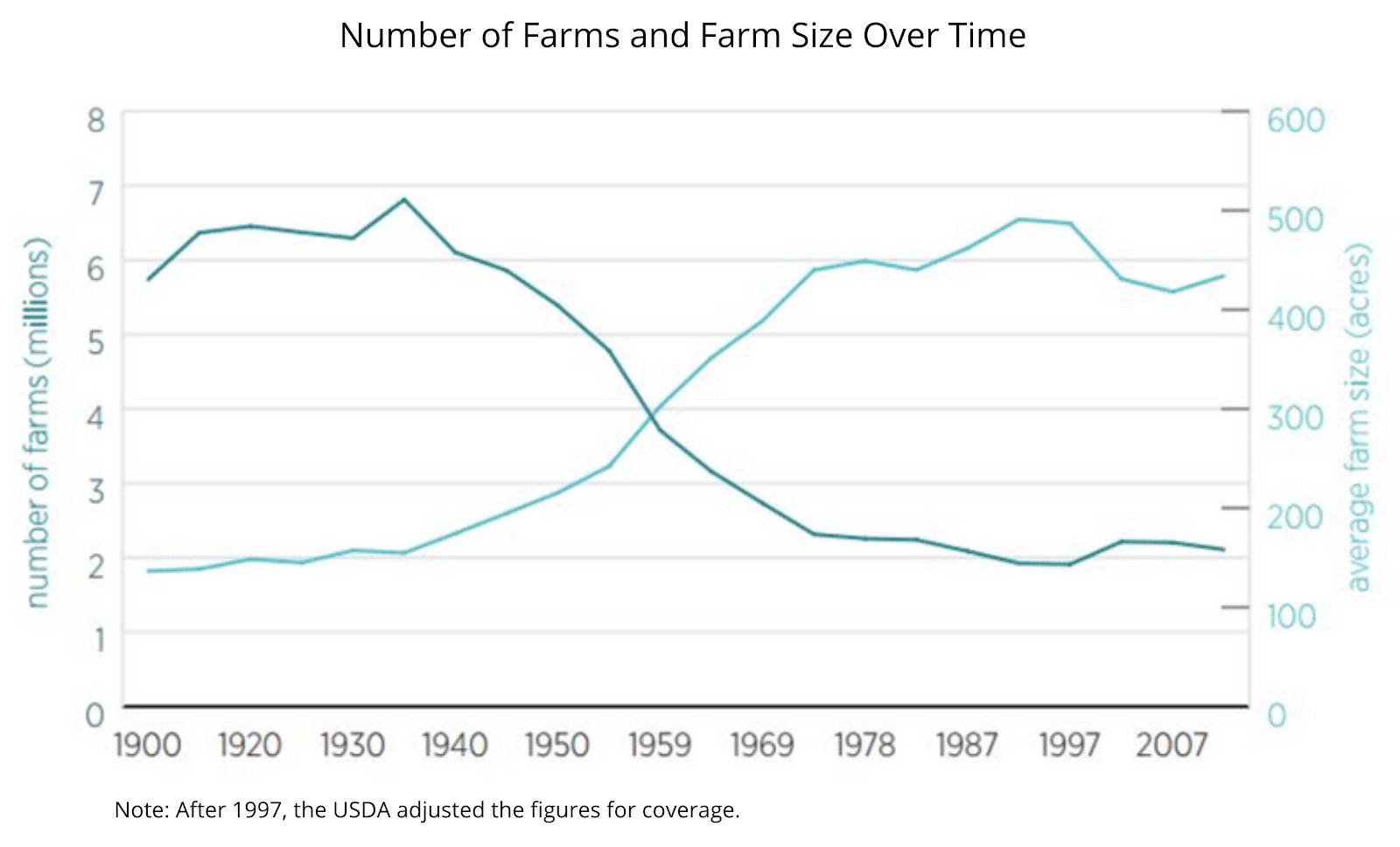

Farmers whose primary occupation is farming represented 1.3 percent of the U.S. workforce in 2019 – down from 41 percent in 1900. Though there are fewer farms, production nearly tripled between 1948 and 2017. The 2017 Census of Agriculture revealed that, of the 2.04 million remaining farms and ranches, just five percent represented a staggering 75 percent of this production. In addition, while the 3.7 percent of farms that make above $1 million represent over ⅔ of the $389 billion value of production, the 76 percent of farms that make below $50,000 represent under three percent of production.

