Over Memorial Day weekend, President Joe Biden and House Speaker Kevin McCarthy (R-CA-20) struck a “tentative” deal intended to avoid a catastrophic default on the United States’ debt. In the days since the initial announcement, more details about the deal – now known as the Fiscal Responsibility Act of 2023, H.R. 3746 – have continued to emerge. As of posting, Congress is expected to pass H.R. 3746 without amendment before June 5, when the Treasury Department would have “insufficient resources to satisfy the government’s obligations.”

For close observers of federal policy, it will come as no surprise that H.R. 3746 would have wide-ranging impacts on the future of the food and farm system. Throughout this post, the National Sustainable Agriculture Coalition (NSAC) examines several major components of the deal to better understand these impacts, including on annual appropriations and the 2023 Farm Bill reauthorization.

Overview

As introduced, the 100 pages of the Fiscal Responsibility Act cover several main areas. If enacted, the bill would:

- Establish fiscal year (FY) 2024 and FY2025 defense and non-defense discretionary (NDD) spending caps.

- Rescind $27 billion of unobligated funds that were provided to address COVID-19.

- End the suspension of federal student loan payments.

- Expand work requirements for the Supplemental Nutrition Assistance Program (SNAP) and the Temporary Assistance for Needy Families (TANF) program.

- Expedite the permitting process for energy projects.

- Extend the debt ceiling through January 1, 2025.

Overall, the Fiscal Responsibility Act importantly avoids a catastrophic default by extending the debt ceiling. It also avoids rescissions to the Inflation Reduction Act and is significantly less severe than the recently released FY2024 House Agriculture Appropriations Bill. Nonetheless, the agreement would still put a cap on the resilience of rural and urban communities nationwide through a combination of spending reductions, rescissions, and policy changes that establish obstacles to food assistance.

Discretionary Spending Caps

The single biggest cost reduction in the bill comes through the establishment of NDD spending caps for FY2024 and FY2025. Over the course of ten years, the Congressional Budget Office (CBO) estimates that the caps would save roughly $1.33 trillion, amounting to 87% of the cost-reductions in the bill.

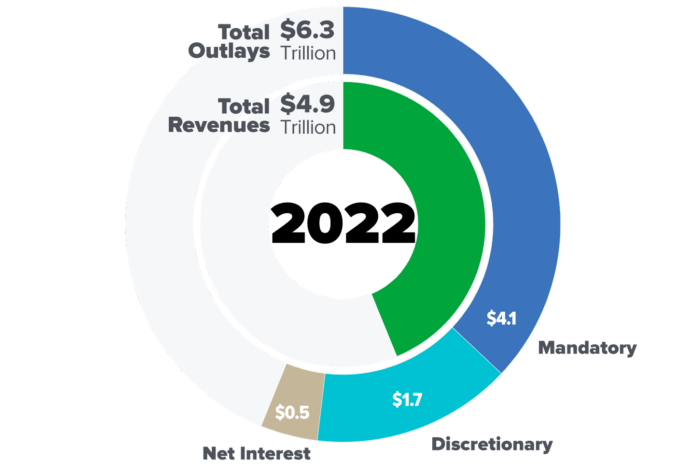

The three primary components of the federal budget are discretionary spending, mandatory spending, and federal revenues. Discretionary spending is governed by the annual appropriations process. Mandatory spending – often referred to as direct spending – is controlled by laws other than appropriation acts (e.g., the farm bill). Meanwhile, federal revenues include federal tax receipts and revenues from other sources. Overall, mandatory spending represents the majority of government spending in a given fiscal year. The graphic below shows the FY2022 federal budget, when $4.1 trillion went to mandatory spending, and $1.7 trillion to discretionary spending.

Source: Congressional Budget Office

Mandatory spending includes Medicaid, Medicare, and Social Security, and consequently has been shielded from cuts due to broad popularity. As a result, Congressional Republicans seeking to limit federal spending have focused nearly exclusively on discretionary spending.

The deal between President Biden and Speaker McCarthy focuses entirely on discretionary spending, and applies a cap of $703.65 billion in FY2024 and of $710.68 billion in FY2025. Based on the FY2023 enacted NDD spending of $772.5 billion, these new caps would be a 9% ($68.85 billion) and 8% ($61.82 billion) reduction, respectively, below the FY2023 enacted funding level.

However, H.R. 3746 is structured to allow for the rescission of certain unobligated funds (more on rescissions further below) to be used by Congressional appropriators to offset some of the reductions to discretionary spending. The Biden Administration originally anticipated roughly $27.7 billion to be available for appropriators as a result of the rescissions. However, the Congressional Budget Office score of H.R. 3746 indicates only $11 billion worth of outlays from the rescission of unobligated balances – meaning that from a budget perspective, Congressional appropriators could have less money than initially anticipated in order to reduce the discretionary cuts.

So, what exactly is the impact of the new discretionary spending caps on federal food and farm policy? In short, we know there will be at least some reduction to agriculture’s portion of discretionary spending, but we do not yet know how much. In theory, the discretionary spending reductions put in place by the Fiscal Responsibility Act could be spread out evenly across all ten domestic appropriations bills… but that’s not guaranteed. In the days and weeks ahead – as Congress moves toward drafting and finalizing its FY2024 appropriations bills – NSAC will be laser focused on the appropriations process to ensure investments in everything from local and regional food systems to on-farm conservation, agriculture research, and much, much more are are fairly resourced in FY2024 and beyond.

