“Do no harm” to crop insurance has become a common refrain in Washington DC as we gear up for a new farm bill this year. NSAC agrees that a top priority should be to not harm crop insurance as the 2023 Farm Bill debate heats up. In fact, we aim to improve it. Barriers in program design and implementation leave small to mid-sized, beginning, specialty crop, and organic farmers without access to this pivotal safety net program, and Congress has the opportunity to address these shortfalls.

Background

A federally subsidized farm safety net is a necessary tool to help protect farmers from the many risks of farming. Yet NSAC members have long supported and worked with farmers for whom crop insurance is inaccessible. Limited resource, small, beginning, diverse, and organic farmers find themselves choosing between either purchasing crop insurance each year, if a relevant policy is even available and advertised to them, or adopting on-farm conservation practices and diversifying production and markets to mitigate risk and improve long-term resilience against disasters. Almost invariably, they choose the latter.

If a farmer chooses to adopt conservation measures and diversification but then does not have enough remaining resources to be able to enroll in support of the farm safety net, it suggests that the program as it currently stands is not an effective tool that meets the needs of all farmers. No farmer should be forced to choose, and in fact, both strategies should be incentivized to help farmers manage risk.

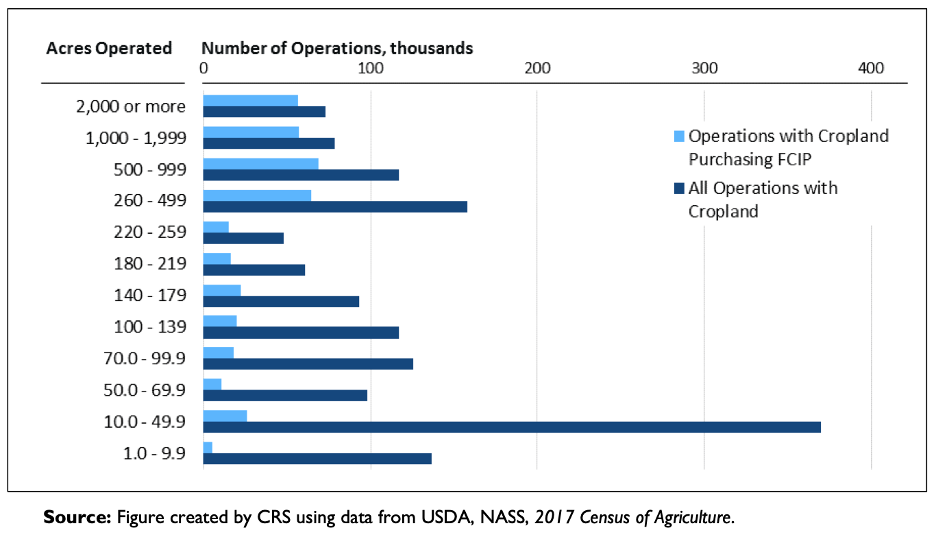

While more than 85 percent of planted acres for commodity crops (e.g., corn, soybeans, cotton, and wheat) are insured under the federal crop insurance program (FCIP), the chart below illustrates most farms are not served at all by the program. Most farms above 500 acres hold insurance policies, yet very few farms under 260 acres are enrolled in the FCIP relative to the total number of operations.

All Farms and Farms Purchasing FCIP Policies, by Acres Operated

The reason for this disparity in access is not because these farmers do not want a safety net to protect against the once-in-a-generation weather event or market pitfall that have become regular features of the farm economy. Rather, the FCIP was not designed to meet the needs of small, beginning, specialty crop, and organic farmers.

Why is crop insurance not working for everyone?

First, because it is not accessible to farmers looking to diversify their income streams or differentiate themselves in the marketplace.

The federal crop insurance program is a public-private partnership. Farmers purchase insurance policies from private sector insurers, known as Approved Insurance Providers (AIPs). USDA, specifically the Risk Management Agency (RMA), regulates the policies sold by AIPs, uses taxpayer dollars to subsidize farmer premiums (the cost of purchasing a policy), and subsidizes AIPs for the cost of selling and servicing crop insurance policies.