These numbers reflect the evolution of farming from a diversified, localized industry where small, midsized, and large producers competed in the marketplace, to a system where many small farms directly serve local markets and far fewer very large farms serve national markets through a complex web of distribution and manufacture. In today’s farm landscape you are either big or small, and the hollowing of the farm spectrum has created a bifurcated food system that is neither sustainable nor resilient, as the COVID-19 pandemic revealed last year.

The actions necessary to stem the pandemic – closing schools, institutions, and halting public gatherings – were precisely what robbed smaller, direct marketing farmers of their markets. Farmers who served local markets could not easily sell the goods they grew and produced into the national distribution network meant for large farms, as they lacked relationships with buyers and frequently the certifications necessary to sell to them. The small farmers that did manage to access those commodity oriented markets were frequently offered prices well below their cost of production. Many small farmers with ripening produce and no outlet watched their crops literally rot on the vine.

On the other end of the spectrum, the pandemic impacted the largest producers in different ways. As millions of people stopped going to work, school, or restaurants and began eating more meals at home, the food manufacturing industry found that it could not easily pivot from supplying institutional customers to the consumer at home. This was most evident in the meat supply chain, where early outbreaks of COVID-19 at several of the country’s major processing plants – where laborers were compelled to work despite unsafe conditions – severely diminished the ability of farmers to get their animals processed. Small meat processors faced a sudden surge in demand, but did not have the resources necessary to rapidly expand their operations. This all meant that some farmers were forced to euthanize their livestock while less beef and chicken were available in markets, and that at a heightened price for consumers.

While food was being destroyed, tens of millions of Americans struggled to feed their families. They still are. This stunning juxtaposition led many consumers to realize that our food system rests on a few disconnected, parallel systems that risk collapse when faced with any disruption. It failed farmers and consumers at this critical moment, despite being hailed by apologists as “too big to fail.” That said, the modern, consolidated food system was not designed to primarily serve these groups; food insecurity, malnutrition, and diet-related health issues already affected millions of Americans pre-pandemic, and today’s farmers receive less than 15 cents per dollar that consumers spend on food. Rather, it was designed to maximize the efficiency and profits of multinational food corporations. These agribusiness “middlemen” (e.g. corporate processors, retailers, etc.) accrue more than 80 cents of every food dollar spent and are emerging insulated – even profitable – amidst the economic devastation wrought against small, independent restaurants and food businesses during the pandemic.

To be clear, critiques of the contemporary agriculture system are not to be conflated with critiques against large family farmers who may have had no choice but to expand their operations to participate in the system – lest they be swallowed, too. It was the largest business, banking, and industry leaders who coordinated with policymakers to write the rules of this zero-sum game that created modern agribusiness.

Resistance to change

A nationwide poll this year revealed that a striking 81 percent of rural voters would support a candidate who said, “A handful of corporate monopolies now run our entire food system. We need a moratorium on factory farms and corporate monopolies in food and agriculture.” Just ¼ of these self-proclaimed rural voters identify as “liberal” or “progresssive,” suggesting that the issue transcends the bitter partisanship which defines our age. Despite the salience of this issue in rural communities, neither the Republican nor Democratic party have formally claimed its mantle.

Isolated attempts have been made by policymakers on both sides of the aisle to address anticompetitive practices, but no meaningful reforms have passed through Congress. The Farm Bill does not acknowledge the corporate capture of the food system, instead perpetuating the bifurcation of the food system with the consolidation of financial resources and land in the hands of its largest actors. If a popular consensus exists to democratize the food system, why do these attempts consistently fail?

Part of this is the commanding voice of agribusiness interests in Washington. Nine political action committees (PACs) representing large pork, dairy, corn, soybeans, wheat, beef, cotton, and chicken producer groups donated $3.2 million in campaign contributions to farm-state lawmakers through October of the 2020 election cycle. These lobbying groups donated most heavily to Republican campaign committees, though outgoing House Agriculture Chair Collin Peterson (D-MN-7) earned the most contributions of any individual. Without campaign finance reform, the ability of these corporations to influence legislation to maintain the status quo, or at most allow modest reforms within acceptable guardrails, will continue unabated.