Rescissions

In addition to discretionary spending reductions, the Fiscal Responsibility Act includes dozens of rescissions of unobligated funding from previously passed legislation such as the American Rescue Plan Act (ARPA), the Consolidated Appropriations Act of 2021, and the CARES Act, among others – it also allows Congressional appropriators to reinvest the rescinded funding into FY2024 and FY2025 appropriations legislation. Perhaps unsurprisingly, there are a wide variety of rescissions targeted at the US Department of Agriculture (USDA). Below is a complete list of the USDA-focused rescissions included in H.R. 3746:

- Sec. 3 – rescinds all unobligated funds of the $9.5 billion from the CARES Act under the heading “Agricultural Programs-Office of the Secretary”, which were intended “to prevent, prepare for, and respond to coronavirus by providing support for agricultural producers impacted by coronavirus, including producers of specialty crops, producers that supply local food systems, including farmers markets, restaurants, and schools, and livestock producers, including dairy producers.”

- Sec. 4 – rescinds all unobligated funds from the $11.187 billion appropriated to USDA “to prevent, prepare for, and respond to coronavirus by providing support for agricultural producers, growers, and processors impacted by coronavirus, including producers and growers of specialty crops, non-specialty crops, dairy, livestock, and poultry, producers that supply local food systems, including farmers markets, restaurants, and schools, and growers who produce livestock or poultry under a contract for another entity.”

- Sec. 5 – rescinds all unobligated funds from the $100 million appropriated to the Local Agriculture Market Program to support local markets “due to the impacts [of] COVID–19.”

- Sec. 6 – rescinds all unobligated funds from the $75 million appropriated to the Farming Opportunities Training & Outreach Grant Program “due to the impacts of COVID–19 on certain producers.”

- Sec. 7 – rescinds all unobligated funds from the $400 million appropriated to the Dairy Donation Program which was established for the purposes of facilitating the timely donation of eligible dairy products and preventing and minimizing food waste.

- Sec. 8 – rescinds all unobligated funds from the $60 million appropriated for grants for improvements to meat and poultry facilities to allow for interstate shipment.

- Sec. 9 – rescinds all unobligated funds from the $4 billion appropriated to the food supply chain and agriculture pandemic response (Sec. 1001 of ARPA). The programs listed below are several that were authorized by Sec. 1001, and may or may not have unobligated funds remaining that are eligible for rescission:

- Regional Food Systems Infrastructure Program

- Indigenous Animals Harvesting and Meat Processing Program

- Local Meat Capacity Grants

- Sec. 60 – rescinds all unobligated funds from the $25 million appropriated to USDA’s Rural Utilities Services Distance Learning, Telemedicine, and Broadband Program.

- Sec. 61 – rescinds all unobligated funds from the $100 million appropriated to the Specialty Crop Block Grant program.

- Sec. 62 – rescinds all unobligated funds from the $500 million for Emergency Rural Development Grants for Rural Health Care.

In all, the Administration has estimated that the rescissions in H.R. 3746 would total approximately $27.7 billion which could be reinvested into discretionary spending. However, as briefly mentioned above, the CBO score of H.R. 3746 indicates that there are only $11 billion worth of outlays from rescissions that would be available for Congressional appropriators to reinvest in future discretionary appropriations legislation, including for agriculture. This difference is significant, to put it mildly, and indicates that discretionary cuts could be deeper than the Administration initially anticipated.

The rescissions would have significant consequences for food and agriculture. First, the difference between $27.7 billion and $11 billion would likely have a significant impact on the annual appropriations process, presumably leading to steeper cuts for appropriations legislation, including agriculture. Second, because the operating assumption is that all unobligated funds would be eligible for rescission, the passage of the Fiscal Responsibility Act would not only prevent future USDA initiatives from relying on funding provided by COVID-era resources, it would also prevent already-announced USDA initiatives from moving forward if they have funds that are yet to be obligated. In practice, this means that newly-announced programs with potentially unobligated funds – for example, the Resilient Food Systems Infrastructure Program or the Indigenous Animals Harvesting and Meat Processing Grant Program – could cease to operate even before they fully get off the ground, to the detriment of the communities they are designed to serve.

Nutrition

One of the most disappointing aspects of H.R. 3746 is the attack on nutrition assistance. Leading anti-hunger advocates have stated that the deal would “increase hunger and poverty among [very low-income older adults]” and that the “expansion of cruel, harsh, and arbitrary time limits on the Supplemental Nutrition Assistance Program (SNAP) for older unemployed and underemployed adults struggling in the labor market will only deepen hunger and poverty.”

NSAC’s vision of agriculture is, in part, one where family farmers contribute to the strength and stability of their communities. It is deeply disappointing to see a debt ceiling agreement that would weaken rural and urban communities alike by making it more challenging for hungry people to access food assistance through SNAP and TANF. Senator Debbie Stabenow (D-MI), Chair of the Senate Agriculture Committee, has voiced displeasure with the inclusion of these provisions in the agreement, and said that their inclusion “takes the issue of SNAP work requirements off the table” for the current farm bill reauthorization.

The CBO score of the Fiscal Responsibility Act released on May 30 also analyzed the cost of these proposed changes to SNAP and TANF. Contrary to the overall goal of H.R. 3746 – “fiscal responsibility” – the CBO found that the changes to SNAP and TANF would actually increase the deficit by over $2 billion by 2033.

Next Steps

As of posting, the Fiscal Responsibility Act is expected to pass Congress in the days ahead, thankfully averting a debt default. Yet the manufactured debt-default crisis would nonetheless cap investments in rural and urban communities, put up obstacles to food assistance, and potentially restrict some of USDA’s current initiatives. Beyond these, the debt agreement will undoubtedly impact the 2023 farm bill reauthorization – although the extent and scope of those impacts is still coming into focus.

Thank you for these details and elaborations. This knowledge, while troubling, helps me make adjustments to my program plans…you know, the part I can control.