Farmers may file a claim to receive an indemnity payment when they experience an insurable event, either a natural peril or revenue losses (depending on the type of insurance policy purchased: yield, revenue, or area-based policies, and more). Insurable commodities vary by location and depend on whether data exists to verify the projected value of a farmer’s product confidently and appropriately.

This variability in whether a crop is insurable already places small, beginning, and specialty crop growers at a structural disadvantage. For example, a beginning farmer who wishes to grow strawberries in a Montana county where no other producer grows that crop will almost certainly not have the option to purchase an insurance policy that insures strawberries. If they desire the security of a safety net, the farmer will be incentivized to instead grow a commodity that is already widely grown in the county – such as wheat – which is unlikely to unlock market opportunity and allow the beginning farmer to differentiate themselves, but for which an insurance product is readily available.

Second, because it promotes monoculture commodity production over specialty crops and on-farm conservation.

Several rules and guidelines that determine how the FCIP is administered challenge the ability of nonconventional farmers to remain eligible for full crop insurance protections. For example, farmers must adhere to “Good Farming Practices” as defined by RMA to qualify for indemnity payments in the aftermath of an insurable event. RMA currently maintains that a practice which reduces yields may not be considered a Good Farming Practice. This is a serious deterrent against adoption of many conservation practices because temporary yield drags are common on farms transitioning to climate-friendly, regenerative, and organic systems before yields can stabilize and even rise.

Additional guidance on when and how cover crops may be terminated creates a similar disincentive. What should be a farm-specific decision is applied to a broad region wherein conditions may vary wildly from farm to farm.

Likewise, RMA determines regionally appropriate final planting dates, wherein acres planted on or before this date receive the full yield or revenue guarantee that a farmer selected when purchasing their insurance policy. Organic and conventional operations are currently held to the same final planting date, even though certified organic farmers sometimes plant crops such as corn later than their conventional counterparts to avoid cross-contamination with neighboring genetically engineered seed. The value of a yield or revenue guarantee is reduced each day for farmers who plant after the final planting date.

This structure to incentivize monoculture commodity production over specialty crops and diverse rotations is mirrored in eligibility considerations to receive agriculture loans as well as other public and commercial resources. The Whole-Farm Revenue Protection (WFRP) program is an exception to this paradigm and the dominant insurance model where the availability of policies is determined by crop and county. WFRP is the only insurance product designed to protect a farmer’s entire operation, not just one crop, and it is available nationwide. It also includes a built-in insurance premium discount for crop and enterprise diversification that considers the inherent risk reduction impacts of diversification. However, significant red tape has made it difficult for farmers to purchase WFRP. Recent changes announced by RMA are expected to improve farmers’ ability to access the product, and additional changes can and should be made.

How can insurance be improved to expand access?

There are many reasons why small, beginning, organic, diversified, and specialty crop farmers rarely purchase crop insurance. Historical barriers include limited policy availability, bureaucratic red tape (including burdensome paperwork), and insufficient outreach and education. While Congress and USDA in recent years have taken steps to address these challenges and expand insurance coverage for nonconventional producers, additional reforms are needed.

NSAC’s 2023 Farm Bill Platform proposes recommendations that will be key to improving crop insurance access for small and diversified farmers. In summary, these needed reforms include:

- Expanding insurance options and further streamlining the WFRP program;

- Directing RMA to provide continued education to insurance agents about agronomic practices and coverage options for nonconventional producers;

- Reforming barriers to conservation practice adoption perpetuated by insurance rules, including the RMA definition of Good Farming Practices and cover crop termination guidelines; and

- Establishing a secure data service to collect, link, and analyze data on conservation practices so this information can be integrated into crop insurance actuarial tables, as proposed in the Agriculture Innovation Act of 2021.

Remember: low enrollment in federal crop insurance policies among small and diversified farms does not reflect disinterest in participation. Overwhelmingly, these farmers desire a safety net to protect themselves from the worst impacts of unpredictable weather events and market variability, just as any other farmer does. It is the responsibility of Congress to ensure these historically underserved farmers can purchase an insurance policy as easily as their conventional counterparts.