In addition, agribusiness corporations with concentrated market share possess leverage to deter small producers from exposing anti-competitive practices in the industry. Those that do call attention to anti-competitive behavior face retaliation in an industry that has no whistleblower protections. While a bipartisan piece of legislation was passed in December to address this gap, its impacts on industry practice once enacted remain to be seen. Just speaking out against malpractice would hold little weight, however, if existing laws meant to preserve competition are not enforced to their fullest extent. Litigation is not a realistic avenue to compel such action; even if it were reasonable for a small farmer to take a multinational corporation to court, mandatory private arbitration – a method of dispute settlement behind closed doors, free from a neutral third party and independent of court precedent – has become the corporate-friendly status quo consistently upheld by the Supreme Court since the 1980s.

“These corporations are very, very good at messing with your head,” said Dave Bishop, 70, a small farmer in rural Illinois. Today, the popular narrative in agriculture is that the rapid concentration of the industry is a natural consequence of advancing technology, not the result of conscious decisions made by agribusiness and government leaders. The food system is hailed as better for consumers, demonstrated by a lower cost for food, while ignoring the rising health issues, environmental degradation, and rural depopulation that it creates. These hidden costs challenge the mainstream rhetoric about the food system’s superior efficiency. “This is a design issue. This is a choice,” Bishop explained.

So, is the status quo worth defending? It is for the multinational food corporations who amass power from excessive, subsidized commodity production, are free to consolidate operations and concentrate market share, and bear no responsibility for hidden costs. It is not for the farmer who sells their product into a marketplace with fewer buyers for a lower price, the consumer with heart disease or diabetes forced to pay untold sums for treatment, or even the policymaker sworn to represent these people.

Opportunity for change

The Biden-Harris Administration inherits this consolidated agriculture system supported by every occupant of the White House for decades. President Biden pledged the following in his rural plan to Build Back Better:

Strengthen antitrust enforcement. From the inputs they depend on – such as seeds – to the markets where they sell their products, American farmers and ranchers are being hurt by increasing market concentration. Biden will make sure farmers and producers have access to fair markets where they can compete and get fair prices for their products – and require large corporations to play by the rules instead of writing them – by strengthening enforcement of the Sherman and Clayton Antitrust Acts and the Packers and Stockyards Act.

We at the National Sustainable Agriculture Coalition (NSAC) urge President Biden to fulfill his commitment, championing statutory change where necessary and strengthening administrative and regulatory antitrust action where possible. Our recommendations for the Biden-Harris Administration to address concentration in the livestock industry concentration are included in NSAC’s 2020 Transition Briefing Papers, and additional policy recommendations will be featured in this blog series.

NSAC is committed to leveling the playing field for sustainable and organic farmers by bringing grassroots perspectives to the table normally dominated by big business. The time is ripe for a serious conversation about common-sense competition and antitrust reform in agriculture as a structural root of many economic, environmental, and personal challenges that farmers, ranchers, and their rural neighbors face. This series will continue to explore how the central role of agribusiness in the food system is not the pinnacle of fair competition but its antithesis, and expose how the dominant actors in each agriculture sector inflate the prices that farmers must pay for inputs, drive down commodity prices, and restrict the ability of farmers to compete in the marketplace.

The next (second) entry in this blog series will explore the consolidation and concentration of the inputs foundational for any farm – including land, farm equipment, and seeds. You can the second entry here.

It is hard to make it out here on the farm with input prices ever increasing.

Lack of competition in our inputs and in our sales are a huge problem.

Hey thanks!

This article gives new meaning to the phrase “You Can’t Beat City Hall” specifically as it relates to the rural farmers of the past and present. Our government has gotten way too big, like a slow growing cancer they have infiltrated all industry on local, state and federal levels—farming being only one —-but the point is well made and the article well written.

However, Biden’s words are just those—words—at least for today anyway, time will tell.

What do you think of the Food and Ag Merger Moratorium Act?

With time limited do we work to support state or National Ag Policy and Bills?