It has been five years since the 2014 Farm Bill created Whole-Farm Revenue Protection (WFRP) – a new crop insurance policy championed by the National Sustainable Agriculture Coalition (NSAC) for its potential to level the playing field for producers underserved by other federal crop insurance options. WFRP replaced two former policies – Adjusted Gross Revenue (AGR) and Adjusted Gross Revenue Lite (AGR-Lite) – and offered producers (for the first time) the option to insure the revenue of their entire operation, including livestock and nursery production.

Over the first two years that WFRP was offered, NSAC’s analysis of data from the U.S. Department of Agriculture’s (USDA) Risk Management Agency (RMA) showed policies nearly doubled. Five years after its creation, however, the program is showing signs of slowing down. While the dip in enrollment over the past two years is concerning, it’s important to keep in mind that WFRP is still a program in its infancy that has plenty of time and opportunity to continue improving. In this post, we break down recent WFRP enrollment trends from the 2017 and 2018 crop insurance years.

Additional information on WFRP can be found on the NSAC Grassroots Guide WFRP webpage, RMA’s Whole-Farm Revenue Protection webpage, and in webinar form (webinar produced by NSAC, RAFI-USA, and NCAT).

WFRP Enrollment Trends

To date, the biggest enrollment period for WFRP was in 2017, when the program counted 2,728 policies sold and $2.83 billion in liabilities (total revenue insured). Since then, the number of policies sold and the amount of total liabilities has declined, by a total of 22 percent and 17 percent respectively. Despite this dip, however, over 2,000 policies were sold last year, representing over $2 billion in total liabilities. One positive decline occurred in the loss ratio, which is a calculation of total premiums to total claims that can show how well an insurance program is doing. An ideal loss ratio is 1.0 or less and the WFRP loss ratio decreased from 1.10 to 0.82, within the desired range.

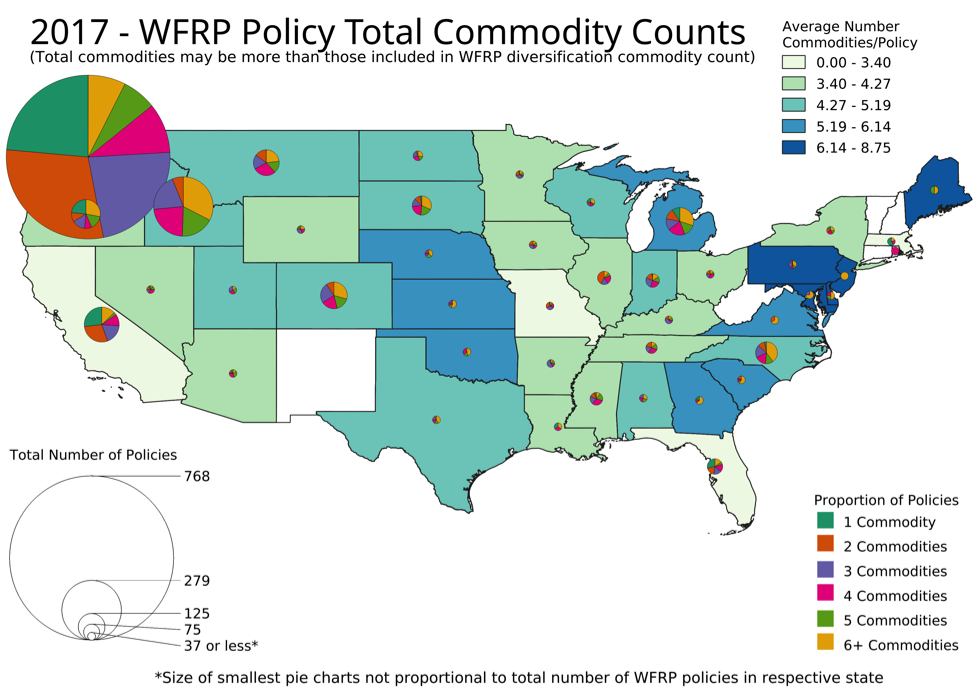

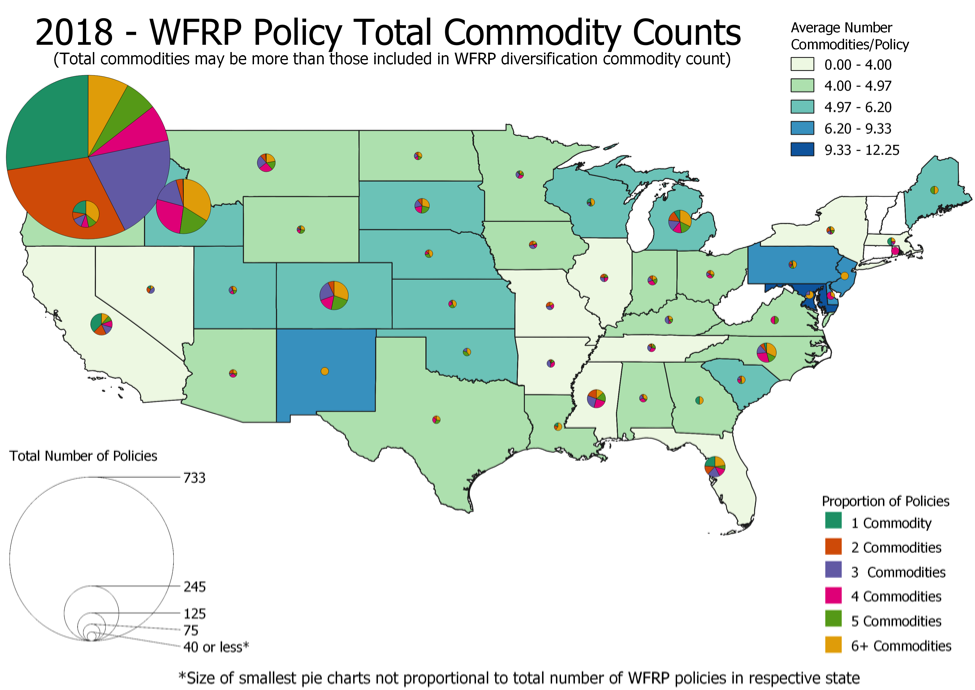

The reduction in WFRP policies over the last two years did not occur uniformly across the country. California, Florida, and Mississippi are among states that saw an increase in policies sold from 2017 to 2018, while Idaho, Illinois, and Oregon saw a decline in policies sold during the same time period. Washington State, which had the highest number of policies sold in both years, also experienced a slight decrease.

While we don’t have specific insight from farmers or crop insurance agents on the ground that explains some of these trends, we do know that there have been some recent challenges with the program which may have impacted recent enrollment numbers. For example, producers consistently report that crop insurance agents in their area don’t offer the policy, despite being legally required to do so, or discourage producers from signing up for the policy. Additionally, the extensive recordkeeping and paperwork requirements have been described as overly burdensome by some producers. Crop insurance agents also claim that the continuous updates to the policy make it difficult to write and administer.

The maps below provide a visual representation of the change in WFRP policies sold per state over the last two years, as well as the level of diversification for policies on a state-by-state basis. The diversification bonus is a unique feature of WFRP which encourages farmers to diversify their production with many different crops, rather than rely on monoculture or two-crop systems (e.g. corn and soybeans). This unique WFRP provision often results in greater economic value for the producer, reduced risk of a total loss in the event of a disaster, and enhanced biodiversity and environmental benefits on and around the farm.

Map credit: Jerzy Jaromczyk, Researcher at Cornell University. Based on: http://ageconmt.com/wfrp-in-mt/

Program Performance Summary

After five years of WFRP implementation and data aggregation, the program’s performance can be summarized as follows:

- WFRP is still in its infancy, representing on an annual basis just over two-tenths of one percent of total federal crop insurance policies and between 2 and 3 percent of total liabilities, with lots of room for growth.

- The percentage of policies and farm units earning premiums that ultimately receive indemnities (payment from a claim) due to loss is about the same for WFRP (23.5 percent) as for federal crop insurance as a whole (21.8 percent)

- The average WFRP subsidy is between 70 and 72 percent of the premium, somewhat more than 63 percent average for federal crop insurance as a whole.

WFRP Moving Forward

We are also currently working with RMA to simplify recordkeeping, improve expansion rules, and guarantee that insurance companies cannot adjust yield and price information at the time of a loss claim. NSAC will continue to work with farmers and ranchers across the country to identify issues within WFRP and ensure that they are quickly addressed by RMA in these annual reviews.

It’s important to keep in mind that WFRP is still a pilot program, which means it can be updated and improved each year by the Federal Crop Insurance Corporation. This flexibility is important for a newer program like WFRP because it allows the program to adapt and address issues as producers encounter and report them.

For example, the most recent changes to WFRP (approved in August 2019 for the 2020 insurance year) seek to address the problem of underinsurance by smoothing out WFRP’s five-year (three-years for beginning farmers and ranchers) revenue history requirement. The 2020 changes will also increase the amount of livestock production that can be covered under WFRP. NSAC welcomes these and other improvements slated for the 2020 insurance year, which will make the program more effective and user friendly in the coming crop insurance year – and we anticipate seeing enrollment numbers begin to tick back up in the coming years.

Nice report.. can you share the 2018 on diversification and did you break out for organic? As you know our data goes only up to 2017

I kind of disagree with this quote:

“Additionally, the extensive recordkeeping and paperwork requirements have been described as “backbreaking” by some and overly burdensome by producers. Crop insurance agents also claim that the continuous updates to the policy make it difficult to write and administer. ”

The paperwork argument is overblown, though many of the recommendations NCAT and NSAC has made to improve ought to lessen that burden. ALL crop insurance requires paperwork, it just that agents are used to selling and renewing single crop policies for major commodity crops and do not want to change that business model. We have found in our research that many agents like WFRP and many have made it a new way to expand their business.

Finally, it would have been nice to explicitly list the recommendations to improve.